Jun 7, 2026

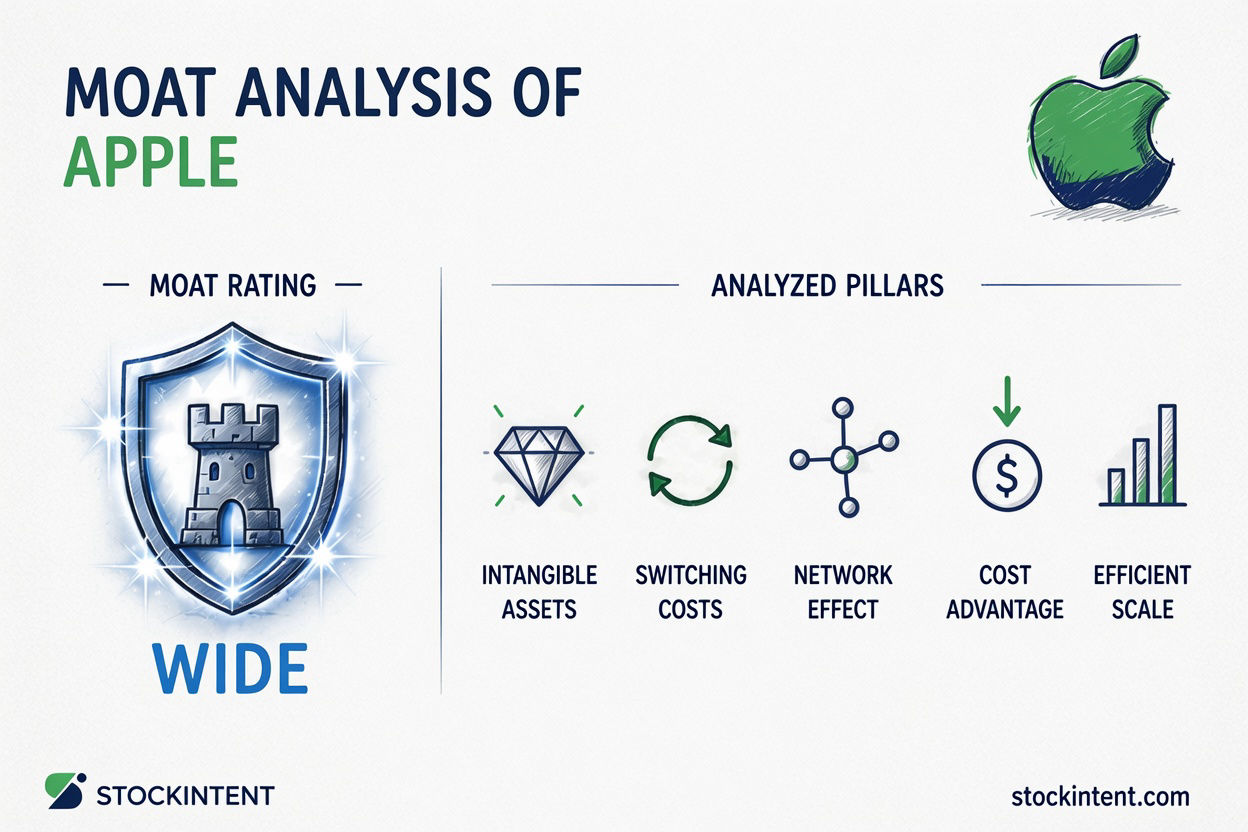

Apple still carries a wide economic moat in 2026, but the trend is best described as stable to slightly pressured rather than widening. The company's medium uncertainty rating reflects a business that prints exceptional returns on capital yet faces real questions about whether its advantages will prove as durable over the next decade as they have been over the last one.

The bull case is familiar and still mostly intact. Apple has built a massive device ecosystem, switching costs that deepen with every iMessage thread and iCloud photo library, and a premium brand that supports strong pricing. Its returns on invested capital have reportedly exceeded its cost of capital by a wide margin. The services segment, with its recurring revenue and high margins, has become the financial engine investors hoped for.

Still, the ground is shifting. Regulatory pressure on the App Store, the generative AI platform transition, and geopolitical friction around China and tariffs are not distant risks anymore. They're live debates that could affect distribution control, take rates, and supply chain stability. Some 2026 analysis flags services margin compression and AI integration costs as underappreciated threats. Siri and Apple Intelligence slipping into 2026 raised eyebrows about whether Apple can lead the next platform shift or merely participate in it.

Here's what matters most for investors evaluating Apple's competitive position:

From our experience analyzing moats across the technology sector, Apple's case illustrates a common tension. The historical evidence of durable competitive advantage is overwhelming, but the forward-looking question is what investors are actually being asked to pay for. A wide moat today does not automatically mean a widening moat tomorrow, and the difference matters enormously for long-term compounding. The ecosystem still looks hard to dislodge. Whether it remains hard to erode is the question this analysis explores.

Apple's moat doesn't rest on a single pillar. It's a layered defense where some walls are thick concrete and others are more like chain-link fencing. Let's walk through the five standard moat pillars and see which ones actually carry weight for Apple in 2026.

This is Apple's most reliable moat pillar, and it's not close.

The practical reality for most iPhone users: you've got iMessage threads spanning years, AirPods that pair instantly, an Apple Watch that won't work with Android, photos synced across iCloud, and probably a few subscriptions billed through Apple. Replacing all of that isn't just buying a different phone. It's reconstructing your digital life. Morningstar's March 2025 equity report identifies customer switching costs as a core source of Apple's wide economic moat.

The financial evidence for retention and installed-base scale appears in the business-performance section below. The practical cost of switching isn't just monetary; it's the time to migrate data, re-learn workflows, and lose ecosystem features that have become invisible habits.

We rate switching costs as very strong and Apple's most reliable moat pillar.

Apple's brand isn't just a logo. It's a premium positioning that lets the company charge $1,000+ for phones while cheaper alternatives remain widely available. Morningstar identifies Apple's differentiated user experience and vertically integrated design expertise as important intangible assets that support premium pricing and margins.

But the intangible asset runs deeper than pricing power. Apple's privacy positioning, design reputation, and the trust built through consistent software support (iOS updates for 5+ year old devices) create a preference that operates below conscious price comparison. Customers don't evaluate Android vs. iOS on a feature checklist. They feel the difference, or at least believe they do.

The risk here is generational. Younger users who grew up with TikTok and Spotify as their primary platforms may weight brand differently than millennials who remember the iPod-to-iPhone transition. But as of 2026, the intangible asset remains firmly intact.

We rate Apple's intangible assets as very strong. Brand durability is always debatable, but Apple's track record is hard to dismiss.

Apple's network effects aren't the classic two-sided marketplace variety like Visa or Airbnb. They're ecosystem network effects, and that distinction matters for how durable they are.

The mechanism works like this: more iPhone users attract more app developers, which improves the App Store selection, which makes iPhone more valuable, which attracts more users. Same loop for services like iMessage, FaceTime, and Find My. Morningstar identifies network effects associated with Apple's iOS ecosystem as one source of its moat.

The catch? These effects are weaker than pure platform dominance. A developer still builds for Android first if that's where the users are. The network effect is real but bounded; it reinforces the ecosystem rather than creating winner-take-all dynamics.

We rate Apple's network effects as moderate to strong: valuable, but less formidable than its switching costs.

Here's where we need to be honest. Apple is not a low-cost producer in the traditional sense. It doesn't win on price; it wins despite price.

That said, Apple does have selective cost advantages. Custom silicon (A-series and M-series chips) eliminates the Qualcomm/Intel tax and allows optimized performance-per-watt. Supply chain scale gives negotiating leverage with Foxconn, TSMC, and component suppliers. Vertical integration in chip design and software reduces dependency margins that competitors pay.

But calling this a "cost advantage" moat is misleading. Apple's gross margins aren't from being cheapest to produce; they're from pricing power and design efficiency. Some moat frameworks recognize selective cost and scale advantages, although these are less central than switching costs, brand, and ecosystem effects.

We rate the cost-advantage pillar as weak to moderate: helpful, but not a core moat driver.

Efficient scale as a moat concept applies best to industries with limited markets served by one or a few players, like railroads or utilities. Apple's markets are massive and fiercely contested.

Yes, Apple's scale matters. It enables the R&D budget ($30+ billion annually), the supply chain leverage, and the services economics that make Apple Music or TV+ viable. But scale here is better understood as an amplifier of other moats rather than a standalone competitive barrier. Samsung, Google, and Chinese competitors like Xiaomi operate at comparable or greater unit volumes in some segments.

We rate efficient scale as weak. It is relevant in parts of the business but not a clean moat fit.

Pro Insight: From our experience, the switching-cost pillar is where Apple most resembles the classic "razor and blades" model, except the razors are $1,000 and customers thank you for the privilege of buying them. Investors can underestimate this because it feels "soft" compared with manufacturing scale or patent counts. Yet retention and multi-device ownership trends provide observable evidence of ecosystem stickiness. When evaluating whether Apple's moat is widening or narrowing, watch switching costs and brand strength first.

A moat sounds great in theory. What matters is whether you can see it in the numbers. Here's where Apple's competitive advantages actually leave fingerprints.

Services profitability is the clearest evidence. One 2026 analysis states that Services generated $111.65 billion of revenue and roughly 41% of Apple's gross profit at a 75.6% gross margin. That's not just a side business anymore. It's direct monetization of ecosystem lock-in.

Returns on capital tell the same story. Morningstar reports fiscal 2024 ROE of 164.6% and forecasts fiscal 2026 ROA of 35.2%, supporting the analysis that Apple's moat produces unusually high capital efficiency.

Customer retention completes the picture. The installed base hit roughly 2.5 billion devices in early 2026, and iPhone retention rates have historically exceeded 90%. When someone owns three or more Apple devices, the probability of switching drops off a cliff. The moat shows up in behavior, not just spreadsheets.

| Moat Source | Observable Business Outcome | Strength |

|---|---|---|

| Ecosystem lock-in / switching costs | 90%+ iPhone retention, 2.5B device installed base | Very strong |

| Services monetization | 75.6% gross margin, ~41% of gross profit from 26% of revenue | Very strong |

| Brand / premium positioning | iPhone ASP ~$930 vs. industry average ~$300-400 | Strong |

| Returns on capital | ROE ~164%, ROA ~35%, FCF margins >27% | Very strong |

| Network effects | Developer ecosystem, iMessage/FaceTime stickiness | Moderate |

Pricing power is more disputed than the brand narrative suggests. Blank Capital Research reports Apple's 47.1% gross margin below its stated sector benchmark, suggesting that pricing power is less clear-cut than the premium-brand narrative implies. Product-mix shifts toward Pro models can also make average selling-price growth look stronger than broad price increases across the lineup.

App Store economics are under visible pressure. Regulatory action, particularly DMA-style enforcement in Europe, threatens the take rates and distribution control that underpin Services margins. One investment analysis argues that regulation is weakening the contractual protections around Apple's platform economics. The money is still flowing, but the legal plumbing is being rewired.

Scale advantages are weaker than commonly assumed. The same analysis that questioned pricing power also scored Apple's cost and scale advantage low. Apple doesn't win on manufacturing cost; it wins despite higher prices. Custom silicon helps, but it's more about differentiation than cost leadership.

In our experience analyzing moats across tech, the gap between "strategic moat" and "accounting moat" is where investors get hurt. Apple's Services gross margin and retention data pass the accounting test. The App Store's future take rate and Siri's competitive position do not yet. We therefore give more weight to visible cash-flow conversion than to strategic narrative. Apple's balance remains favorable, but the gap has narrowed.

Apple's moat is most visible where customers are already locked in and paying. It's least visible where regulation, competition, or technological shifts could change the rules. The services transition has made the moat more economically tangible, not less. But the same transition has concentrated risk in a revenue stream that regulators are actively targeting.

For investors doing their own apple moat analysis, the key question isn't whether Apple has advantages. It's whether those advantages are widening faster than the threats are mounting. The 2026 evidence is mixed: retention and services margins say yes; pricing power trends and regulatory pressure say maybe not.

We assess Apple's moat trend as stable to slightly pressured. The moat isn't collapsing, but the 2026 context is more defensive than offensive. The question investors face isn't whether Apple retains a wide moat. It's whether that moat is still expanding or has shifted into preservation mode as external constraints pile up.

The shift from offense to defense matters for compounding. A widening moat lets a company reinvest at high returns and grow into new areas. A stable moat protects existing cash flows but may not support the same expansion rate. Apple sits somewhere in between, with services growth pushing one direction and regulation, AI disruption, and China friction pulling the other.

Consumer technology in 2026 is being reshaped by AI-first computing and regulatory scrutiny of platform economics. CNBC frames Apple's entry into its second half-century around five major strategic questions. The value proposition is moving beyond devices toward intelligence, services, and ecosystem control.

Smartphones remain mature, but competition now centers on ecosystems, AI features, and regulatory access rather than hardware specs alone. Apple's moat quality depends more on software integration and distribution power than on unit growth. That's generally good for margins but creates vulnerability if AI platforms become the primary customer interface instead of the device itself.

Three developments currently support moat expansion:

Four headwinds are worth tracking closely:

Apple's geographic split is increasingly important for moat assessment. The US position looks stable to strong. In China, Apple's longer-term competitive position has weakened even as recent sales improved. An October 2025 moat analysis identifies Apple's weakening China position as a major test of its competitive durability. The moat appears strongest in high-income Western markets and most contested where local competition and geopolitics intersect.

Pro Insight: From our experience analyzing moats across technology, the geographic concentration of competitive strength is often underweighted. Apple's moat isn't uniform globally. We score geographic diversification separately because a strong US position can mask erosion elsewhere that eventually matters for total returns. When regional trends diverge, the source of that divergence, whether regulation, competition, or demographic shifts, matters.

| Indicator | What to Watch | Bullish Signal | Bearish Signal |

|---|---|---|---|

| Apple Intelligence / Siri engagement | Feature adoption, upgrade intent, daily usage metrics | Rising usage correlates with retention and upgrade acceleration | Weak adoption suggests AI strategy isn't differentiating |

| Services revenue growth and ARPU per device | Quarterly services growth, active device monetization trends | Sustained double-digit growth with stable or rising ARPU | Deceleration or ARPU compression |

| iPhone premium-segment share in US and China | Market share data, ASP trends, quarterly shipment estimates | Stable or rising share in both markets | Erosion, especially in China |

| Regulatory outcomes on App Store/search/payments | Court rulings, EU enforcement actions, legislative developments | No material take-rate or control reduction | Forced opening of platform economics |

These four indicators capture the core tension in Apple's moat trajectory. Services monetization and AI execution represent the expansion case. Regulatory and competitive pressure represent the contraction case. The balance between them will determine whether Apple's wide moat rating holds or narrows over the next 3-5 years.

For investors conducting their own apple moat analysis, the key discipline is separating what's already priced from what's still uncertain. The installed base, ecosystem lock-in, and services margins are largely understood. The AI transition path and regulatory endpoint are not. The return difference will likely come from handicapping those uncertainties better than the consensus does.

Apple earns a medium uncertainty rating in our apple moat analysis. That's not a knock on the business. It's a recognition that even the best companies face variables that can shift the range of plausible outcomes wider than the stock's day-to-day volatility suggests.

The revenue picture looks unusually predictable right now. Apple reported $143.8 billion in fiscal Q1 2026, up 16% year over year, with iPhone sales climbing 23%. Management guided Q2 revenue growth of 13% to 16%. Reuters reported that Apple beat Wall Street sales and profit estimates amid strong iPhone demand. That's the kind of visibility most consumer hardware companies only dream about.

Margins tell a similar story with one wrinkle. Gross margin hit 48.2% in Q1, above expectations, with Q2 guidance of 48% to 49%. But management warned that rising memory prices would have a greater impact on gross margins in the March quarter. It's a small headwind, not a crisis. Still, it reminds us that even Apple's pricing power has supply-side limits.

So why medium uncertainty instead of low? Three factors widen the range of outcomes beyond what the current quarter's beat suggests.

First, the iPhone cycle remains the dominant driver. Services growth and India expansion help diversify, but roughly half of revenue still rides on one product family. Replacement timing can shift by quarters, and AI-enabled upgrade enthusiasm is still unproven. CNBC's post-earnings analysis contrasted strong iPhone sales, including in China, with uncertainty about what comes next.

Second, geopolitical and regulatory exposure is live, not theoretical. China's recovery helps today; policy shifts or competitive pressure from Huawei could hurt tomorrow. The App Store faces ongoing regulatory scrutiny that could affect services economics, though quantifying that risk remains speculative.

Third, AI execution carries binary risk. Apple Intelligence and Siri improvements are central to the next upgrade cycle. Delays or underwhelming reception would weaken the core switching-cost mechanism that underpins the wide moat rating.

From our experience, medium uncertainty is the right call for businesses with fortress-like current performance but real questions about the 3-5 year trajectory. Apple's balance sheet strength, cash generation, and ecosystem lock-in compress the downside. The dependence on iPhone cycles, memory costs, regulatory outcomes, and AI execution widen the upside dispersion. The moat itself looks durable. The rate of compounding it generates is less certain than it was five years ago.

For investors conducting their own apple moat analysis, the discipline is distinguishing between "predictable next quarter" and "predictable next half-decade." Apple passes the first test easily. The second is where medium uncertainty earns its keep.

Apple's wide economic moat rating holds up in 2026, but the trend has shifted from expansion to preservation. The medium uncertainty rating reflects a business generating exceptional returns today while facing questions about whether those returns will compound at the same rate over the next decade.

The two issues that matter most from here: regulatory pressure on platform economics and AI execution risk. App Store take rates and distribution control are already under visible pressure in Europe and the US. That's not a distant threat; it's a live restructuring of how Apple monetizes its ecosystem. Meanwhile, Siri and Apple Intelligence arriving later than hoped raises a harder question. If generative AI becomes the primary interface rather than the device itself, the switching-cost advantage that underpins this entire moat analysis becomes less central to user behavior.

For investors conducting their own apple moat analysis, the discipline is distinguishing between what Apple has built and what it can still build. The forward question is whether its proven advantages are widening or merely defending territory. In 2026, the honest answer is: mostly defending, with selective opportunities to expand through services depth and privacy positioning.

The moat remains wide. Whether it remains wide enough to justify the premium investors pay is the separate question this framework helps you evaluate, not answer.

Apple still carries a wide economic moat in 2026, but the trend is best described as stable to slightly pressured rather than widening. The company's medium uncertainty rating reflects a business that prints exceptional returns on capital yet faces real questions about whether its advantages will prove as durable over the next decade as they have been over the last one.

The bull case is familiar and still mostly intact. Apple has built a massive device ecosystem, switching costs that deepen with every iMessage thread and iCloud photo library, and a premium brand that supports strong pricing. Its returns on invested capital have reportedly exceeded its cost of capital by a wide margin. The services segment, with its recurring revenue and high margins, has become the financial engine investors hoped for.

Still, the ground is shifting. Regulatory pressure on the App Store, the generative AI platform transition, and geopolitical friction around China and tariffs are not distant risks anymore. They're live debates that could affect distribution control, take rates, and supply chain stability. Some 2026 analysis flags services margin compression and AI integration costs as underappreciated threats. Siri and Apple Intelligence slipping into 2026 raised eyebrows about whether Apple can lead the next platform shift or merely participate in it.

Here's what matters most for investors evaluating Apple's competitive position:

From our experience analyzing moats across the technology sector, Apple's case illustrates a common tension. The historical evidence of durable competitive advantage is overwhelming, but the forward-looking question is what investors are actually being asked to pay for. A wide moat today does not automatically mean a widening moat tomorrow, and the difference matters enormously for long-term compounding. The ecosystem still looks hard to dislodge. Whether it remains hard to erode is the question this analysis explores.

Apple's moat doesn't rest on a single pillar. It's a layered defense where some walls are thick concrete and others are more like chain-link fencing. Let's walk through the five standard moat pillars and see which ones actually carry weight for Apple in 2026.

This is Apple's most reliable moat pillar, and it's not close.

The practical reality for most iPhone users: you've got iMessage threads spanning years, AirPods that pair instantly, an Apple Watch that won't work with Android, photos synced across iCloud, and probably a few subscriptions billed through Apple. Replacing all of that isn't just buying a different phone. It's reconstructing your digital life. Morningstar's March 2025 equity report identifies customer switching costs as a core source of Apple's wide economic moat.

The financial evidence for retention and installed-base scale appears in the business-performance section below. The practical cost of switching isn't just monetary; it's the time to migrate data, re-learn workflows, and lose ecosystem features that have become invisible habits.

We rate switching costs as very strong and Apple's most reliable moat pillar.

Apple's brand isn't just a logo. It's a premium positioning that lets the company charge $1,000+ for phones while cheaper alternatives remain widely available. Morningstar identifies Apple's differentiated user experience and vertically integrated design expertise as important intangible assets that support premium pricing and margins.

But the intangible asset runs deeper than pricing power. Apple's privacy positioning, design reputation, and the trust built through consistent software support (iOS updates for 5+ year old devices) create a preference that operates below conscious price comparison. Customers don't evaluate Android vs. iOS on a feature checklist. They feel the difference, or at least believe they do.

The risk here is generational. Younger users who grew up with TikTok and Spotify as their primary platforms may weight brand differently than millennials who remember the iPod-to-iPhone transition. But as of 2026, the intangible asset remains firmly intact.

We rate Apple's intangible assets as very strong. Brand durability is always debatable, but Apple's track record is hard to dismiss.

Apple's network effects aren't the classic two-sided marketplace variety like Visa or Airbnb. They're ecosystem network effects, and that distinction matters for how durable they are.

The mechanism works like this: more iPhone users attract more app developers, which improves the App Store selection, which makes iPhone more valuable, which attracts more users. Same loop for services like iMessage, FaceTime, and Find My. Morningstar identifies network effects associated with Apple's iOS ecosystem as one source of its moat.

The catch? These effects are weaker than pure platform dominance. A developer still builds for Android first if that's where the users are. The network effect is real but bounded; it reinforces the ecosystem rather than creating winner-take-all dynamics.

We rate Apple's network effects as moderate to strong: valuable, but less formidable than its switching costs.

Here's where we need to be honest. Apple is not a low-cost producer in the traditional sense. It doesn't win on price; it wins despite price.

That said, Apple does have selective cost advantages. Custom silicon (A-series and M-series chips) eliminates the Qualcomm/Intel tax and allows optimized performance-per-watt. Supply chain scale gives negotiating leverage with Foxconn, TSMC, and component suppliers. Vertical integration in chip design and software reduces dependency margins that competitors pay.

But calling this a "cost advantage" moat is misleading. Apple's gross margins aren't from being cheapest to produce; they're from pricing power and design efficiency. Some moat frameworks recognize selective cost and scale advantages, although these are less central than switching costs, brand, and ecosystem effects.

We rate the cost-advantage pillar as weak to moderate: helpful, but not a core moat driver.

Efficient scale as a moat concept applies best to industries with limited markets served by one or a few players, like railroads or utilities. Apple's markets are massive and fiercely contested.

Yes, Apple's scale matters. It enables the R&D budget ($30+ billion annually), the supply chain leverage, and the services economics that make Apple Music or TV+ viable. But scale here is better understood as an amplifier of other moats rather than a standalone competitive barrier. Samsung, Google, and Chinese competitors like Xiaomi operate at comparable or greater unit volumes in some segments.

We rate efficient scale as weak. It is relevant in parts of the business but not a clean moat fit.

Pro Insight: From our experience, the switching-cost pillar is where Apple most resembles the classic "razor and blades" model, except the razors are $1,000 and customers thank you for the privilege of buying them. Investors can underestimate this because it feels "soft" compared with manufacturing scale or patent counts. Yet retention and multi-device ownership trends provide observable evidence of ecosystem stickiness. When evaluating whether Apple's moat is widening or narrowing, watch switching costs and brand strength first.

A moat sounds great in theory. What matters is whether you can see it in the numbers. Here's where Apple's competitive advantages actually leave fingerprints.

Services profitability is the clearest evidence. One 2026 analysis states that Services generated $111.65 billion of revenue and roughly 41% of Apple's gross profit at a 75.6% gross margin. That's not just a side business anymore. It's direct monetization of ecosystem lock-in.

Returns on capital tell the same story. Morningstar reports fiscal 2024 ROE of 164.6% and forecasts fiscal 2026 ROA of 35.2%, supporting the analysis that Apple's moat produces unusually high capital efficiency.

Customer retention completes the picture. The installed base hit roughly 2.5 billion devices in early 2026, and iPhone retention rates have historically exceeded 90%. When someone owns three or more Apple devices, the probability of switching drops off a cliff. The moat shows up in behavior, not just spreadsheets.

| Moat Source | Observable Business Outcome | Strength |

|---|---|---|

| Ecosystem lock-in / switching costs | 90%+ iPhone retention, 2.5B device installed base | Very strong |

| Services monetization | 75.6% gross margin, ~41% of gross profit from 26% of revenue | Very strong |

| Brand / premium positioning | iPhone ASP ~$930 vs. industry average ~$300-400 | Strong |

| Returns on capital | ROE ~164%, ROA ~35%, FCF margins >27% | Very strong |

| Network effects | Developer ecosystem, iMessage/FaceTime stickiness | Moderate |

Pricing power is more disputed than the brand narrative suggests. Blank Capital Research reports Apple's 47.1% gross margin below its stated sector benchmark, suggesting that pricing power is less clear-cut than the premium-brand narrative implies. Product-mix shifts toward Pro models can also make average selling-price growth look stronger than broad price increases across the lineup.

App Store economics are under visible pressure. Regulatory action, particularly DMA-style enforcement in Europe, threatens the take rates and distribution control that underpin Services margins. One investment analysis argues that regulation is weakening the contractual protections around Apple's platform economics. The money is still flowing, but the legal plumbing is being rewired.

Scale advantages are weaker than commonly assumed. The same analysis that questioned pricing power also scored Apple's cost and scale advantage low. Apple doesn't win on manufacturing cost; it wins despite higher prices. Custom silicon helps, but it's more about differentiation than cost leadership.

In our experience analyzing moats across tech, the gap between "strategic moat" and "accounting moat" is where investors get hurt. Apple's Services gross margin and retention data pass the accounting test. The App Store's future take rate and Siri's competitive position do not yet. We therefore give more weight to visible cash-flow conversion than to strategic narrative. Apple's balance remains favorable, but the gap has narrowed.

Apple's moat is most visible where customers are already locked in and paying. It's least visible where regulation, competition, or technological shifts could change the rules. The services transition has made the moat more economically tangible, not less. But the same transition has concentrated risk in a revenue stream that regulators are actively targeting.

For investors doing their own apple moat analysis, the key question isn't whether Apple has advantages. It's whether those advantages are widening faster than the threats are mounting. The 2026 evidence is mixed: retention and services margins say yes; pricing power trends and regulatory pressure say maybe not.

We assess Apple's moat trend as stable to slightly pressured. The moat isn't collapsing, but the 2026 context is more defensive than offensive. The question investors face isn't whether Apple retains a wide moat. It's whether that moat is still expanding or has shifted into preservation mode as external constraints pile up.

The shift from offense to defense matters for compounding. A widening moat lets a company reinvest at high returns and grow into new areas. A stable moat protects existing cash flows but may not support the same expansion rate. Apple sits somewhere in between, with services growth pushing one direction and regulation, AI disruption, and China friction pulling the other.

Consumer technology in 2026 is being reshaped by AI-first computing and regulatory scrutiny of platform economics. CNBC frames Apple's entry into its second half-century around five major strategic questions. The value proposition is moving beyond devices toward intelligence, services, and ecosystem control.

Smartphones remain mature, but competition now centers on ecosystems, AI features, and regulatory access rather than hardware specs alone. Apple's moat quality depends more on software integration and distribution power than on unit growth. That's generally good for margins but creates vulnerability if AI platforms become the primary customer interface instead of the device itself.

Three developments currently support moat expansion:

Four headwinds are worth tracking closely:

Apple's geographic split is increasingly important for moat assessment. The US position looks stable to strong. In China, Apple's longer-term competitive position has weakened even as recent sales improved. An October 2025 moat analysis identifies Apple's weakening China position as a major test of its competitive durability. The moat appears strongest in high-income Western markets and most contested where local competition and geopolitics intersect.

Pro Insight: From our experience analyzing moats across technology, the geographic concentration of competitive strength is often underweighted. Apple's moat isn't uniform globally. We score geographic diversification separately because a strong US position can mask erosion elsewhere that eventually matters for total returns. When regional trends diverge, the source of that divergence, whether regulation, competition, or demographic shifts, matters.

| Indicator | What to Watch | Bullish Signal | Bearish Signal |

|---|---|---|---|

| Apple Intelligence / Siri engagement | Feature adoption, upgrade intent, daily usage metrics | Rising usage correlates with retention and upgrade acceleration | Weak adoption suggests AI strategy isn't differentiating |

| Services revenue growth and ARPU per device | Quarterly services growth, active device monetization trends | Sustained double-digit growth with stable or rising ARPU | Deceleration or ARPU compression |

| iPhone premium-segment share in US and China | Market share data, ASP trends, quarterly shipment estimates | Stable or rising share in both markets | Erosion, especially in China |

| Regulatory outcomes on App Store/search/payments | Court rulings, EU enforcement actions, legislative developments | No material take-rate or control reduction | Forced opening of platform economics |

These four indicators capture the core tension in Apple's moat trajectory. Services monetization and AI execution represent the expansion case. Regulatory and competitive pressure represent the contraction case. The balance between them will determine whether Apple's wide moat rating holds or narrows over the next 3-5 years.

For investors conducting their own apple moat analysis, the key discipline is separating what's already priced from what's still uncertain. The installed base, ecosystem lock-in, and services margins are largely understood. The AI transition path and regulatory endpoint are not. The return difference will likely come from handicapping those uncertainties better than the consensus does.

Apple earns a medium uncertainty rating in our apple moat analysis. That's not a knock on the business. It's a recognition that even the best companies face variables that can shift the range of plausible outcomes wider than the stock's day-to-day volatility suggests.

The revenue picture looks unusually predictable right now. Apple reported $143.8 billion in fiscal Q1 2026, up 16% year over year, with iPhone sales climbing 23%. Management guided Q2 revenue growth of 13% to 16%. Reuters reported that Apple beat Wall Street sales and profit estimates amid strong iPhone demand. That's the kind of visibility most consumer hardware companies only dream about.

Margins tell a similar story with one wrinkle. Gross margin hit 48.2% in Q1, above expectations, with Q2 guidance of 48% to 49%. But management warned that rising memory prices would have a greater impact on gross margins in the March quarter. It's a small headwind, not a crisis. Still, it reminds us that even Apple's pricing power has supply-side limits.

So why medium uncertainty instead of low? Three factors widen the range of outcomes beyond what the current quarter's beat suggests.

First, the iPhone cycle remains the dominant driver. Services growth and India expansion help diversify, but roughly half of revenue still rides on one product family. Replacement timing can shift by quarters, and AI-enabled upgrade enthusiasm is still unproven. CNBC's post-earnings analysis contrasted strong iPhone sales, including in China, with uncertainty about what comes next.

Second, geopolitical and regulatory exposure is live, not theoretical. China's recovery helps today; policy shifts or competitive pressure from Huawei could hurt tomorrow. The App Store faces ongoing regulatory scrutiny that could affect services economics, though quantifying that risk remains speculative.

Third, AI execution carries binary risk. Apple Intelligence and Siri improvements are central to the next upgrade cycle. Delays or underwhelming reception would weaken the core switching-cost mechanism that underpins the wide moat rating.

From our experience, medium uncertainty is the right call for businesses with fortress-like current performance but real questions about the 3-5 year trajectory. Apple's balance sheet strength, cash generation, and ecosystem lock-in compress the downside. The dependence on iPhone cycles, memory costs, regulatory outcomes, and AI execution widen the upside dispersion. The moat itself looks durable. The rate of compounding it generates is less certain than it was five years ago.

For investors conducting their own apple moat analysis, the discipline is distinguishing between "predictable next quarter" and "predictable next half-decade." Apple passes the first test easily. The second is where medium uncertainty earns its keep.

Apple's wide economic moat rating holds up in 2026, but the trend has shifted from expansion to preservation. The medium uncertainty rating reflects a business generating exceptional returns today while facing questions about whether those returns will compound at the same rate over the next decade.

The two issues that matter most from here: regulatory pressure on platform economics and AI execution risk. App Store take rates and distribution control are already under visible pressure in Europe and the US. That's not a distant threat; it's a live restructuring of how Apple monetizes its ecosystem. Meanwhile, Siri and Apple Intelligence arriving later than hoped raises a harder question. If generative AI becomes the primary interface rather than the device itself, the switching-cost advantage that underpins this entire moat analysis becomes less central to user behavior.

For investors conducting their own apple moat analysis, the discipline is distinguishing between what Apple has built and what it can still build. The forward question is whether its proven advantages are widening or merely defending territory. In 2026, the honest answer is: mostly defending, with selective opportunities to expand through services depth and privacy positioning.

The moat remains wide. Whether it remains wide enough to justify the premium investors pay is the separate question this framework helps you evaluate, not answer.