Mar 3, 2026

If you're evaluating Broadcom (AVGO) for your portfolio, understanding what actually drives this semiconductor giant is essential. Here's what surprised me when I dug into it: unlike most Fortune 500 companies, Broadcom doesn't plaster a catchy mission statement on its homepage. Their purpose shows up in their strategy and actions instead.

Key Takeaways:

The company's strategic direction has evolved dramatically in recent years. Broadcom now generates roughly 60% of revenue from Semiconductor Solutions (including AI accelerators and networking chips) and 40% from Infrastructure Software (led by VMware Cloud Foundation). This isn't just diversification - it's a deliberate move to capture the entire technology stack that enterprises need for AI and digital transformation.

Let's get into the nuts and bolts of what Broadcom actually does today. The company runs two distinct but complementary businesses that together pulled in $63.9 billion in fiscal 2025 according to official guidance — and they're expecting Q1 2026 to hit $19.1 billion in just a single quarter. That kind of scale puts them in rare company.

Here’s what you need to know in 30 seconds:

These figures come from Broadcom's financial releases and market analysis.

In our experience analyzing tech giants, the magic isn't just in these numbers — it's in how Broadcom has positioned itself as "the tollroad for AI giants". While Nvidia captures headlines with GPUs, Broadcom quietly supplies custom AI accelerators (ASICs/XPUs) that power Google's TPUs and Meta's MTIA chips. They don't compete head-on; they make themselves indispensable. This shows up in their competitive positioning: they're winning share from hyperscalers while facing threats from customer insourcing (Apple building its own Wi-Fi chips) and rivals like AMD and Marvell, as strategic analysis explains.

The VMware acquisition changed everything. Before 2023, Broadcom was a semiconductor pure-play. Today, that 60/40 revenue split reflects a deliberate strategy to own the entire enterprise stack, from the silicon that moves bits to the software that manages entire data centers. It's a moat-building exercise in real time.

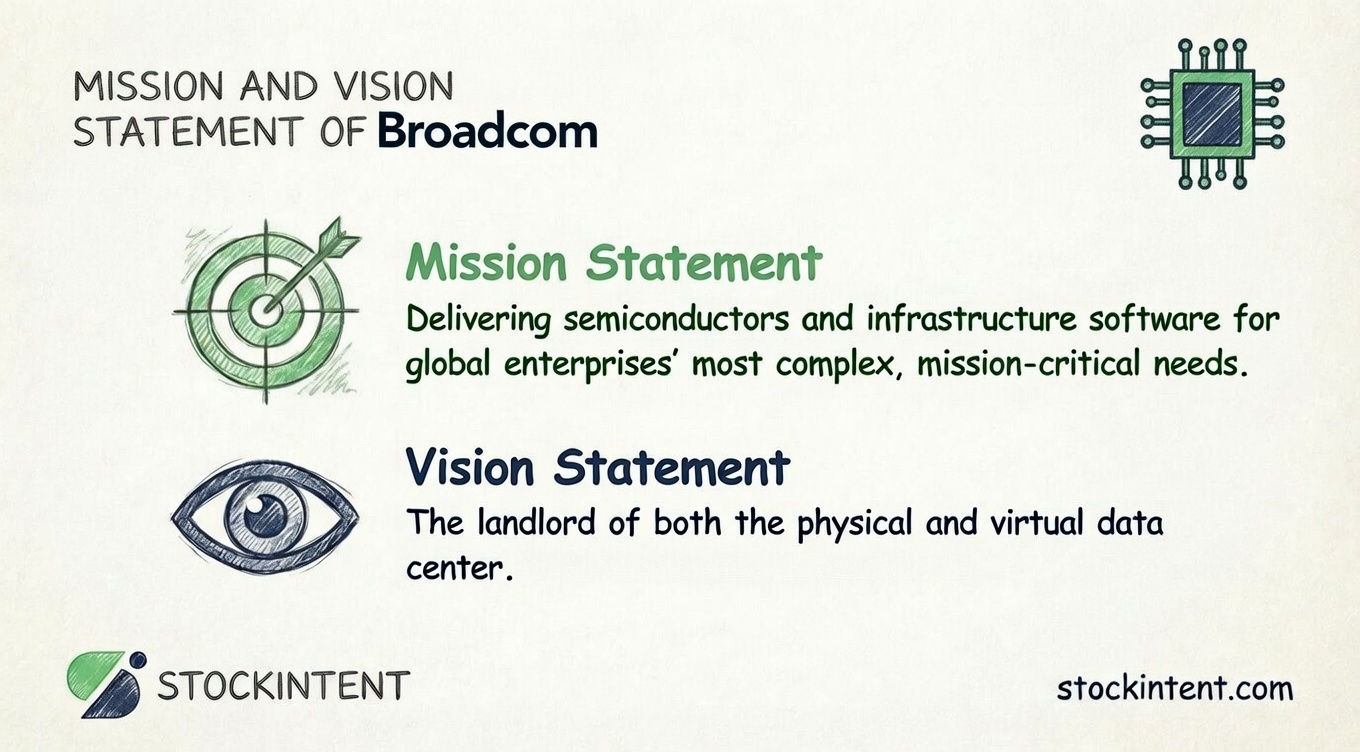

Here's the thing most investors miss when researching Broadcom: they don't actually publish a traditional mission statement. While most S&P 500 companies lead with inspiring corporate mantras, Broadcom's so-called mission lives in their actions and strategic choices. Their de facto purpose centers on delivering semiconductors and infrastructure software for global enterprises' most complex, mission-critical needs.

What this signals about Broadcom's priorities

This isn't a marketing oversight; it's a deliberate reflection of their engineering-first culture. Where competitors like STMicroelectronics pledge to "master the semiconductor supply chain for a sustainable world" and Samsung promises to "contribute to a better global society," Broadcom's language stays grounded in product delivery and customer dependency. They focus on being indispensable rather than aspirational.

🎯 Pro Insight: When evaluating mission statements, pay attention to what isn't said. Broadcom's silence on broad societal goals while emphasizing "mission-critical needs" reveals a capital allocation philosophy that prioritizes high-margin, moat-worthy markets over virtuous signaling. This shows up in their 60/40 semiconductor-software revenue split and $110 billion backlog, both designed for predictable, recurring cash flows rather than flashy growth narratives.

Connecting mission to capital decisions

This de facto mission directly shapes their acquisition strategy. The $69 billion VMware purchase wasn't about chasing cloud trends; it was about becoming "the landlord of both physical and virtual data centers" by owning the software layer that enterprises can't rip out. Every major move, from CA Technologies to Symantec, follows the same pattern: buy mission-critical infrastructure, optimize it for cash flow, and create switching costs that keep customers locked in, as strategic analysis explains.

Why this matters for investors

For those analyzing AVGO as a potential holding, this mission-in-action approach translates to financial predictability. Rather than betting on innovation cycles or consumer trends, you're buying into a company that makes itself essential to the AI infrastructure build-out while facing threats from customer insourcing and rivals like Marvell. The mission, if you can call it that, is simple: be the tollroad, not the destination.

Here's where things get interesting. Broadcom doesn't just operate randomly; their actions cluster around three distinct strategic pillars that actually matter for your investment analysis. Think of these as the load-bearing walls of their entire operation. Each pillar directly translates to competitive advantages you can measure.

This isn't marketing fluff about "changing the world." For Broadcom, it means pouring money into R&D that solves hyperscaler problems at scale. What it is: relentless engineering focus on AI infrastructure, custom silicon, and high-speed networking that makes competitors irrelevant.

Why it matters strategically: In semiconductors, being first doesn't win; being indispensable does. When you're the only company that can deliver custom AI accelerators for Google's TPUs and Meta's MTIA chips, you don't compete on price. You set terms. This shows up in their Q3 2025 numbers: that R&D spend helped generate $7.0 billion in free cash flow while AI semiconductor revenue hit $6.2 billion, up 66% year-over-year.

The concrete example? Their dual-engine model before VMware was roughly 80% semiconductors. Now it's evolved into a tollroad architecture where they capture AI utility layer revenue whether customers build on their chips or their software. That's moat-building in real time. In our experience analyzing tech giants, companies that can maintain 60%+ gross margins while growing AI revenue 66% annually aren't innovating for novelty. They're building walls.

This pillar explains why Broadcom dropped $69 billion on VMware. What it is: creating a full-stack portfolio where customers can't easily rip out one piece without breaking everything else. Semiconductors, networking, security, and enterprise software all integrated together.

Why it matters: Switching costs become astronomical. When your data center runs on Broadcom's Tomahawk chips, VMWare Cloud Foundation, and Symantec security, switching to piecemeal competitors means ripping out three integrated systems simultaneously. Most CFOs won't approve that disruption.

The metric that proves this works? Software revenue grew from 26% to 45% of the mix post-VMware, and operating margins expanded from 15% in 2016 to 32% today. That's not acquisition math; that's integration discipline. Every dollar of software revenue converts to higher-margin recurring cash flows than chips alone. For investors, this means you're buying a company that gets more profitable as it gets larger, which is exactly what you want in a long-term holding.

This is the "landlord of data centers" vision made concrete. What it is: positioning Broadcom as the infrastructure backbone for enterprises and governments that can't afford downtime or security breaches.

Why it matters strategically: This focuses them exclusively on high-margin, mission-critical markets where customers pay premium prices for reliability. They aren't chasing consumer fads or low-margin commodity chips. They're selling to the Fortune 500 and federal agencies with decade-long procurement cycles.

The evidence? That $110 billion backlog gives them revenue visibility most semiconductor companies can only dream about. Add the GSA partnership providing federal agencies discounted enterprise software access, and you see a pattern: Broadcom embeds itself into customer operations so deeply that removing them becomes a career-limiting move for CTOs. That's the economic moat you're paying for when you buy AVGO at 12.5x forward earnings. It doesn't make their stock cheap, but it does make their cash flows predictable, and in 2026's volatile market, predictability is worth a premium.

If you're looking for a glossy vision statement to slap on a PowerPoint slide, Broadcom will disappoint you. Just like with their mission, the company doesn't bother with corporate poetry. What they have instead is a strategic north star that actually matters for your investment analysis.

CEO Hock Tan has been crystal clear about where Broadcom is heading. He describes the company as "the landlord of both the physical and virtual data center." Not a tenant. Not a service provider. The landlord.

"the landlord of both the physical and virtual data center" — CEO Hock Tan on Broadcom's strategic vision

This single phrase explains that $69 billion VMware acquisition we mentioned earlier and that deliberate 60/40 revenue split strategic analysis of Broadcom's positioning. Tan isn't chasing AI hype cycles or cloud buzzwords. He's building a tollroad architecture where Broadcom captures utility-layer revenue whether enterprises build on their chips or their software. The physical data center? That's the semiconductor side: Tomahawk networking chips, custom AI accelerators for Google and Meta, the silicon that moves bits. The virtual data center? That's VMware Cloud Foundation, the software layer enterprises literally cannot rip out without breaking their entire IT operation.

In our experience analyzing tech giants, this landlord positioning is brilliant precisely because it's boring. While Nvidia grabs headlines with GPUs, Broadcom quietly makes itself indispensable to the actual infrastructure AI runs on. They're not trying to be the flashiest tenant in the building; they own the building.

This vision aligns perfectly with 2026's macro trends. The AI infrastructure build-out isn't just about training models; it's about networking, data center management, and enterprise integration Broadcom's AI-era strategy. Broadcom's dual-engine approach positions them to collect rent from both sides of that equation.

Here's where we get into the actual playbook. Broadcom's vision isn't just words on a wall; it's three distinct themes that show up in every major decision. If you're evaluating AVGO as a long-term holding, these are the strategic patterns you need to recognize because they directly impact capital allocation and competitive moats.

Broadcom leadership has made it crystal clear: private cloud isn't a legacy option, it's the control plane for digital transformation. This isn't about fighting the public cloud giants; it's about becoming the indispensable infrastructure layer enterprises can't operate without.

How this shapes strategy: Every dollar spent and every product roadmap decision flows through this lens. The $1 billion R&D investment in VMware Cloud Foundation 9.0 wasn't about feature parity with AWS; it was about creating a unified platform that lets enterprises run AI workloads with the security and compliance they can't get elsewhere Futurum Group analysis of VCF 9.0.

Observable moves: Beyond the VMware acquisition itself, you're seeing this in the GSA OneGov partnership giving federal agencies discounted access official GSA announcement. That's not a one-off deal; it's embedding Broadcom into decade-long government procurement cycles where ripping it out becomes a political problem, not just a technical one.

Analyst interpretation: Industry researchers note this represents a "profound transformation" where private cloud is emerging as the strategic centerpiece, not a secondary option Private Cloud Outlook 2025. The moat here isn't just switching costs; it's regulatory compliance and data sovereignty that public clouds struggle to match.

Remember that "landlord of physical and virtual data centers" vision? This is the physical half made concrete. Broadcom isn't trying to beat Nvidia at GPUs; they're making themselves indispensable to the AI infrastructure that GPUs run on.

How this shapes strategy: The company positions AI not as a product line but as a strategy that permeates everything. When they announced the industry's first Enterprise Wi-Fi 8 Access Point for the AI Era, it wasn't about Wi-Fi speeds; it was about creating the networking fabric AI workloads require Broadcom product announcement.

Observable moves: The numbers tell the story. AI semiconductor revenue hit $6.2 billion last quarter, up 66% year-over-year, representing 22% of total revenue Broadcom Q4 2025 financial release. More importantly, that $110 billion backlog we mentioned earlier is heavily weighted toward custom AI accelerators for Google TPUs and Meta MTIA chips. When you're the only company that can deliver at that scale, you don't compete on price; you set terms.

Analyst interpretation: Market watchers are bullish on this positioning, noting Broadcom "enables hyperscalers to design custom AI inference chips as a more efficient alternative to Nvidia" MarketBeat analyst coverage. The consensus view is that this isn't a cyclical AI play; it's a structural position in the infrastructure layer that benefits regardless of which AI models win.

Here's a theme that doesn't get enough attention but explains Broadcom's margin expansion. In 2026, they're fundamentally shifting from direct service delivery to a partner-led model. Think of it as moving from being a general contractor to being the supplier that every contractor has to buy from.

How this shapes strategy: The channel chief describes 2026 as a "once-in-an-every-other-decade kind of opportunity" centered on delivering AI, on-premises, and private cloud solutions CRN interview on 2026 partner strategy. The strategy is explicit: AI is the strategy, private cloud is the control plane, and edge computing is the operational model Broadcom partner success blog.

Observable moves: In April 2025, they slashed authorized VMware Cloud Service Providers from over 4,500 to a smaller, elite group Intelisys analysis of licensing changes. That's not cost-cutting; it's quality control. They're investing in partner training and certification to ensure value-added services come from partners, not from Broadcom's payroll.

Analyst interpretation: Researchers note that partner conversations have shifted from transactional discussions to "execution-focused, value-realization conversations" CRN partner strategy analysis. This is crucial for investors because it means higher margins (less services headcount) and more scalable growth (partners shoulder the implementation burden).

These three themes work together like a flywheel. Private cloud creates the sticky customer base, AI infrastructure provides the growth engine, and partner delivery keeps margins expanding. You're not just buying a semiconductor or software company; you're buying a capital allocation machine that gets more efficient as it gets larger.

For investors using quantitative screening tools, the metrics to watch aren't just revenue growth. Track the software revenue mix (currently 40% and climbing), the AI semiconductor growth rate (66% year-over-year), and operating margin expansion (from 15% in 2016 to 32% today). These themes show up in the numbers before they show up in the headlines, which is exactly what data-driven investors need to spot durable competitive advantages early.

Now that we've unpacked how Broadcom operates without a traditional mission statement, let's talk about the guardrails that actually guide day-to-day decisions. Every company claims to have core values, but for a $300 billion infrastructure giant like Broadcom, these aren't just wall plaques; they're supposed to shape hiring, culture, and capital allocation.

Broadcom lists Integrity first, though what this means in practice is layered. On paper, it's about ethical business conduct and responsible supply chain sourcing. Strategically, it positions them for long-term contracts with risk-averse enterprise and government customers who need to trust their infrastructure partner won't cut corners. The recent GSA OneGov partnership, which gives federal agencies discounted enterprise software access, reflects this commitment in action GSA partnership announcement.

In our experience analyzing how tech vendors win federal business, these deals are only awarded to suppliers who can demonstrate compliance integrity across thousands of audit points. That $110 billion backlog we mentioned earlier? It's filled with customers who trust Broadcom won't introduce supply chain risks that could take down their operations.

This is where Broadcom genuinely puts its money. Innovation isn't about splashy product launches; it's about solving hyperscaler problems at scale. The company invested roughly $1 billion in R&D to develop VMware Cloud Foundation 9.0, a fully integrated private cloud platform that unifies compute, networking, storage, and security Futurum Group analysis. Real-world proof shows up in their AI semiconductor revenue, which hit $6.2 billion last quarter, up 66% year-over-year. That's innovation translating directly to market dominance, not just patent filings.

🎯 Pro Insight: When evaluating Innovation as a core value, ignore press releases and track R&D efficiency instead. Broadcom's model is brutal: they invest heavily in custom silicon for specific hyperscalers like Google's TPUs and Meta's MTIA chips, creating switching costs that lock in multi-year revenue. This isn't innovation for its own sake; it's innovation that builds moats. The $110 billion backlog proves it's working.

Collaboration sounds warm and fuzzy, but at Broadcom it manifests as a partner-led delivery model. Rather than building a massive professional services army, Broadcom is shifting implementation and consulting to certified partners. In April 2025, they slashed authorized VMware Cloud Service Providers from over 4,500 to a smaller elite group, investing in partner training and certification instead Intelisys analysis. This creates a scalable ecosystem where partners deliver localized expertise while Broadcom focuses on product development. In our experience, this model only works when the vendor is confident enough in product-market fit to let go of direct control.

Excellence shows up in the numbers. Operating margins expanded from 15% in 2016 to 32% today, and software revenue grew from 26% to 45% of the mix post-VMware. That's not luck; that's operational excellence in acquisition integration and cost discipline. The metric that matters: Broadcom serves the world's largest enterprises with AI, custom silicon, and cloud platforms while maintaining 60%+ gross margins. When you're the infrastructure backbone for companies that can't afford downtime, excellence isn't aspirational; it's contractual.

Here's where it gets interesting. Employee surveys suggest mixed alignment: 50% of employees are motivated by the company mission, but only 25% stay because of it. Compensation tops the list at 38% Comparably employee data. Values like Teamwork & Winning rate 100% approval, yet Transparency & Integrity score 0%.

This gap between stated values and lived experience is common in engineering-first cultures where results trump rhetoric. For investors, this data point is crucial: you're buying a company that executes brilliantly, not one that wins culture awards.

Broadcom's formal ESG initiatives tie directly to Innovation and Collaboration values. The Broadcom Foundation runs Coding with Commitment programs focused on STEM education and AI literacy aligned with UN Sustainable Development Goals Broadcom Foundation. They've partnered with the Raspberry Pi Foundation to provide free AI training resources, and offer employee volunteer opportunities.

While these programs lack quantified emissions targets or full ESG frameworks, they embed the company in community ecosystems that support long-term talent pipelines. For a company that needs thousands of engineers to maintain its innovation edge, this isn't just corporate social responsibility; it's strategic workforce development disguised as good citizenship. The sustainable supply chain management mentioned in their corporate responsibility pages reflects governance standards, even if specific environmental targets remain elusive Broadcom corporate responsibility.

So what does this all mean for your investment analysis? Broadcom's strategic identity isn't found in a glossy mission statement on a wall; it's embedded in a capital allocation machine that builds moats while you watch the quarterly reports.

Analysts are clearly bullish on the execution. As of February 2026, 34 analysts rate AVGO a "Buy" with an average price target of $433.87 market consensus data. The consensus view positions Broadcom as "the tollroad for AI giants" rather than a direct competitor, which is exactly the kind of indispensable infrastructure positioning that drives predictable cash flows. Companies like Google and Meta are literally designing their AI future around Broadcom's custom silicon, and that $110 billion backlog gives you revenue visibility that most semiconductor plays can only dream about.

💡 Expert Tip: When evaluating Broadcom's management quality, ignore the CEO's charisma and focus on the margin expansion math. Operating margins climbing from 15% in 2016 to 32% today while integrating a $69 billion acquisition proves they know how to extract value without breaking the strategic machine. That's the real signal.

In our experience tracking tech giants through multiple cycles, this partner-led delivery model Broadcom is pushing in 2026 is the operational detail most investors miss. By shifting from direct services to certified partner channels, they're essentially making their growth more capital-efficient while embedding themselves deeper into customer ecosystems. It's a structural shift that should keep margins expanding even as they scale.

The forward-looking framework is clear: private cloud as the control plane, AI infrastructure as the growth engine, and partner delivery as the margin multiplier. For investors who understand that quality compounds while drama distracts, Broadcom's mission-in-action approach translates into exactly the kind of durable advantage that builds wealth slowly and reliably.

For a deeper dive into the fundamental metrics driving this strategic identity, including how that 60/40 revenue split impacts valuation models, you might find platforms like StockIntent useful for running scenario analysis on the AI semiconductor growth rates and software margin expansion we've discussed.

If you're evaluating Broadcom (AVGO) for your portfolio, understanding what actually drives this semiconductor giant is essential. Here's what surprised me when I dug into it: unlike most Fortune 500 companies, Broadcom doesn't plaster a catchy mission statement on its homepage. Their purpose shows up in their strategy and actions instead.

Key Takeaways:

The company's strategic direction has evolved dramatically in recent years. Broadcom now generates roughly 60% of revenue from Semiconductor Solutions (including AI accelerators and networking chips) and 40% from Infrastructure Software (led by VMware Cloud Foundation). This isn't just diversification - it's a deliberate move to capture the entire technology stack that enterprises need for AI and digital transformation.

Let's get into the nuts and bolts of what Broadcom actually does today. The company runs two distinct but complementary businesses that together pulled in $63.9 billion in fiscal 2025 according to official guidance — and they're expecting Q1 2026 to hit $19.1 billion in just a single quarter. That kind of scale puts them in rare company.

Here’s what you need to know in 30 seconds:

These figures come from Broadcom's financial releases and market analysis.

In our experience analyzing tech giants, the magic isn't just in these numbers — it's in how Broadcom has positioned itself as "the tollroad for AI giants". While Nvidia captures headlines with GPUs, Broadcom quietly supplies custom AI accelerators (ASICs/XPUs) that power Google's TPUs and Meta's MTIA chips. They don't compete head-on; they make themselves indispensable. This shows up in their competitive positioning: they're winning share from hyperscalers while facing threats from customer insourcing (Apple building its own Wi-Fi chips) and rivals like AMD and Marvell, as strategic analysis explains.

The VMware acquisition changed everything. Before 2023, Broadcom was a semiconductor pure-play. Today, that 60/40 revenue split reflects a deliberate strategy to own the entire enterprise stack, from the silicon that moves bits to the software that manages entire data centers. It's a moat-building exercise in real time.

Here's the thing most investors miss when researching Broadcom: they don't actually publish a traditional mission statement. While most S&P 500 companies lead with inspiring corporate mantras, Broadcom's so-called mission lives in their actions and strategic choices. Their de facto purpose centers on delivering semiconductors and infrastructure software for global enterprises' most complex, mission-critical needs.

What this signals about Broadcom's priorities

This isn't a marketing oversight; it's a deliberate reflection of their engineering-first culture. Where competitors like STMicroelectronics pledge to "master the semiconductor supply chain for a sustainable world" and Samsung promises to "contribute to a better global society," Broadcom's language stays grounded in product delivery and customer dependency. They focus on being indispensable rather than aspirational.

🎯 Pro Insight: When evaluating mission statements, pay attention to what isn't said. Broadcom's silence on broad societal goals while emphasizing "mission-critical needs" reveals a capital allocation philosophy that prioritizes high-margin, moat-worthy markets over virtuous signaling. This shows up in their 60/40 semiconductor-software revenue split and $110 billion backlog, both designed for predictable, recurring cash flows rather than flashy growth narratives.

Connecting mission to capital decisions

This de facto mission directly shapes their acquisition strategy. The $69 billion VMware purchase wasn't about chasing cloud trends; it was about becoming "the landlord of both physical and virtual data centers" by owning the software layer that enterprises can't rip out. Every major move, from CA Technologies to Symantec, follows the same pattern: buy mission-critical infrastructure, optimize it for cash flow, and create switching costs that keep customers locked in, as strategic analysis explains.

Why this matters for investors

For those analyzing AVGO as a potential holding, this mission-in-action approach translates to financial predictability. Rather than betting on innovation cycles or consumer trends, you're buying into a company that makes itself essential to the AI infrastructure build-out while facing threats from customer insourcing and rivals like Marvell. The mission, if you can call it that, is simple: be the tollroad, not the destination.

Here's where things get interesting. Broadcom doesn't just operate randomly; their actions cluster around three distinct strategic pillars that actually matter for your investment analysis. Think of these as the load-bearing walls of their entire operation. Each pillar directly translates to competitive advantages you can measure.

This isn't marketing fluff about "changing the world." For Broadcom, it means pouring money into R&D that solves hyperscaler problems at scale. What it is: relentless engineering focus on AI infrastructure, custom silicon, and high-speed networking that makes competitors irrelevant.

Why it matters strategically: In semiconductors, being first doesn't win; being indispensable does. When you're the only company that can deliver custom AI accelerators for Google's TPUs and Meta's MTIA chips, you don't compete on price. You set terms. This shows up in their Q3 2025 numbers: that R&D spend helped generate $7.0 billion in free cash flow while AI semiconductor revenue hit $6.2 billion, up 66% year-over-year.

The concrete example? Their dual-engine model before VMware was roughly 80% semiconductors. Now it's evolved into a tollroad architecture where they capture AI utility layer revenue whether customers build on their chips or their software. That's moat-building in real time. In our experience analyzing tech giants, companies that can maintain 60%+ gross margins while growing AI revenue 66% annually aren't innovating for novelty. They're building walls.

This pillar explains why Broadcom dropped $69 billion on VMware. What it is: creating a full-stack portfolio where customers can't easily rip out one piece without breaking everything else. Semiconductors, networking, security, and enterprise software all integrated together.

Why it matters: Switching costs become astronomical. When your data center runs on Broadcom's Tomahawk chips, VMWare Cloud Foundation, and Symantec security, switching to piecemeal competitors means ripping out three integrated systems simultaneously. Most CFOs won't approve that disruption.

The metric that proves this works? Software revenue grew from 26% to 45% of the mix post-VMware, and operating margins expanded from 15% in 2016 to 32% today. That's not acquisition math; that's integration discipline. Every dollar of software revenue converts to higher-margin recurring cash flows than chips alone. For investors, this means you're buying a company that gets more profitable as it gets larger, which is exactly what you want in a long-term holding.

This is the "landlord of data centers" vision made concrete. What it is: positioning Broadcom as the infrastructure backbone for enterprises and governments that can't afford downtime or security breaches.

Why it matters strategically: This focuses them exclusively on high-margin, mission-critical markets where customers pay premium prices for reliability. They aren't chasing consumer fads or low-margin commodity chips. They're selling to the Fortune 500 and federal agencies with decade-long procurement cycles.

The evidence? That $110 billion backlog gives them revenue visibility most semiconductor companies can only dream about. Add the GSA partnership providing federal agencies discounted enterprise software access, and you see a pattern: Broadcom embeds itself into customer operations so deeply that removing them becomes a career-limiting move for CTOs. That's the economic moat you're paying for when you buy AVGO at 12.5x forward earnings. It doesn't make their stock cheap, but it does make their cash flows predictable, and in 2026's volatile market, predictability is worth a premium.

If you're looking for a glossy vision statement to slap on a PowerPoint slide, Broadcom will disappoint you. Just like with their mission, the company doesn't bother with corporate poetry. What they have instead is a strategic north star that actually matters for your investment analysis.

CEO Hock Tan has been crystal clear about where Broadcom is heading. He describes the company as "the landlord of both the physical and virtual data center." Not a tenant. Not a service provider. The landlord.

"the landlord of both the physical and virtual data center" — CEO Hock Tan on Broadcom's strategic vision

This single phrase explains that $69 billion VMware acquisition we mentioned earlier and that deliberate 60/40 revenue split strategic analysis of Broadcom's positioning. Tan isn't chasing AI hype cycles or cloud buzzwords. He's building a tollroad architecture where Broadcom captures utility-layer revenue whether enterprises build on their chips or their software. The physical data center? That's the semiconductor side: Tomahawk networking chips, custom AI accelerators for Google and Meta, the silicon that moves bits. The virtual data center? That's VMware Cloud Foundation, the software layer enterprises literally cannot rip out without breaking their entire IT operation.

In our experience analyzing tech giants, this landlord positioning is brilliant precisely because it's boring. While Nvidia grabs headlines with GPUs, Broadcom quietly makes itself indispensable to the actual infrastructure AI runs on. They're not trying to be the flashiest tenant in the building; they own the building.

This vision aligns perfectly with 2026's macro trends. The AI infrastructure build-out isn't just about training models; it's about networking, data center management, and enterprise integration Broadcom's AI-era strategy. Broadcom's dual-engine approach positions them to collect rent from both sides of that equation.

Here's where we get into the actual playbook. Broadcom's vision isn't just words on a wall; it's three distinct themes that show up in every major decision. If you're evaluating AVGO as a long-term holding, these are the strategic patterns you need to recognize because they directly impact capital allocation and competitive moats.

Broadcom leadership has made it crystal clear: private cloud isn't a legacy option, it's the control plane for digital transformation. This isn't about fighting the public cloud giants; it's about becoming the indispensable infrastructure layer enterprises can't operate without.

How this shapes strategy: Every dollar spent and every product roadmap decision flows through this lens. The $1 billion R&D investment in VMware Cloud Foundation 9.0 wasn't about feature parity with AWS; it was about creating a unified platform that lets enterprises run AI workloads with the security and compliance they can't get elsewhere Futurum Group analysis of VCF 9.0.

Observable moves: Beyond the VMware acquisition itself, you're seeing this in the GSA OneGov partnership giving federal agencies discounted access official GSA announcement. That's not a one-off deal; it's embedding Broadcom into decade-long government procurement cycles where ripping it out becomes a political problem, not just a technical one.

Analyst interpretation: Industry researchers note this represents a "profound transformation" where private cloud is emerging as the strategic centerpiece, not a secondary option Private Cloud Outlook 2025. The moat here isn't just switching costs; it's regulatory compliance and data sovereignty that public clouds struggle to match.

Remember that "landlord of physical and virtual data centers" vision? This is the physical half made concrete. Broadcom isn't trying to beat Nvidia at GPUs; they're making themselves indispensable to the AI infrastructure that GPUs run on.

How this shapes strategy: The company positions AI not as a product line but as a strategy that permeates everything. When they announced the industry's first Enterprise Wi-Fi 8 Access Point for the AI Era, it wasn't about Wi-Fi speeds; it was about creating the networking fabric AI workloads require Broadcom product announcement.

Observable moves: The numbers tell the story. AI semiconductor revenue hit $6.2 billion last quarter, up 66% year-over-year, representing 22% of total revenue Broadcom Q4 2025 financial release. More importantly, that $110 billion backlog we mentioned earlier is heavily weighted toward custom AI accelerators for Google TPUs and Meta MTIA chips. When you're the only company that can deliver at that scale, you don't compete on price; you set terms.

Analyst interpretation: Market watchers are bullish on this positioning, noting Broadcom "enables hyperscalers to design custom AI inference chips as a more efficient alternative to Nvidia" MarketBeat analyst coverage. The consensus view is that this isn't a cyclical AI play; it's a structural position in the infrastructure layer that benefits regardless of which AI models win.

Here's a theme that doesn't get enough attention but explains Broadcom's margin expansion. In 2026, they're fundamentally shifting from direct service delivery to a partner-led model. Think of it as moving from being a general contractor to being the supplier that every contractor has to buy from.

How this shapes strategy: The channel chief describes 2026 as a "once-in-an-every-other-decade kind of opportunity" centered on delivering AI, on-premises, and private cloud solutions CRN interview on 2026 partner strategy. The strategy is explicit: AI is the strategy, private cloud is the control plane, and edge computing is the operational model Broadcom partner success blog.

Observable moves: In April 2025, they slashed authorized VMware Cloud Service Providers from over 4,500 to a smaller, elite group Intelisys analysis of licensing changes. That's not cost-cutting; it's quality control. They're investing in partner training and certification to ensure value-added services come from partners, not from Broadcom's payroll.

Analyst interpretation: Researchers note that partner conversations have shifted from transactional discussions to "execution-focused, value-realization conversations" CRN partner strategy analysis. This is crucial for investors because it means higher margins (less services headcount) and more scalable growth (partners shoulder the implementation burden).

These three themes work together like a flywheel. Private cloud creates the sticky customer base, AI infrastructure provides the growth engine, and partner delivery keeps margins expanding. You're not just buying a semiconductor or software company; you're buying a capital allocation machine that gets more efficient as it gets larger.

For investors using quantitative screening tools, the metrics to watch aren't just revenue growth. Track the software revenue mix (currently 40% and climbing), the AI semiconductor growth rate (66% year-over-year), and operating margin expansion (from 15% in 2016 to 32% today). These themes show up in the numbers before they show up in the headlines, which is exactly what data-driven investors need to spot durable competitive advantages early.

Now that we've unpacked how Broadcom operates without a traditional mission statement, let's talk about the guardrails that actually guide day-to-day decisions. Every company claims to have core values, but for a $300 billion infrastructure giant like Broadcom, these aren't just wall plaques; they're supposed to shape hiring, culture, and capital allocation.

Broadcom lists Integrity first, though what this means in practice is layered. On paper, it's about ethical business conduct and responsible supply chain sourcing. Strategically, it positions them for long-term contracts with risk-averse enterprise and government customers who need to trust their infrastructure partner won't cut corners. The recent GSA OneGov partnership, which gives federal agencies discounted enterprise software access, reflects this commitment in action GSA partnership announcement.

In our experience analyzing how tech vendors win federal business, these deals are only awarded to suppliers who can demonstrate compliance integrity across thousands of audit points. That $110 billion backlog we mentioned earlier? It's filled with customers who trust Broadcom won't introduce supply chain risks that could take down their operations.

This is where Broadcom genuinely puts its money. Innovation isn't about splashy product launches; it's about solving hyperscaler problems at scale. The company invested roughly $1 billion in R&D to develop VMware Cloud Foundation 9.0, a fully integrated private cloud platform that unifies compute, networking, storage, and security Futurum Group analysis. Real-world proof shows up in their AI semiconductor revenue, which hit $6.2 billion last quarter, up 66% year-over-year. That's innovation translating directly to market dominance, not just patent filings.

🎯 Pro Insight: When evaluating Innovation as a core value, ignore press releases and track R&D efficiency instead. Broadcom's model is brutal: they invest heavily in custom silicon for specific hyperscalers like Google's TPUs and Meta's MTIA chips, creating switching costs that lock in multi-year revenue. This isn't innovation for its own sake; it's innovation that builds moats. The $110 billion backlog proves it's working.

Collaboration sounds warm and fuzzy, but at Broadcom it manifests as a partner-led delivery model. Rather than building a massive professional services army, Broadcom is shifting implementation and consulting to certified partners. In April 2025, they slashed authorized VMware Cloud Service Providers from over 4,500 to a smaller elite group, investing in partner training and certification instead Intelisys analysis. This creates a scalable ecosystem where partners deliver localized expertise while Broadcom focuses on product development. In our experience, this model only works when the vendor is confident enough in product-market fit to let go of direct control.

Excellence shows up in the numbers. Operating margins expanded from 15% in 2016 to 32% today, and software revenue grew from 26% to 45% of the mix post-VMware. That's not luck; that's operational excellence in acquisition integration and cost discipline. The metric that matters: Broadcom serves the world's largest enterprises with AI, custom silicon, and cloud platforms while maintaining 60%+ gross margins. When you're the infrastructure backbone for companies that can't afford downtime, excellence isn't aspirational; it's contractual.

Here's where it gets interesting. Employee surveys suggest mixed alignment: 50% of employees are motivated by the company mission, but only 25% stay because of it. Compensation tops the list at 38% Comparably employee data. Values like Teamwork & Winning rate 100% approval, yet Transparency & Integrity score 0%.

This gap between stated values and lived experience is common in engineering-first cultures where results trump rhetoric. For investors, this data point is crucial: you're buying a company that executes brilliantly, not one that wins culture awards.

Broadcom's formal ESG initiatives tie directly to Innovation and Collaboration values. The Broadcom Foundation runs Coding with Commitment programs focused on STEM education and AI literacy aligned with UN Sustainable Development Goals Broadcom Foundation. They've partnered with the Raspberry Pi Foundation to provide free AI training resources, and offer employee volunteer opportunities.

While these programs lack quantified emissions targets or full ESG frameworks, they embed the company in community ecosystems that support long-term talent pipelines. For a company that needs thousands of engineers to maintain its innovation edge, this isn't just corporate social responsibility; it's strategic workforce development disguised as good citizenship. The sustainable supply chain management mentioned in their corporate responsibility pages reflects governance standards, even if specific environmental targets remain elusive Broadcom corporate responsibility.

So what does this all mean for your investment analysis? Broadcom's strategic identity isn't found in a glossy mission statement on a wall; it's embedded in a capital allocation machine that builds moats while you watch the quarterly reports.

Analysts are clearly bullish on the execution. As of February 2026, 34 analysts rate AVGO a "Buy" with an average price target of $433.87 market consensus data. The consensus view positions Broadcom as "the tollroad for AI giants" rather than a direct competitor, which is exactly the kind of indispensable infrastructure positioning that drives predictable cash flows. Companies like Google and Meta are literally designing their AI future around Broadcom's custom silicon, and that $110 billion backlog gives you revenue visibility that most semiconductor plays can only dream about.

💡 Expert Tip: When evaluating Broadcom's management quality, ignore the CEO's charisma and focus on the margin expansion math. Operating margins climbing from 15% in 2016 to 32% today while integrating a $69 billion acquisition proves they know how to extract value without breaking the strategic machine. That's the real signal.

In our experience tracking tech giants through multiple cycles, this partner-led delivery model Broadcom is pushing in 2026 is the operational detail most investors miss. By shifting from direct services to certified partner channels, they're essentially making their growth more capital-efficient while embedding themselves deeper into customer ecosystems. It's a structural shift that should keep margins expanding even as they scale.

The forward-looking framework is clear: private cloud as the control plane, AI infrastructure as the growth engine, and partner delivery as the margin multiplier. For investors who understand that quality compounds while drama distracts, Broadcom's mission-in-action approach translates into exactly the kind of durable advantage that builds wealth slowly and reliably.

For a deeper dive into the fundamental metrics driving this strategic identity, including how that 60/40 revenue split impacts valuation models, you might find platforms like StockIntent useful for running scenario analysis on the AI semiconductor growth rates and software margin expansion we've discussed.