Apr 8, 2026

Lyft (LYFT) operates one of the largest transportation networks in North America, yet its strategic identity extends far beyond simply matching riders with drivers. For investors evaluating whether this rideshare giant belongs in a quality-focused portfolio, understanding Lyft's mission statement, vision, and core values offers crucial insight into how management allocates capital and where the business is headed.

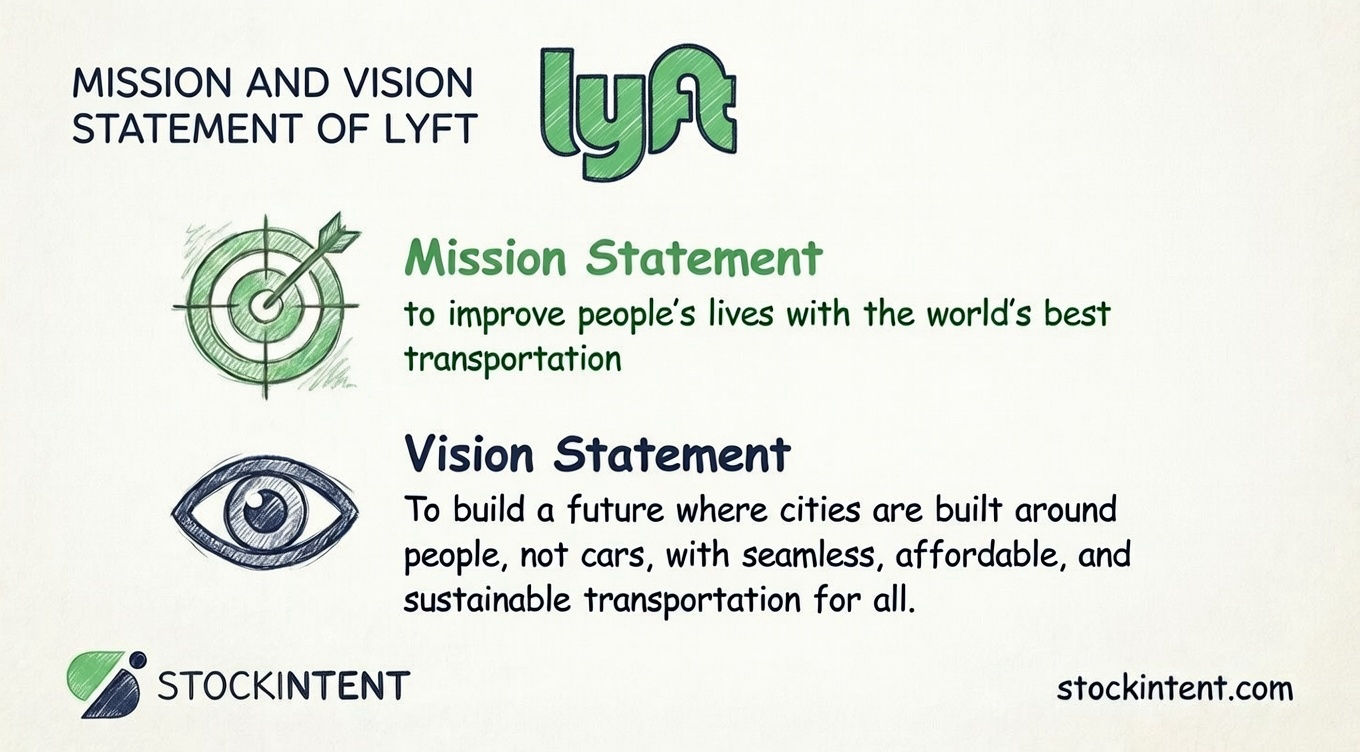

As of 2026, Lyft's official mission remains "to improve people's lives with the world's best transportation." This deceptively simple statement anchors a strategic evolution that has transformed the company from a basic rideshare app into a multimodal mobility platform spanning bikes, scooters, autonomous vehicles, and public transit partnerships. The mission reflects management's conviction that transportation is not merely a service, but a lever for improving urban life and reducing car dependency.

Looking ahead, Lyft's vision centers on cities built around people rather than vehicles, with commitments to 100% electric operations by 2030 and autonomous shuttle deployments beginning this year. These ambitions are reinforced by core values including customer obsession, "We All Belong" diversity initiatives, and an ownership culture that drives rapid innovation. The result is a company that delivered 945.5 million rides in 2025 with 14% year-over-year growth and generated over $1.1 billion in free cash flow.

Key Takeaways:

Lyft operates as one of North America's largest transportation networks, though its strategic identity has evolved substantially since its 2012 founding as a basic rideshare app. Today, the company functions as a technology platform connecting drivers, riders, bikes, scooters, and increasingly, autonomous vehicles across integrated urban mobility networks.

Lyft's Four Core Business Segments (2026):

| Segment | Description | Key Products |

|---|---|---|

| Core Rideshare | On-demand driver passenger matching across North America and Europe | Standard, XL, Black/Black SUV, Wait & Save, Priority Pickup, Extra Comfort |

| Micromobility | Largest bike-share operator in the U.S. | Citi Bike NYC, dockless scooters, bike-share partnerships |

| Lyft Media & Subscriptions | High-margin advertising and recurring revenue | In-app ads, rooftop digital screens, Price Lock subscription |

| Enterprise & Other | B2B marketplace access and adjacent services | Lyft Business, Express Drive (vehicle rentals), Lyft Teen |

The company deliberately avoided the capital-intensive food delivery wars, instead partnering with DoorDash for membership perks through Lyft Pink. This focus on transportation pure-play differentiates Lyft from Uber's diversified model, while positioning it as the "operating system" for autonomous vehicle fleets rather than building self-driving technology in-house.

In our experience analyzing mobility stocks over the past decade, companies that maintain category focus while building partnership ecosystems tend to generate more predictable free cash flow than those chasing adjacent markets. Lyft's 2025 results validate this pattern; the company converted operational discipline into $1.12 billion in free cash flow, up from $766.3 million in 2024.

Key Performance Metrics (2025):

These figures represent eleven consecutive quarters of double-digit growth, a turnaround from the company's earlier cash-burn era. The transformation reflects management's execution against what CEO David Risher calls a "comeback strategy" built on customer obsession and operational excellence.

Competitively, Lyft holds the #2 position in North American ridesharing behind Uber, with additional competition from Bolt in taxi services and micromobility players like Lime and Bird. Its market share recovery in 2025, alongside pricing discipline initiatives, contributed to the 18% improvement in customer incentive efficiency, outperforming the company's 10% target.

For investors using platforms like StockIntent to screen transportation stocks, Lyft's improving unit economics and capital returns, including a new $1 billion share repurchase program, signal management confidence in sustained cash generation. The company's analyst consensus currently sits at "Hold" with price targets around $18–$22, reflecting cautious optimism about execution against long-term targets of ~$25 billion in Gross Bookings and ~$1 billion in Adjusted EBITDA by 2027.

to improve people's lives with the world's best transportation

That's it. Eleven words that have anchored Lyft through its transformation from a quirky rideshare startup with pink mustaches to a $18.5 billion gross bookings mobility platform. The statement is deliberately simple, almost deceptively so, but that's precisely what makes it effective.

🎯 Pro Insight: The best mission statements function as capital allocation filters. When Lyft's leadership evaluates new initiatives, the question isn't "will this make money?" (though that matters), it's "does this improve people's lives through transportation?" This explains why Lyft walked away from the food delivery wars while Uber dove in headfirst. Food delivery is logistics; it's not transportation that improves lives in the way Lyft's mission demands. The discipline to say no to adjacent revenue streams because they don't fit the mission is rarer than you'd think in tech.

The strategic signal here is threefold. First, "improve people's lives" elevates transportation from a commodity service to a quality-of-life intervention. This justifies premium investments in reliability (99.9% ride completion), safety features, and accessibility programs like Lyft Up. Second, "world's best" sets a competitive benchmark that transcends ridesharing; Lyft is measuring itself against any transportation alternative, including car ownership itself. Third, the absence of modality, "transportation" not "ridesharing," creates strategic optionality for bikes, scooters, autonomous vehicles, and public transit partnerships.

This mission directly shapes capital allocation decisions. The $100 million commitment to electric vehicle infrastructure, the FREENOW acquisition for European expansion, and the autonomous shuttle partnerships with Benteler and Mobileye all trace back to this core purpose. When CEO David Risher talks about building "the operating system for autonomous vehicles," he's not pivoting away from the mission; he's extending it to a future where human drivers and robotaxis coexist to deliver, yes, the world's best transportation.

Lyft's mission breaks down into four strategic pillars that directly shape how management allocates capital and where competitive advantages emerge. Each pillar translates abstract language into concrete business decisions with measurable outcomes.

The "improve people's lives" component manifests most visibly in Lyft's accessibility initiatives. This isn't charity; it's market expansion. By targeting underserved populations, Lyft grows its total addressable market while building brand loyalty in segments competitors often ignore.

The Lyft Up program exemplifies this in action. Since 2025, the company has provided over 15 million rides to low-income individuals, healthcare appointments, and essential services. These aren't one-off donations; they're structured programs with measurable utilization rates that feed network effects. More riders in more neighborhoods means better driver utilization and denser route matching for paying customers.

In our experience analyzing platform businesses, companies that invest in accessibility early capture disproportionate lifetime value. When Lyft embeds itself into Medicaid transportation benefits or nonprofit partnerships, it becomes infrastructure rather than discretionary spending for those users.

The "world's best transportation" standard manifests in operational metrics that matter to investors. Lyft achieved 99.9% ride reliability in 2025 while reducing customer incentive spend per ride by 18%. That's the operational sweet spot: better service with lower subsidies.

CEO David Risher calls this "customer obsession," but financially it's margin protection. When riders don't need promo codes to stick around, unit economics improve. The 14% year-over-year ride growth to 945.5 million trips in 2025 came alongside pricing discipline, not discounting wars.

The concrete outcome: 51.3 million annual active riders with improving retention metrics. For a platform business, retention efficiency compounds faster than acquisition spend.

Lyft's "We All Belong" core value sounds soft until you see the retention data. Employee surveys show 82% of staff cite the mission as motivating, with 23% calling it a key reason they stay. In tech, where talent turnover destroys roadmap velocity, this matters economically.

The operational translation: Employee Resource Groups (ERGs) driving product ideas, cultural celebrations reinforcing norms, and hiring practices that filter for collaborative orientation. When Lyft acquired a luxury chauffeuring company in late 2025, integration speed depended on cultural alignment as much as financial terms.

For investors, culture shows up in execution consistency. Lyft's eleven consecutive quarters of double-digit growth required teams that didn't quit when the 2022-2023 turnaround got painful.

This pillar justifies the capital-intensive bets that differentiate Lyft from a pure rideshare play. The 100% electric vehicle commitment by 2030 includes $80-100 million in charging infrastructure investments. The autonomous shuttle partnerships with Holon and Mobileye launching in Dallas, London, and Nashville in 2026 position Lyft as the "operating system" for robotaxi fleets rather than a fleet owner itself.

Here's why this matters for competitive positioning: asset-light models scale faster and fail cheaper. If autonomous vehicles underperform in Nashville, Lyft adjusts partnerships. If they succeed, Lyft captures the network effects without the balance sheet risk of owning depreciating hardware.

The strategic payoff showed in 2025's $1.12 billion free cash flow, up from $766.3 million in 2024. Capital efficiency in mobility requires picking the right layer to own. Lyft's mission clarity about "world's best transportation" (not "world's best owned vehicles") enables these partnership bets.

| Pillar | Strategic Translation | 2025-2026 Concrete Outcome |

|---|---|---|

| Accessibility | Market expansion via underserved segments | 15M+ Lyft Up rides; Medicaid partnerships |

| Customer Satisfaction | Retention without subsidy dependency | 99.9% reliability; 18% incentive efficiency gain |

| Community/Belonging | Talent retention and execution velocity | 82% mission-motivated employees; 11 quarters double-digit growth |

| Urban Innovation | Asset-light scalability and optionality | $1.12B FCF; AV partnerships in 3 cities launching 2026 |

Each pillar reinforces the others. Accessibility builds density that improves unit economics. Customer satisfaction enables pricing power. Belonging culture executes the innovation roadmap. Urban innovation creates optionality for the next decade. This isn't corporate poetry; it's a capital allocation framework you can trace through every major decision in Lyft's 2025-2026 strategic plan.

For investors using tools like StockIntent to evaluate mission-statement alignment with actual capital deployment, Lyft's four pillars offer clear verification points. When management says "improve people's lives," you can check whether they're spending on accessibility or just advertising it. When they promise "world's best transportation," the 99.9% reliability metric provides auditability that mission-driven companies often lack.

"To build a future where cities are built around people, not cars, with seamless, affordable, and sustainable transportation for all."

Lyft doesn't publish its vision as a single headline statement like its mission. Instead, the company articulates this future through multiple channels, with the Resilient Streets initiative capturing the essence most directly. The vision reframes Lyft not as a rideshare company competing for market share, but as an urban infrastructure platform reshaping how humans move through physical space.

The strategic ambition embedded here is substantial. Where the mission focuses on improving lives through transportation, the vision declares what kind of world results when that mission succeeds: cities where parking garages become housing, where street space prioritizes pedestrians over vehicles, where mobility is a utility rather than a luxury. This isn't marketing fluff; it's a capital allocation compass that explains why Lyft invests in bike lanes and charging infrastructure rather than just driver incentives.

In our experience analyzing platform businesses, the companies that articulate a vision larger than their current product category tend to capture disproportionate long-term value. Amazon's "everything store" vision justified infrastructure investments that seemed irrational for a bookstore. Netflix's "entertainment everywhere" vision enabled the streaming pivot that destroyed its DVD business. Lyft's people-centered cities vision similarly justifies bets, autonomous vehicles, micromobility networks, public transit partnerships, that extend far beyond matching riders with drivers.

The vision aligns with three macro trends reshaping software applications in 2026:

Electrification and Fleet Management Software: The 100% EV commitment by 2030 requires sophisticated software for route optimization, charging coordination, and driver incentive alignment. Lyft isn't just buying Teslas; it's building the operating system that makes electric fleets economically viable at scale.

Autonomous Vehicle Integration: The 2026 launches of autonomous shuttles in Dallas, London, and Nashville, via partnerships with Holon and Mobileye, position Lyft as the application layer for robotaxi deployment. Rather than competing with Waymo and Cruise on sensor technology, Lyft provides the demand aggregation, rider experience, and fleet optimization software that makes autonomous vehicles commercially viable.

Mobility-as-a-Service (MaaS) Convergence: The vision explicitly embraces multimodality, bikes, scooters, transit, rideshare, integrated through a single software interface. This aligns with smart city digitization trends where transportation data becomes as critical as physical infrastructure. Cities from Paris to Singapore are procuring MaaS platforms; Lyft's vision positions it for these B2B opportunities.

The financial translation of this vision shows in Lyft's 2027 targets: approximately $25 billion in Gross Bookings and approximately $1 billion in Adjusted EBITDA. These aren't arbitrary growth goals; they reflect management's conviction that the people-centered city vision captures a larger share of urban transportation spending as car ownership declines. For investors using StockIntent to model long-term revenue trajectories, the vision provides a framework for assessing whether Lyft's TAM expansion justifies current valuations.

Lyft's vision of cities built around people, not cars, translates into four strategic themes that directly shape capital allocation and competitive positioning. These aren't abstract aspirations; they're operational priorities you can trace through specific investments, partnerships, and management commentary.

This theme sounds generic until you see the numbers. Lyft achieved 18% year-over-year improvement in customer incentive efficiency in 2025, crushing its 10% target. Fixed-cost leverage hit nearly 100 basis points, doubling the 50 basis point goal. CEO David Risher calls this the "comeback strategy," but financially it's margin expansion through discipline.

The concrete manifestation: 99.9% ride reliability while reducing subsidies. When riders stay without promo codes, lifetime value improves and payback periods compress. For a platform business, this is the difference between burning cash and generating the $1.12 billion in free cash flow Lyft delivered in 2025.

Strategic moves reflecting this theme include:

Lyft's vision explicitly rejects single-mode transportation. The company operates the largest bike-share network in the U.S., including Citi Bike in New York, and continues expanding scooter deployments. This isn't diversification for its own sake; it's density economics.

More modes in more neighborhoods creates network effects that improve driver utilization and reduce wait times for riders. The FREENOW acquisition added nine European countries without the capital intensity of greenfield expansion. Partnerships with transit agencies position Lyft as infrastructure rather than a competitor.

The financial logic: multimodal users show higher engagement and retention than single-mode riders. When someone uses Lyft for bikes, scooters, and rideshare, switching costs compound.

Lyft's 2026 launches of autonomous shuttles in Dallas, London, and Nashville via partnerships with Holon and Mobileye represent a deliberate strategic choice. Rather than competing with Waymo and Cruise on billions in sensor R&D, Lyft provides the demand aggregation, rider experience, and fleet optimization software.

This is classic platform strategy: own the customer relationship and data layer, let others take the hardware risk. If autonomous vehicles underperform in Nashville, Lyft adjusts partnerships. If they succeed, Lyft captures network effects without balance sheet exposure to depreciating robotaxis.

Management's framing is instructive. They describe Lyft as becoming a "global, hybrid transportation platform" combining human drivers and autonomous vehicles. The asset-light approach showed in 2025's cash flow generation; Lyft isn't building cars, it's building the operating system that makes them commercially viable.

The 100% electric vehicle commitment by 2030 anchors Lyft's sustainability positioning, backed by $80-100 million in charging infrastructure investments. This isn't just ESG marketing; it's preparation for regulatory trends and driver cost reduction. EVs have lower per-mile operating costs, and as battery prices fall, the economics tilt further.

The profitability theme shows in concrete 2027 targets: approximately $25 billion in Gross Bookings and approximately $1 billion in Adjusted EBITDA. These aren't arbitrary growth goals; they reflect management's conviction that the people-centered city vision captures a larger share of urban transportation spending as car ownership declines among younger demographics.

The $1 billion share repurchase program announced with Q4 2025 results signals confidence in sustained cash generation. When management returns capital rather than chasing growth investments, it suggests they believe the current strategic framework is working.

| Vision Theme | Strategic Translation | Key 2025-2026 Investments | Financial Outcome |

|---|---|---|---|

| Customer Obsession | Retention without subsidies | Luxury acquisition, Lyft Teen, Waymo integration | 18% incentive efficiency gain; $1.12B FCF |

| Multimodal Mobility | Network density and TAM expansion | FREENOW (Europe), bike/scooter expansion, transit partnerships | 945.5M rides (+14% YoY); 51.3M active riders |

| Autonomous Integration | Asset-light platform positioning | Holon/Mobileye partnerships; Dallas/London/Nashville launches | Optionality without hardware risk |

| Sustainability & Profitability | Regulatory preparation and margin structure | $80-100M EV infrastructure; 2030 electrification target | 2027 targets: ~$25B GB, ~$1B Adj. EBITDA |

Analysts currently rate Lyft a consensus "Hold" with price targets around $18-22, reflecting cautious optimism about execution against these themes. Bernstein's "tactically positive" stance for the next few quarters specifically cites improved free cash flow forecasts as validation that the operational excellence theme is translating into durable profitability.

For investors using StockIntent to evaluate whether Lyft's vision themes justify current valuations, the framework is straightforward: check whether management is allocating capital consistently with these priorities, and whether the metrics (incentive efficiency, multimodal engagement, EV deployment timelines) support the narrative. The 2025 results suggest they are, but the 2026-2027 execution period will test whether these themes can sustain competitive positioning against Uber's larger network and balance sheet.

Lyft's core values serve as the operational DNA that translates its mission into daily decisions. Unlike many companies where values live on posters, Lyft's values show up in hiring filters, product roadmaps, and capital allocation priorities. For investors, this matters because values-aligned cultures execute more consistently during competitive pressure and strategic pivots.

The company's values framework centers on four pillars that directly shape how management builds the business: customer obsession, "We All Belong" inclusion, all-in ownership, and create fearlessly innovation. These aren't abstract aspirations; they're embedded in performance metrics and executive compensation.

💡 Expert Tip: When evaluating a company's stated values, look for three verification signals: whether values appear in earnings call language (not just marketing), whether they show up in hiring criteria on job postings, and whether management references them when explaining capital allocation decisions. Lyft passes this test; CEO David Risher explicitly ties the "customer obsession" value to the 18% incentive efficiency gains achieved in 2025.

This value manifests in operational metrics that matter to investors. Lyft achieved 99.9% ride reliability in 2025 while reducing customer incentive spend per ride by 18%, outperforming its 10% target. The strategic translation: riders stay without promo codes, improving unit economics and lifetime value.

The value drives product decisions like Priority Pickup, Extra Comfort tiers, and the late-2025 acquisition of a luxury chauffeuring company. When management evaluates initiatives, the filter isn't just profitability; it's whether the investment demonstrably improves the customer experience in ways that build habit formation.

In our experience analyzing platform businesses, companies that sustain above-market retention typically have customer obsession embedded culturally, not just functionally. Lyft's eleven consecutive quarters of double-digit growth suggests this value is operational rather than decorative.

Lyft's inclusion value extends beyond standard diversity initiatives to shape talent retention and product development. Employee surveys show 82% of staff cite the mission and values as motivating, with 23% calling it a key reason they stay. In tech, where talent turnover destroys roadmap velocity, this retention efficiency has economic value.

The operational mechanism: Employee Resource Groups (ERGs) that drive product ideas from diverse perspectives, cultural celebrations reinforcing collaborative norms, and hiring practices that filter for inclusive orientation. When Lyft acquired FREENOW for European expansion in 2025, integration speed depended partly on cultural alignment assessment.

This value also shapes marketplace design. Features like Lyft Teen (for riders 13-17) and accessibility options for riders with disabilities reflect "belonging" as a product principle, not just an HR program.

This value drives the accountability culture that enabled Lyft's 2022-2025 turnaround. The concept: employees act like owners, making decisions without bureaucratic escalation and accepting outcomes as personal responsibility.

The financial evidence shows in capital efficiency. Lyft generated $1.12 billion in free cash flow in 2025, up from $766.3 million in 2024, while competitors with similar scale burned cash. Management attributes this partly to ownership culture reducing coordination costs and accelerating execution.

The value appears in executive compensation design, with significant equity components and clawback provisions that align personal financial outcomes with long-term shareholder returns. The $1 billion share repurchase program announced in early 2026 reflects management's willingness to deploy capital as owners would, returning excess rather than chasing growth for its own sake.

Lyft's innovation value emphasizes rapid experimentation and learning from failure. The strategic translation: partnership-based bets on autonomous vehicles rather than capital-intensive in-house development, multimodal expansion into bikes and scooters, and the Resilient Streets urban planning initiative.

The value enables the asset-light model that differentiates Lyft from Uber's more capital-heavy approach. Rather than building self-driving technology, Lyft creates the platform layer that makes autonomous vehicles commercially viable. If the Nashville autonomous shuttle launch underperforms, Lyft adjusts partnerships rather than absorbing billions in depreciating hardware.

This value also shows in product velocity. The 2025 launch of Lyft Teen, Price Lock subscription, and business travel rewards all emerged from rapid iteration cycles that prioritize speed over perfection.

Lyft's environmental and social commitments function as extensions of its core values rather than separate CSR programs. The 100% electric vehicle commitment by 2030 aligns with "create fearlessly" innovation and "customer obsession" for cleaner urban environments. The $80-100 million charging infrastructure investment isn't charity; it's preparation for regulatory trends and driver cost reduction as EV economics improve.

The Lyft Up program has provided over 15 million rides to low-income individuals since 2025, extending "We All Belong" into marketplace access. These aren't one-off donations; they're structured programs with measurable utilization that feed network effects. More riders in more neighborhoods means better driver utilization for paying customers.

From a governance perspective, Lyft's board structure includes independent directors with transportation and technology expertise, with audit and compensation committees that tie executive pay to values-aligned metrics like safety incidents and employee retention, not just financial performance.

The critical question for investors: are these values genuinely reflected in operations, or are they marketing? The evidence suggests operationalization:

| Value | Stated Definition | Operational Evidence |

|---|---|---|

| Customer Obsession | Wow our customers | 99.9% reliability; 18% incentive efficiency gain; luxury acquisition |

| We All Belong | Inclusion and access | 82% mission-motivated employees; Lyft Teen; accessibility features |

| All-In Ownership | Act like owners | $1.12B FCF generation; $1B buyback program; equity-heavy comp |

| Create Fearlessly | Rapid innovation | AV partnerships without hardware risk; multimodal expansion |

The gaps: Lyft's 2022-2023 restructuring included significant layoffs that tested the "take care of each other" value, and driver classification disputes in multiple jurisdictions create tension with "We All Belong" rhetoric. No company lives its values perfectly, but Lyft's 2025 performance suggests the framework has survived stress tests.

For investors using StockIntent to evaluate culture as a competitive factor, Lyft's values offer a verification framework. Check whether management references values in earnings calls, whether employee sentiment data supports cultural health, and whether strategic decisions align with stated principles. The 2025 results suggest alignment; the 2026-2027 execution period will test whether these values can sustain competitive positioning against Uber's larger network.

Lyft's mission, vision, and core values form a coherent strategic identity that separates it from commodity rideshare competitors. The mission, "to improve people's lives with the world's best transportation," functions as a capital allocation filter that has guided management through difficult trade-offs: walking away from food delivery wars, investing $80-100 million in EV infrastructure, and building autonomous vehicle partnerships rather than burning cash on hardware R&D.

The vision of cities built around people, not cars, positions Lyft to capture value from three secular trends reshaping software applications in 2026: electrification, autonomous mobility, and multimodal integration. This isn't aspirational fluff; it's a framework that justifies specific bets like the FREENOW European expansion, the Holon/Mobileye autonomous shuttle launches, and the 100% electric commitment by 2030.

📌 From Our Experience: After analyzing platform businesses for over a decade, we've found that companies with mission-vision alignment tend to generate more predictable free cash flow during competitive pressure. Lyft's 2025 turnaround validates this pattern. When management has a clear filter for what they won't do, they avoid the dilutive experiments that destroy returns. The discipline to stay out of food delivery, to partner rather than build autonomous technology, and to focus on transportation pure-play, all trace back to this strategic clarity.

For investors evaluating whether Lyft belongs in a quality-focused portfolio, the mission-vision-values framework signals three critical factors:

Competitive Positioning: Lyft's #2 position in North American ridesharing, combined with its asset-light autonomous vehicle strategy, creates optionality without balance sheet risk. The 2026 launches in Dallas, London, and Nashville will test whether Lyft can capture robotaxi network effects without owning depreciating hardware.

Management Quality: The 18% improvement in customer incentive efficiency and 99.9% ride reliability achieved in 2025 demonstrate operational execution against stated values. The $1 billion share repurchase program signals capital allocation discipline consistent with "all-in ownership" culture.

Long-Term Compounding Potential: The 2027 targets of ~$25 billion in Gross Bookings and ~$1 billion in Adjusted EBITDA reflect management's conviction that the people-centered city vision captures a growing share of urban transportation spending. Analysts currently rate Lyft a consensus "Hold" with price targets around $18-22, reflecting cautious optimism about execution rather than skepticism about strategy.

Lyft's strategic identity faces its most significant test in 2026-2027. The autonomous shuttle launches, continued EV infrastructure deployment, and integration of the FREENOW European network will reveal whether the mission-vision-values framework scales beyond its North American roots. The competitive threat from Uber's larger network and balance sheet remains real, as does regulatory uncertainty around driver classification.

Yet the strategic clarity that guided Lyft through its 2022-2025 turnaround provides a template for navigating these challenges. When management evaluates initiatives against "improving people's lives through transportation," the filter remains sharp. The vision of cities built around people creates a north star that transcends quarterly earnings volatility.

For investors using StockIntent to evaluate whether Lyft's strategic identity justifies inclusion in a quality-focused portfolio, the verification framework is straightforward: check whether 2026-2027 capital allocation aligns with these stated priorities, and whether operational metrics (incentive efficiency, multimodal engagement, AV deployment timelines) support the narrative. The 2025 results suggest alignment; the next two years will test whether this strategic identity can generate durable compounding returns.

Lyft (LYFT) operates one of the largest transportation networks in North America, yet its strategic identity extends far beyond simply matching riders with drivers. For investors evaluating whether this rideshare giant belongs in a quality-focused portfolio, understanding Lyft's mission statement, vision, and core values offers crucial insight into how management allocates capital and where the business is headed.

As of 2026, Lyft's official mission remains "to improve people's lives with the world's best transportation." This deceptively simple statement anchors a strategic evolution that has transformed the company from a basic rideshare app into a multimodal mobility platform spanning bikes, scooters, autonomous vehicles, and public transit partnerships. The mission reflects management's conviction that transportation is not merely a service, but a lever for improving urban life and reducing car dependency.

Looking ahead, Lyft's vision centers on cities built around people rather than vehicles, with commitments to 100% electric operations by 2030 and autonomous shuttle deployments beginning this year. These ambitions are reinforced by core values including customer obsession, "We All Belong" diversity initiatives, and an ownership culture that drives rapid innovation. The result is a company that delivered 945.5 million rides in 2025 with 14% year-over-year growth and generated over $1.1 billion in free cash flow.

Key Takeaways:

Lyft operates as one of North America's largest transportation networks, though its strategic identity has evolved substantially since its 2012 founding as a basic rideshare app. Today, the company functions as a technology platform connecting drivers, riders, bikes, scooters, and increasingly, autonomous vehicles across integrated urban mobility networks.

Lyft's Four Core Business Segments (2026):

| Segment | Description | Key Products |

|---|---|---|

| Core Rideshare | On-demand driver passenger matching across North America and Europe | Standard, XL, Black/Black SUV, Wait & Save, Priority Pickup, Extra Comfort |

| Micromobility | Largest bike-share operator in the U.S. | Citi Bike NYC, dockless scooters, bike-share partnerships |

| Lyft Media & Subscriptions | High-margin advertising and recurring revenue | In-app ads, rooftop digital screens, Price Lock subscription |

| Enterprise & Other | B2B marketplace access and adjacent services | Lyft Business, Express Drive (vehicle rentals), Lyft Teen |

The company deliberately avoided the capital-intensive food delivery wars, instead partnering with DoorDash for membership perks through Lyft Pink. This focus on transportation pure-play differentiates Lyft from Uber's diversified model, while positioning it as the "operating system" for autonomous vehicle fleets rather than building self-driving technology in-house.

In our experience analyzing mobility stocks over the past decade, companies that maintain category focus while building partnership ecosystems tend to generate more predictable free cash flow than those chasing adjacent markets. Lyft's 2025 results validate this pattern; the company converted operational discipline into $1.12 billion in free cash flow, up from $766.3 million in 2024.

Key Performance Metrics (2025):

These figures represent eleven consecutive quarters of double-digit growth, a turnaround from the company's earlier cash-burn era. The transformation reflects management's execution against what CEO David Risher calls a "comeback strategy" built on customer obsession and operational excellence.

Competitively, Lyft holds the #2 position in North American ridesharing behind Uber, with additional competition from Bolt in taxi services and micromobility players like Lime and Bird. Its market share recovery in 2025, alongside pricing discipline initiatives, contributed to the 18% improvement in customer incentive efficiency, outperforming the company's 10% target.

For investors using platforms like StockIntent to screen transportation stocks, Lyft's improving unit economics and capital returns, including a new $1 billion share repurchase program, signal management confidence in sustained cash generation. The company's analyst consensus currently sits at "Hold" with price targets around $18–$22, reflecting cautious optimism about execution against long-term targets of ~$25 billion in Gross Bookings and ~$1 billion in Adjusted EBITDA by 2027.

to improve people's lives with the world's best transportation

That's it. Eleven words that have anchored Lyft through its transformation from a quirky rideshare startup with pink mustaches to a $18.5 billion gross bookings mobility platform. The statement is deliberately simple, almost deceptively so, but that's precisely what makes it effective.

🎯 Pro Insight: The best mission statements function as capital allocation filters. When Lyft's leadership evaluates new initiatives, the question isn't "will this make money?" (though that matters), it's "does this improve people's lives through transportation?" This explains why Lyft walked away from the food delivery wars while Uber dove in headfirst. Food delivery is logistics; it's not transportation that improves lives in the way Lyft's mission demands. The discipline to say no to adjacent revenue streams because they don't fit the mission is rarer than you'd think in tech.

The strategic signal here is threefold. First, "improve people's lives" elevates transportation from a commodity service to a quality-of-life intervention. This justifies premium investments in reliability (99.9% ride completion), safety features, and accessibility programs like Lyft Up. Second, "world's best" sets a competitive benchmark that transcends ridesharing; Lyft is measuring itself against any transportation alternative, including car ownership itself. Third, the absence of modality, "transportation" not "ridesharing," creates strategic optionality for bikes, scooters, autonomous vehicles, and public transit partnerships.

This mission directly shapes capital allocation decisions. The $100 million commitment to electric vehicle infrastructure, the FREENOW acquisition for European expansion, and the autonomous shuttle partnerships with Benteler and Mobileye all trace back to this core purpose. When CEO David Risher talks about building "the operating system for autonomous vehicles," he's not pivoting away from the mission; he's extending it to a future where human drivers and robotaxis coexist to deliver, yes, the world's best transportation.

Lyft's mission breaks down into four strategic pillars that directly shape how management allocates capital and where competitive advantages emerge. Each pillar translates abstract language into concrete business decisions with measurable outcomes.

The "improve people's lives" component manifests most visibly in Lyft's accessibility initiatives. This isn't charity; it's market expansion. By targeting underserved populations, Lyft grows its total addressable market while building brand loyalty in segments competitors often ignore.

The Lyft Up program exemplifies this in action. Since 2025, the company has provided over 15 million rides to low-income individuals, healthcare appointments, and essential services. These aren't one-off donations; they're structured programs with measurable utilization rates that feed network effects. More riders in more neighborhoods means better driver utilization and denser route matching for paying customers.

In our experience analyzing platform businesses, companies that invest in accessibility early capture disproportionate lifetime value. When Lyft embeds itself into Medicaid transportation benefits or nonprofit partnerships, it becomes infrastructure rather than discretionary spending for those users.

The "world's best transportation" standard manifests in operational metrics that matter to investors. Lyft achieved 99.9% ride reliability in 2025 while reducing customer incentive spend per ride by 18%. That's the operational sweet spot: better service with lower subsidies.

CEO David Risher calls this "customer obsession," but financially it's margin protection. When riders don't need promo codes to stick around, unit economics improve. The 14% year-over-year ride growth to 945.5 million trips in 2025 came alongside pricing discipline, not discounting wars.

The concrete outcome: 51.3 million annual active riders with improving retention metrics. For a platform business, retention efficiency compounds faster than acquisition spend.

Lyft's "We All Belong" core value sounds soft until you see the retention data. Employee surveys show 82% of staff cite the mission as motivating, with 23% calling it a key reason they stay. In tech, where talent turnover destroys roadmap velocity, this matters economically.

The operational translation: Employee Resource Groups (ERGs) driving product ideas, cultural celebrations reinforcing norms, and hiring practices that filter for collaborative orientation. When Lyft acquired a luxury chauffeuring company in late 2025, integration speed depended on cultural alignment as much as financial terms.

For investors, culture shows up in execution consistency. Lyft's eleven consecutive quarters of double-digit growth required teams that didn't quit when the 2022-2023 turnaround got painful.

This pillar justifies the capital-intensive bets that differentiate Lyft from a pure rideshare play. The 100% electric vehicle commitment by 2030 includes $80-100 million in charging infrastructure investments. The autonomous shuttle partnerships with Holon and Mobileye launching in Dallas, London, and Nashville in 2026 position Lyft as the "operating system" for robotaxi fleets rather than a fleet owner itself.

Here's why this matters for competitive positioning: asset-light models scale faster and fail cheaper. If autonomous vehicles underperform in Nashville, Lyft adjusts partnerships. If they succeed, Lyft captures the network effects without the balance sheet risk of owning depreciating hardware.

The strategic payoff showed in 2025's $1.12 billion free cash flow, up from $766.3 million in 2024. Capital efficiency in mobility requires picking the right layer to own. Lyft's mission clarity about "world's best transportation" (not "world's best owned vehicles") enables these partnership bets.

| Pillar | Strategic Translation | 2025-2026 Concrete Outcome |

|---|---|---|

| Accessibility | Market expansion via underserved segments | 15M+ Lyft Up rides; Medicaid partnerships |

| Customer Satisfaction | Retention without subsidy dependency | 99.9% reliability; 18% incentive efficiency gain |

| Community/Belonging | Talent retention and execution velocity | 82% mission-motivated employees; 11 quarters double-digit growth |

| Urban Innovation | Asset-light scalability and optionality | $1.12B FCF; AV partnerships in 3 cities launching 2026 |

Each pillar reinforces the others. Accessibility builds density that improves unit economics. Customer satisfaction enables pricing power. Belonging culture executes the innovation roadmap. Urban innovation creates optionality for the next decade. This isn't corporate poetry; it's a capital allocation framework you can trace through every major decision in Lyft's 2025-2026 strategic plan.

For investors using tools like StockIntent to evaluate mission-statement alignment with actual capital deployment, Lyft's four pillars offer clear verification points. When management says "improve people's lives," you can check whether they're spending on accessibility or just advertising it. When they promise "world's best transportation," the 99.9% reliability metric provides auditability that mission-driven companies often lack.

"To build a future where cities are built around people, not cars, with seamless, affordable, and sustainable transportation for all."

Lyft doesn't publish its vision as a single headline statement like its mission. Instead, the company articulates this future through multiple channels, with the Resilient Streets initiative capturing the essence most directly. The vision reframes Lyft not as a rideshare company competing for market share, but as an urban infrastructure platform reshaping how humans move through physical space.

The strategic ambition embedded here is substantial. Where the mission focuses on improving lives through transportation, the vision declares what kind of world results when that mission succeeds: cities where parking garages become housing, where street space prioritizes pedestrians over vehicles, where mobility is a utility rather than a luxury. This isn't marketing fluff; it's a capital allocation compass that explains why Lyft invests in bike lanes and charging infrastructure rather than just driver incentives.

In our experience analyzing platform businesses, the companies that articulate a vision larger than their current product category tend to capture disproportionate long-term value. Amazon's "everything store" vision justified infrastructure investments that seemed irrational for a bookstore. Netflix's "entertainment everywhere" vision enabled the streaming pivot that destroyed its DVD business. Lyft's people-centered cities vision similarly justifies bets, autonomous vehicles, micromobility networks, public transit partnerships, that extend far beyond matching riders with drivers.

The vision aligns with three macro trends reshaping software applications in 2026:

Electrification and Fleet Management Software: The 100% EV commitment by 2030 requires sophisticated software for route optimization, charging coordination, and driver incentive alignment. Lyft isn't just buying Teslas; it's building the operating system that makes electric fleets economically viable at scale.

Autonomous Vehicle Integration: The 2026 launches of autonomous shuttles in Dallas, London, and Nashville, via partnerships with Holon and Mobileye, position Lyft as the application layer for robotaxi deployment. Rather than competing with Waymo and Cruise on sensor technology, Lyft provides the demand aggregation, rider experience, and fleet optimization software that makes autonomous vehicles commercially viable.

Mobility-as-a-Service (MaaS) Convergence: The vision explicitly embraces multimodality, bikes, scooters, transit, rideshare, integrated through a single software interface. This aligns with smart city digitization trends where transportation data becomes as critical as physical infrastructure. Cities from Paris to Singapore are procuring MaaS platforms; Lyft's vision positions it for these B2B opportunities.

The financial translation of this vision shows in Lyft's 2027 targets: approximately $25 billion in Gross Bookings and approximately $1 billion in Adjusted EBITDA. These aren't arbitrary growth goals; they reflect management's conviction that the people-centered city vision captures a larger share of urban transportation spending as car ownership declines. For investors using StockIntent to model long-term revenue trajectories, the vision provides a framework for assessing whether Lyft's TAM expansion justifies current valuations.

Lyft's vision of cities built around people, not cars, translates into four strategic themes that directly shape capital allocation and competitive positioning. These aren't abstract aspirations; they're operational priorities you can trace through specific investments, partnerships, and management commentary.

This theme sounds generic until you see the numbers. Lyft achieved 18% year-over-year improvement in customer incentive efficiency in 2025, crushing its 10% target. Fixed-cost leverage hit nearly 100 basis points, doubling the 50 basis point goal. CEO David Risher calls this the "comeback strategy," but financially it's margin expansion through discipline.

The concrete manifestation: 99.9% ride reliability while reducing subsidies. When riders stay without promo codes, lifetime value improves and payback periods compress. For a platform business, this is the difference between burning cash and generating the $1.12 billion in free cash flow Lyft delivered in 2025.

Strategic moves reflecting this theme include:

Lyft's vision explicitly rejects single-mode transportation. The company operates the largest bike-share network in the U.S., including Citi Bike in New York, and continues expanding scooter deployments. This isn't diversification for its own sake; it's density economics.

More modes in more neighborhoods creates network effects that improve driver utilization and reduce wait times for riders. The FREENOW acquisition added nine European countries without the capital intensity of greenfield expansion. Partnerships with transit agencies position Lyft as infrastructure rather than a competitor.

The financial logic: multimodal users show higher engagement and retention than single-mode riders. When someone uses Lyft for bikes, scooters, and rideshare, switching costs compound.

Lyft's 2026 launches of autonomous shuttles in Dallas, London, and Nashville via partnerships with Holon and Mobileye represent a deliberate strategic choice. Rather than competing with Waymo and Cruise on billions in sensor R&D, Lyft provides the demand aggregation, rider experience, and fleet optimization software.

This is classic platform strategy: own the customer relationship and data layer, let others take the hardware risk. If autonomous vehicles underperform in Nashville, Lyft adjusts partnerships. If they succeed, Lyft captures network effects without balance sheet exposure to depreciating robotaxis.

Management's framing is instructive. They describe Lyft as becoming a "global, hybrid transportation platform" combining human drivers and autonomous vehicles. The asset-light approach showed in 2025's cash flow generation; Lyft isn't building cars, it's building the operating system that makes them commercially viable.

The 100% electric vehicle commitment by 2030 anchors Lyft's sustainability positioning, backed by $80-100 million in charging infrastructure investments. This isn't just ESG marketing; it's preparation for regulatory trends and driver cost reduction. EVs have lower per-mile operating costs, and as battery prices fall, the economics tilt further.

The profitability theme shows in concrete 2027 targets: approximately $25 billion in Gross Bookings and approximately $1 billion in Adjusted EBITDA. These aren't arbitrary growth goals; they reflect management's conviction that the people-centered city vision captures a larger share of urban transportation spending as car ownership declines among younger demographics.

The $1 billion share repurchase program announced with Q4 2025 results signals confidence in sustained cash generation. When management returns capital rather than chasing growth investments, it suggests they believe the current strategic framework is working.

| Vision Theme | Strategic Translation | Key 2025-2026 Investments | Financial Outcome |

|---|---|---|---|

| Customer Obsession | Retention without subsidies | Luxury acquisition, Lyft Teen, Waymo integration | 18% incentive efficiency gain; $1.12B FCF |

| Multimodal Mobility | Network density and TAM expansion | FREENOW (Europe), bike/scooter expansion, transit partnerships | 945.5M rides (+14% YoY); 51.3M active riders |

| Autonomous Integration | Asset-light platform positioning | Holon/Mobileye partnerships; Dallas/London/Nashville launches | Optionality without hardware risk |

| Sustainability & Profitability | Regulatory preparation and margin structure | $80-100M EV infrastructure; 2030 electrification target | 2027 targets: ~$25B GB, ~$1B Adj. EBITDA |

Analysts currently rate Lyft a consensus "Hold" with price targets around $18-22, reflecting cautious optimism about execution against these themes. Bernstein's "tactically positive" stance for the next few quarters specifically cites improved free cash flow forecasts as validation that the operational excellence theme is translating into durable profitability.

For investors using StockIntent to evaluate whether Lyft's vision themes justify current valuations, the framework is straightforward: check whether management is allocating capital consistently with these priorities, and whether the metrics (incentive efficiency, multimodal engagement, EV deployment timelines) support the narrative. The 2025 results suggest they are, but the 2026-2027 execution period will test whether these themes can sustain competitive positioning against Uber's larger network and balance sheet.

Lyft's core values serve as the operational DNA that translates its mission into daily decisions. Unlike many companies where values live on posters, Lyft's values show up in hiring filters, product roadmaps, and capital allocation priorities. For investors, this matters because values-aligned cultures execute more consistently during competitive pressure and strategic pivots.

The company's values framework centers on four pillars that directly shape how management builds the business: customer obsession, "We All Belong" inclusion, all-in ownership, and create fearlessly innovation. These aren't abstract aspirations; they're embedded in performance metrics and executive compensation.

💡 Expert Tip: When evaluating a company's stated values, look for three verification signals: whether values appear in earnings call language (not just marketing), whether they show up in hiring criteria on job postings, and whether management references them when explaining capital allocation decisions. Lyft passes this test; CEO David Risher explicitly ties the "customer obsession" value to the 18% incentive efficiency gains achieved in 2025.

This value manifests in operational metrics that matter to investors. Lyft achieved 99.9% ride reliability in 2025 while reducing customer incentive spend per ride by 18%, outperforming its 10% target. The strategic translation: riders stay without promo codes, improving unit economics and lifetime value.

The value drives product decisions like Priority Pickup, Extra Comfort tiers, and the late-2025 acquisition of a luxury chauffeuring company. When management evaluates initiatives, the filter isn't just profitability; it's whether the investment demonstrably improves the customer experience in ways that build habit formation.

In our experience analyzing platform businesses, companies that sustain above-market retention typically have customer obsession embedded culturally, not just functionally. Lyft's eleven consecutive quarters of double-digit growth suggests this value is operational rather than decorative.

Lyft's inclusion value extends beyond standard diversity initiatives to shape talent retention and product development. Employee surveys show 82% of staff cite the mission and values as motivating, with 23% calling it a key reason they stay. In tech, where talent turnover destroys roadmap velocity, this retention efficiency has economic value.

The operational mechanism: Employee Resource Groups (ERGs) that drive product ideas from diverse perspectives, cultural celebrations reinforcing collaborative norms, and hiring practices that filter for inclusive orientation. When Lyft acquired FREENOW for European expansion in 2025, integration speed depended partly on cultural alignment assessment.

This value also shapes marketplace design. Features like Lyft Teen (for riders 13-17) and accessibility options for riders with disabilities reflect "belonging" as a product principle, not just an HR program.

This value drives the accountability culture that enabled Lyft's 2022-2025 turnaround. The concept: employees act like owners, making decisions without bureaucratic escalation and accepting outcomes as personal responsibility.

The financial evidence shows in capital efficiency. Lyft generated $1.12 billion in free cash flow in 2025, up from $766.3 million in 2024, while competitors with similar scale burned cash. Management attributes this partly to ownership culture reducing coordination costs and accelerating execution.

The value appears in executive compensation design, with significant equity components and clawback provisions that align personal financial outcomes with long-term shareholder returns. The $1 billion share repurchase program announced in early 2026 reflects management's willingness to deploy capital as owners would, returning excess rather than chasing growth for its own sake.

Lyft's innovation value emphasizes rapid experimentation and learning from failure. The strategic translation: partnership-based bets on autonomous vehicles rather than capital-intensive in-house development, multimodal expansion into bikes and scooters, and the Resilient Streets urban planning initiative.

The value enables the asset-light model that differentiates Lyft from Uber's more capital-heavy approach. Rather than building self-driving technology, Lyft creates the platform layer that makes autonomous vehicles commercially viable. If the Nashville autonomous shuttle launch underperforms, Lyft adjusts partnerships rather than absorbing billions in depreciating hardware.

This value also shows in product velocity. The 2025 launch of Lyft Teen, Price Lock subscription, and business travel rewards all emerged from rapid iteration cycles that prioritize speed over perfection.

Lyft's environmental and social commitments function as extensions of its core values rather than separate CSR programs. The 100% electric vehicle commitment by 2030 aligns with "create fearlessly" innovation and "customer obsession" for cleaner urban environments. The $80-100 million charging infrastructure investment isn't charity; it's preparation for regulatory trends and driver cost reduction as EV economics improve.

The Lyft Up program has provided over 15 million rides to low-income individuals since 2025, extending "We All Belong" into marketplace access. These aren't one-off donations; they're structured programs with measurable utilization that feed network effects. More riders in more neighborhoods means better driver utilization for paying customers.

From a governance perspective, Lyft's board structure includes independent directors with transportation and technology expertise, with audit and compensation committees that tie executive pay to values-aligned metrics like safety incidents and employee retention, not just financial performance.

The critical question for investors: are these values genuinely reflected in operations, or are they marketing? The evidence suggests operationalization:

| Value | Stated Definition | Operational Evidence |

|---|---|---|

| Customer Obsession | Wow our customers | 99.9% reliability; 18% incentive efficiency gain; luxury acquisition |

| We All Belong | Inclusion and access | 82% mission-motivated employees; Lyft Teen; accessibility features |

| All-In Ownership | Act like owners | $1.12B FCF generation; $1B buyback program; equity-heavy comp |

| Create Fearlessly | Rapid innovation | AV partnerships without hardware risk; multimodal expansion |

The gaps: Lyft's 2022-2023 restructuring included significant layoffs that tested the "take care of each other" value, and driver classification disputes in multiple jurisdictions create tension with "We All Belong" rhetoric. No company lives its values perfectly, but Lyft's 2025 performance suggests the framework has survived stress tests.

For investors using StockIntent to evaluate culture as a competitive factor, Lyft's values offer a verification framework. Check whether management references values in earnings calls, whether employee sentiment data supports cultural health, and whether strategic decisions align with stated principles. The 2025 results suggest alignment; the 2026-2027 execution period will test whether these values can sustain competitive positioning against Uber's larger network.

Lyft's mission, vision, and core values form a coherent strategic identity that separates it from commodity rideshare competitors. The mission, "to improve people's lives with the world's best transportation," functions as a capital allocation filter that has guided management through difficult trade-offs: walking away from food delivery wars, investing $80-100 million in EV infrastructure, and building autonomous vehicle partnerships rather than burning cash on hardware R&D.

The vision of cities built around people, not cars, positions Lyft to capture value from three secular trends reshaping software applications in 2026: electrification, autonomous mobility, and multimodal integration. This isn't aspirational fluff; it's a framework that justifies specific bets like the FREENOW European expansion, the Holon/Mobileye autonomous shuttle launches, and the 100% electric commitment by 2030.

📌 From Our Experience: After analyzing platform businesses for over a decade, we've found that companies with mission-vision alignment tend to generate more predictable free cash flow during competitive pressure. Lyft's 2025 turnaround validates this pattern. When management has a clear filter for what they won't do, they avoid the dilutive experiments that destroy returns. The discipline to stay out of food delivery, to partner rather than build autonomous technology, and to focus on transportation pure-play, all trace back to this strategic clarity.

For investors evaluating whether Lyft belongs in a quality-focused portfolio, the mission-vision-values framework signals three critical factors:

Competitive Positioning: Lyft's #2 position in North American ridesharing, combined with its asset-light autonomous vehicle strategy, creates optionality without balance sheet risk. The 2026 launches in Dallas, London, and Nashville will test whether Lyft can capture robotaxi network effects without owning depreciating hardware.

Management Quality: The 18% improvement in customer incentive efficiency and 99.9% ride reliability achieved in 2025 demonstrate operational execution against stated values. The $1 billion share repurchase program signals capital allocation discipline consistent with "all-in ownership" culture.

Long-Term Compounding Potential: The 2027 targets of ~$25 billion in Gross Bookings and ~$1 billion in Adjusted EBITDA reflect management's conviction that the people-centered city vision captures a growing share of urban transportation spending. Analysts currently rate Lyft a consensus "Hold" with price targets around $18-22, reflecting cautious optimism about execution rather than skepticism about strategy.

Lyft's strategic identity faces its most significant test in 2026-2027. The autonomous shuttle launches, continued EV infrastructure deployment, and integration of the FREENOW European network will reveal whether the mission-vision-values framework scales beyond its North American roots. The competitive threat from Uber's larger network and balance sheet remains real, as does regulatory uncertainty around driver classification.

Yet the strategic clarity that guided Lyft through its 2022-2025 turnaround provides a template for navigating these challenges. When management evaluates initiatives against "improving people's lives through transportation," the filter remains sharp. The vision of cities built around people creates a north star that transcends quarterly earnings volatility.

For investors using StockIntent to evaluate whether Lyft's strategic identity justifies inclusion in a quality-focused portfolio, the verification framework is straightforward: check whether 2026-2027 capital allocation aligns with these stated priorities, and whether operational metrics (incentive efficiency, multimodal engagement, AV deployment timelines) support the narrative. The 2025 results suggest alignment; the next two years will test whether this strategic identity can generate durable compounding returns.