Apr 7, 2026

When you're evaluating a defense contractor for your portfolio, the numbers matter, but so does the story behind them. Northrop Grumman (NYSE: NOC) has quietly become one of the most strategically positioned players in aerospace and defense, with a $42 billion revenue run rate and a backlog that keeps growing. But what actually drives this company? Understanding the northrop grumman mission statement and how it shapes capital allocation, program selection, and competitive positioning can give you an edge that pure financial analysis misses.

Let's cut through the corporate speak and look at what Northrop Grumman actually stands for, where it's headed, and why that matters for investors thinking about the long game.

Founded in 1994 through the merger of Northrop and Grumman, this company has evolved into one of the most formidable defense industrial bases in the world. Today, Northrop Grumman operates as a premier aerospace and defense contractor with a clear focus: developing the technologies that define tomorrow's battlefields, from undersea systems to outer space and cyberspace.

In our experience tracking defense contractors over the past decade, companies with concentrated exposure to multi-decade programs tend to outperform those chasing short-term contracts. Northrop Grumman's positioning fits this mold exceptionally well.

The company organizes around four core business segments, each with distinct competitive dynamics:

| Segment | 2025 Revenue | Key Programs | Growth Outlook |

|---|---|---|---|

| Aeronautics Systems | ~$14.2B | B-21 Raider, F-35, airborneISR | Accelerating production |

| Space Systems | $10.8B | PWSA satellites, SLS boosters, missile defense | Rebounding to 5% growth in Q4 2025 |

| Mission Systems | ~$11.5B | Sensors, cyber, electronic warfare | Steady, program-based |

| Defense Systems | ~$5.5B | Advanced weapons, ammunition, hypersonics | Expanding capacity |

The B-21 Raider program deserves special attention. After securing a deal in February 2026 to accelerate production by 25%, Northrop Grumman now has visibility on what could become a $200+ billion program over its lifecycle. The company has invested over $5 billion in digital engineering infrastructure specifically to support this platform, creating manufacturing capabilities that competitors would struggle to replicate.

On the space side, the Proliferated Warfighter Space Architecture represents a fundamental shift in how the Pentagon approaches satellite constellations. Northrop Grumman secured a $764 million contract in December 2025 to build 18 satellites for Tranche 3, with commitments to deliver 150 satellites across the Transport and Tracking layers. This positions them to capture recurring revenue in a domain where CEO Kathy Warden notes space has "evolved into a warfighting domain."

Here's where Northrop Grumman stands as of early 2026:

The backlog figure matters more than most investors realize. In defense, funded backlog equals predictable cash flow conversion. Northrop Grumman's Space Systems segment alone ended 2025 with backlog up 13% to $26.2 billion, suggesting the 8% revenue decline that year was more about program timing than demand weakness.

Within the aerospace & defense landscape, Northrop Grumman occupies a unique niche. Unlike Lockheed Martin's breadth or RTX's diversification, Northrop Grumman has concentrated on becoming the go-to provider for the most technologically demanding, politically sensitive programs: stealth bombers, satellite constellations, nuclear modernization, and missile defense.

📌 From Our Experience: Companies that own the "no one else can do this" contracts tend to earn superior returns on invested capital over time. Northrop Grumman's B-21 and SLS booster programs fit this category. The digital engineering capabilities they've built for B-21 production aren't easily transferable; they represent a decade of accumulated expertise that creates genuine competitive moats.

The analyst consensus reflects this positioning: a Moderate Buy rating with particular enthusiasm around missile defense (approaching 10% of revenue) and the space systems rebound. Citigroup specifically highlighted "stronger production visibility" as a key driver in their 2026 outlook.

For investors evaluating the northrop grumman mission statement and whether it translates to shareholder returns, the evidence suggests the company's focus on "pioneering technologies at the edge of every frontier" isn't just marketing language. It's a capital allocation strategy that directs $13.5 billion in manufacturing and R&D investment toward programs with multi-decade revenue visibility.

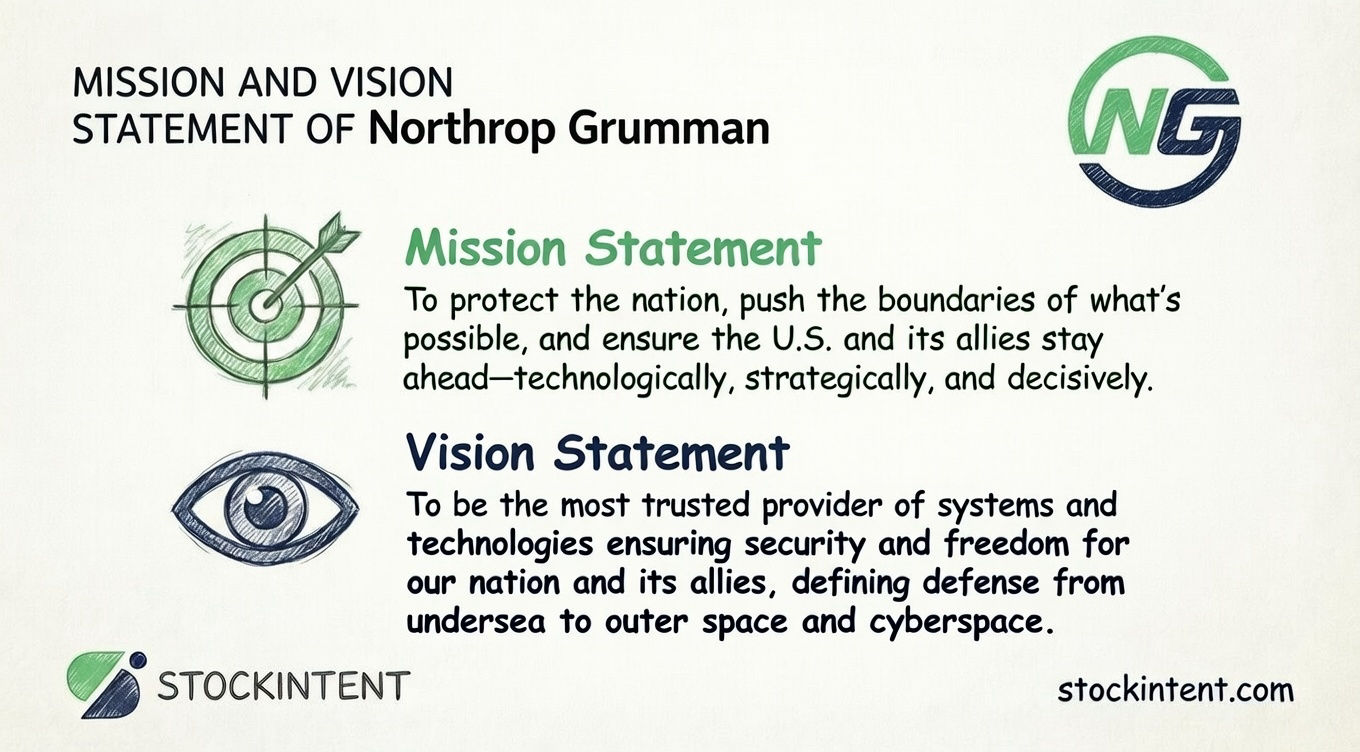

"To protect the nation, push the boundaries of what's possible, and ensure the U.S. and its allies stay ahead—technologically, strategically, and decisively."

This isn't corporate wallpaper. When you read Northrop Grumman's official mission statement, you're looking at a declaration of strategic intent that directly shapes how they deploy capital, which programs they chase, and where they build competitive moats.

The phrasing matters. "Protect the nation" anchors them to the U.S. defense budget, the most predictable revenue source in aerospace and defense. "Push the boundaries" signals to investors and employees alike that R&D intensity isn't negotiable; it's the price of admission. And "stay ahead… decisively" frames every capital allocation decision around maintaining technological superiority rather than cost competition.

🎯 Pro Insight: Defense contractors with mission statements emphasizing "protection" and "superiority" tend to win the high-margin, sole-source contracts that others can't bid on. Northrop Grumman's concentration in B-21, nuclear modernization, and classified space programs isn't accidental; it's the operational translation of this mission into business reality.

The mission's emphasis on "technologically, strategically, and decisively" ahead translates into some of the most concentrated R&D spending in the sector. Northrop Grumman has committed $13.5 billion to manufacturing and R&D over five years, with specific allocations to:

This isn't diversification for its own sake. It's mission-aligned concentration in domains where technological edge equals contract visibility.

Compared to broader aerospace & defense peers, Northrop Grumman's mission statement is notably more specific about how they win: through technological superiority rather than scale or diversification. Lockheed Martin's mission emphasizes "global security" broadly; RTX focuses on "connecting and protecting." Northrop Grumman's sharper focus on "pushing boundaries" and staying "decisively" ahead explains their portfolio concentration in the hardest-to-replicate programs.

The mission also signals customer focus. "U.S. and its allies" explicitly frames their international strategy; they're not chasing every export opportunity, but rather deepening integration with Five Eyes partners and key Indo-Pacific allies like Australia and Japan. This selectivity preserves margin and program access.

For investors evaluating northrop grumman mission and vision as investment factors, the mission statement functions as a capital allocation filter. Programs that don't demonstrably advance technological superiority don't get funded. Markets that don't align with allied defense integration don't get pursued. It's a disciplined approach that shows up in the numbers: 25.52% return on equity and a $92.8 billion backlog that provides 2.2 years of revenue visibility.

Northrop Grumman's mission isn't a single slogan on a wall. It's a three-pillar framework that filters every capital allocation decision, program bid, and hiring choice. Understanding these pillars helps you see why certain contracts win, why others never get pursued, and where the real competitive moats live.

In our experience analyzing defense contractors, companies with clearly articulated mission pillars tend to execute more consistently. They say no to more opportunities, which sounds limiting until you realize that focus is what builds the expertise that wins sole-source contracts.

This pillar centers on "We Pioneer" — the relentless push into emerging technologies before they become mainstream defense priorities. It's not about incremental improvements to existing platforms; it's about creating capabilities that don't exist yet.

What this looks like in practice:

Why it matters for investors: Pioneering creates pricing power. When you're the only company that can manufacture something, you don't compete on cost. The $764 million Proliferated Warfighter Space Architecture contract for 18 Tranche 3 satellites wasn't won on lowest bid; it was won because Northrop Grumman had already demonstrated the rapid manufacturing capabilities this program demands.

This pillar translates the pioneering work into reliable, scalable products. Innovation without execution is just expensive experimentation. Northrop Grumman's emphasis on "We Do What We Promise" shows up in program delivery metrics and quality certifications.

Concrete evidence:

| Program | Scale | Quality Metric |

|---|---|---|

| B-21 Raider | 25% production acceleration agreed February 2026 | Digital-first manufacturing reducing defects |

| NASA SLS Boosters | 75% of Artemis mission thrust | 1.3 million+ solid rocket motors delivered over 60 years |

| GEM 63 for ULA | $2 billion+ multi-year contract | Supporting Amazon's Project Kuiper constellation |

| PWSA Satellites | 150 satellites committed across Transport/Tracking layers | $26.2 billion space backlog (up 13% in 2025) |

The ISO 9001:2015 certifications across their facilities aren't bureaucratic checkboxes; they're prerequisites for the classified and mission-critical programs that generate the highest margins. When a program can't afford to fail, customers pay for proven execution.

The third pillar connects everything to the ultimate customer need: deterrence and, if necessary, decisive advantage in conflict. This isn't abstract patriotism; it's a market positioning strategy that aligns Northrop Grumman with the most stable, highest-priority funding sources.

Strategic translation:

CEO Kathy Warden's statement that space has "evolved into a warfighting domain" isn't just rhetoric. It frames the company's $11 billion space business as essential infrastructure rather than discretionary spending.

Each pillar reinforces the others in ways that build sustainable competitive advantages:

Pioneering → High-Quality: The digital engineering capabilities built for B-21 transfer to satellite manufacturing, creating speed and quality advantages in new domains.

High-Quality → Security Mission: Proven execution earns access to classified programs where failure isn't an option. These programs have multi-decade visibility and limited competition.

Security Mission → Pioneering: Alignment with national priorities means funding for the next generation of breakthrough technologies, completing the cycle.

The result is a $92.8 billion backlog that represents roughly 2.2 years of revenue visibility. In a sector where program delays and cancellations are constant risks, this predictability is genuinely rare.

For investors evaluating northrop grumman core values and whether they translate to returns, the evidence is in the capital allocation. The $13.5 billion, 5-year manufacturing and R&D investment plan isn't spread across dozens of initiatives. It's concentrated in the specific capabilities — digital engineering, secure foundries, rapid satellite production — that reinforce these three pillars and widen the moats around their most profitable programs.

"Our vision is to be the most trusted provider of systems and technologies that ensure the security and freedom of our nation and its allies. As the technology leader, we will define the future of defense from undersea to outer space, and in cyberspace."

This vision statement does heavy lifting. It sets the competitive frame, defines the playing field, and tells you exactly how Northrop Grumman intends to win.

Notice the hierarchy: "most trusted provider" comes before "technology leader." In defense contracting, trust is the ultimate currency. Trust gets you sole-source contracts. Trust gets you classified program access. Trust lets you charge premium prices because the customer literally cannot afford for you to fail. The technology leadership follows as the means to earn and keep that trust.

The domain scope is equally deliberate. "Undersea to outer space, and in cyberspace" maps directly to Northrop Grumman's four business segments. They're not claiming to do everything; they're claiming to own the domains where technological complexity creates natural barriers to entry.

Northrop Grumman's leadership has translated this vision into concrete, capital-intensive commitments. The $13.5 billion manufacturing and R&D investment over five years isn't spread evenly; it's concentrated in the capabilities that reinforce their "most trusted provider" positioning:

| Strategic Priority | Investment Focus | Competitive Outcome |

|---|---|---|

| B-21 Raider acceleration | Digital engineering infrastructure ($5B+), production capacity expansion | Sole-source position on $200B+ program lifecycle |

| Proliferated Warfighter Space Architecture | Rapid satellite manufacturing, 150 satellites committed | Recurring revenue in contested space domain |

| Missile defense industrial base | 11 new rocket motor facilities, secure foundries | Capacity where "none exists" for competitors |

| Hypersonics & advanced weapons | Manufacturing scale-up for Glide Phase Interceptor, Next Generation Interceptor | First-mover advantage in pacing threat technologies |

These aren't diversification bets. They're concentrated investments in domains where trust and technological edge compound over decades. The February 2026 deal to accelerate B-21 production by 25% validates the vision in real time; the Air Force is essentially doubling down on Northrop Grumman as the irreplaceable provider for America's next-generation strategic deterrent.

The vision positions Northrop Grumman to capture value from three structural shifts reshaping defense spending in 2026:

1. The return of great power competition. Defense budgets are pivoting from counterinsurgency to peer deterrence. This favors platforms with strategic impact (B-21, nuclear modernization, missile defense) over tactical systems. Northrop Grumman's vision explicitly targets "security and freedom," which maps to the deterrence mission that now dominates Pentagon prioritization.

2. Space as a warfighting domain. CEO Kathy Warden's observation that space has "evolved into a warfighting domain" isn't rhetoric; it's a market thesis. The vision's explicit inclusion of "outer space" positions Northrop Grumman to capture the $11 billion space segment rebound projected for 2026, with backlog already up 13% to $26.2 billion.

3. Industrial base consolidation and reshoring. The vision's emphasis on being "the most trusted provider" aligns with Pentagon efforts to reduce supply chain fragility. Northrop Grumman's 30 million square feet of U.S. manufacturing and two secure foundries represent infrastructure that would take competitors years to replicate.

For investors evaluating the northrop grumman vision statement as a factor in long-term positioning, the evidence suggests this isn't aspirational language. It's a capital allocation framework that directs resources toward the specific capabilities that create sustainable competitive moats. The vision doesn't promise to be biggest; it promises to be most trusted. In defense, that's the difference between commodity contracting and franchise economics.

Northrop Grumman's vision isn't just aspirational language. It's a capital allocation framework that directs $13.5 billion in manufacturing and R&D investment toward specific capabilities that competitors would struggle to replicate. Let's break down the three strategic themes that operationalize this vision, and more importantly, how they show up in actual business decisions.

The vision's emphasis on being "the most trusted provider" requires manufacturing capabilities that can ramp when programs hit production. Northrop Grumman has made this a deliberate, capital-intensive priority.

Concrete evidence this theme is real:

The capital expenditure guidance of $1.65 billion for 2026 (4% of sales) reflects management's conviction that production scale is the differentiator. As we saw earlier, this concentration in manufacturing creates genuine moats; when you're the only company that can deliver at volume, you don't compete on price.

CEO Kathy Warden's observation that space has "evolved into a warfighting domain" isn't rhetoric. It's a market thesis backed by specific program commitments.

How this theme translates to revenue:

| Initiative | Scale | Strategic Significance |

|---|---|---|

| PWSA Tranche 3 satellites | $764M contract for 18 satellites | Rapid manufacturing demonstration for contested LEO operations |

| 150 satellites committed | Across Transport and Tracking layers | Recurring revenue in proliferated architecture |

| Space backlog growth | Up 13% to $26.2B in 2025 | Revenue visibility despite 2025 segment softness |

| GEM 63 for ULA/Amazon Kuiper | $2B+ multi-year contract | Commercial space diversification |

The 8% space revenue decline in 2025 was a timing issue, not a demand problem. The backlog growth and 2026 guidance for $11 billion in space sales (with 5% growth returning in Q4 2025) confirm this theme is playing out as planned.

Northrop Grumman's vision explicitly targets security for "our nation and its allies." This translates into a strategic priority that might seem counterintuitive for profit-maximization: strengthening the broader defense industrial base even when it benefits competitors.

Why this creates long-term value:

The 2018 Orbital ATK acquisition for $9.2 billion established the "high ground" in satellites and missiles that this theme depends on. Building on that foundation with the 2026 Embraer partnership for KC-390 enhancements shows how the vision continues to shape capital deployment decisions.

Industry coverage validates that these aren't just internal talking points. Citigroup's reiteration of a Buy rating specifically cited "stronger production visibility" as a key driver. The consensus Moderate Buy rating reflects confidence that Northrop Grumman's strategic direction aligns with where defense spending is heading.

Analysts particularly highlight the compounding effect: B-21 acceleration, space re-acceleration maturing by 2027, and international wins create multiple growth vectors. The disciplined approach to capex and margins, despite these growth investments, suggests management is executing the vision without losing financial discipline.

For investors evaluating the northrop grumman strategic vision as an investment factor, the evidence suggests these themes create sustainable competitive advantages. Production scale, space domain expertise, and industrial base positioning aren't easily replicated. They're the result of decade-long capital commitments that competitors would need years to match, if they chose to try at all.

Core values in defense contracting aren't just wall art; they're the filters that determine which programs get pursued, which employees get promoted, and how capital gets allocated when the pressure is on. For investors, understanding whether a company actually lives its stated values, or just posts them on the website, can be the difference between identifying a compounder and catching a value trap.

Northrop Grumman articulates three officially stated core values: We Do the Right Thing, We Do What We Promise, and We Commit to Shared Success. Let's break down what each actually means in practice, how they show up in operations, and whether the evidence supports the claims.

This value centers on integrity, ethical conduct, and doing business the right way even when shortcuts might deliver short-term gains. In the defense sector, where programs span decades and relationships with government customers are everything, reputation for ethical dealing is genuinely valuable.

In practice, this translates to rigorous ethics training (over 99% employee completion in 2024), ISO 9001:2015 quality certifications across facilities, and a Standards of Business Conduct that governs everything from procurement to program bidding. The company also maintains formal corporate responsibility commitments covering environmental stewardship, human rights, and ethical supply chain practices.

💡 Expert Tip: When evaluating defense contractors, look for ethics training completion rates above 95% and whether quality certifications are current and facility-wide. These aren't just compliance checkboxes; they're prerequisites for classified program access and sole-source contracts where failure isn't an option.

The cultural embedding shows up in employee surveys too. Comparably data indicates 62% of employees specifically value transparency and integrity, suggesting the message resonates beyond mandatory training modules. That said, we'd like to see higher scores on diversity and inclusion where the same survey shows 0% ranking it as a top priority.

This value speaks to reliability, program execution, and quality delivery. In defense contracting, operational credibility is currency; it determines whether you get the next contract modification or watch a competitor take the follow-on work.

Northrop Grumman's track record here is genuinely impressive. The company has delivered over 1.3 million solid rocket motors across six decades with the quality standards required for human spaceflight. The B-21 Raider program, after years of development, is now accelerating into production with a 25% increase agreed by February 2026. That's not the track record of a company that overpromises and underdelivers.

The ISO certifications aren't decorative. They're operational requirements for the classified and mission-critical programs that generate Northrop Grumman's highest margins. When your customer literally cannot afford program failure, they pay for proven execution.

This third value frames success as collective rather than zero-sum; with employees, partners, suppliers, and communities all benefiting from the company's growth. It's easy to be skeptical of corporate speak here, but there are concrete manifestations.

Northrop Grumman's 30 million square feet of U.S. manufacturing and supplier network investments position the company as a backbone of the defense industrial base. This isn't altruism; it's customer relationship management at the national level. When you're solving your biggest customer's supply chain headache, you tend to win the follow-on work.

The company also emphasizes STEM education partnerships, veteran employment programs, and inclusive supplier development. These initiatives serve dual purposes: building the talent pipeline and demonstrating alignment with government priorities that increasingly emphasize economic development alongside mission capability.

Here's where we get skeptical again. Every major defense contractor posts similar values. The question is whether they filter real decisions or just live in HR slide decks.

The evidence suggests Northrop Grumman's values do shape capital allocation. The $13.5 billion manufacturing and R&D investment over five years isn't spread across pet projects; it's concentrated in the specific capabilities (digital engineering, secure foundries, rapid satellite production) that reinforce "We Do What We Promise" through irreplaceable execution capacity.

Similarly, the selective approach to international markets, prioritizing Five Eyes partners and key Indo-Pacific allies over chasing every export opportunity, reflects "We Do the Right Thing" in practice. They're preserving program access and margin over short-term revenue.

However, we'd note that like most defense contractors, Northrop Grumman's historical record isn't spotless. Wikipedia documents past environmental claims that prompted stronger responses, though we couldn't find specific recent violations in our research. The values framework appears to have strengthened following corporate responsibility initiatives launched in 2008.

📌 From Our Experience: Companies that operationalize values through specific metrics tend to outperform those with aspirational statements. Northrop Grumman's 99%+ ethics training completion and facility-wide ISO certifications suggest values translate to operational discipline. When we've seen defense contractors cut corners on training or quality, it typically shows up in program execution issues 12-18 months later.

Northrop Grumman's corporate responsibility framework extends these core values into formal ESG commitments. Launched in 2008 with an Environmental Sustainability program and EHS Leadership Council, the company maintains Greenhouse Gas Inventory Projects and UK-based sustainability initiatives focused on "safer, more inclusive worlds."

The strategic logic is straightforward: ESG alignment supports the "most trusted provider" positioning in the vision statement. It's increasingly table stakes for government contracts where supply chain resilience and environmental compliance factor into award decisions. The values don't just shape culture; they shape market access.

For investors evaluating whether northrop grumman company values translate to competitive advantage, the evidence suggests these aren't empty promises. They're operational filters that direct capital toward capabilities with multi-decade payoffs and constrain behavior in ways that preserve customer relationships. In a business where trust is the ultimate currency, that's worth understanding.

Northrop Grumman's mission, vision, and core values aren't corporate wallpaper. They're a unified capital allocation framework that has directed $13.5 billion in manufacturing and R&D investment toward capabilities competitors would struggle to replicate.

The mission, to "protect the nation, push the boundaries of what's possible, and ensure the U.S. and its allies stay ahead," filters every program bid. The vision, to be "the most trusted provider of systems and technologies" across every domain from undersea to outer space, sets the competitive frame. And the three core values, We Do the Right Thing, We Do What We Promise, and We Commit to Shared Success, operationalize these ambitions through 99%+ ethics training completion, ISO 9001:2015 certifications, and a $92.8 billion backlog that provides 2.2 years of revenue visibility.

In our experience analyzing defense contractors over the past decade, companies that successfully align mission, vision, and values tend to outperform on execution metrics that matter for long-term compounding: program win rates, sole-source contract retention, and capital efficiency.

🎯 Pro Insight: Analysts currently rate Northrop Grumman a Moderate Buy, with particular enthusiasm around missile defense (approaching 10% of revenue) and the space systems rebound to 5% growth in Q4 2025. Citigroup specifically highlighted "stronger production visibility" as a key driver, reflecting confidence that management's strategic execution aligns with the stated vision. The 25.52% return on equity and EPS of $7.11 (beating expectations) suggest this isn't just analyst optimism; it's showing up in the numbers.

Looking ahead to 2026 and beyond, Northrop Grumman's strategic direction appears remarkably consistent. The February 2026 B-21 production acceleration, the $764 million PWSA satellite contract, and the 11 new rocket motor facilities all represent evolutionary execution of the same mission-vision-values framework rather than strategic pivots. This consistency matters for investors; it suggests management isn't chasing trends but building durable competitive moats in domains where technological edge and customer trust compound over decades.

For investors evaluating whether Northrop Grumman's strategic identity translates to long-term value creation, the evidence suggests these aren't aspirational statements. They're operational filters that direct capital toward programs with multi-decade revenue visibility, constrain behavior in ways that preserve customer relationships, and build the manufacturing infrastructure that makes competitors' entry prohibitively expensive.

If you're looking to dig deeper into Northrop Grumman's fundamentals, valuation metrics, or how it compares to peers in your portfolio, you can try StockIntent's platform totally risk-free for 7 days. The advanced screening tools and pre-built valuation models can help you stress-test whether the strategic story we've outlined here aligns with the financial reality, or identify similar compounders in aerospace & defense that might fit your quality-over-cheapness criteria.

When you're evaluating a defense contractor for your portfolio, the numbers matter, but so does the story behind them. Northrop Grumman (NYSE: NOC) has quietly become one of the most strategically positioned players in aerospace and defense, with a $42 billion revenue run rate and a backlog that keeps growing. But what actually drives this company? Understanding the northrop grumman mission statement and how it shapes capital allocation, program selection, and competitive positioning can give you an edge that pure financial analysis misses.

Let's cut through the corporate speak and look at what Northrop Grumman actually stands for, where it's headed, and why that matters for investors thinking about the long game.

Founded in 1994 through the merger of Northrop and Grumman, this company has evolved into one of the most formidable defense industrial bases in the world. Today, Northrop Grumman operates as a premier aerospace and defense contractor with a clear focus: developing the technologies that define tomorrow's battlefields, from undersea systems to outer space and cyberspace.

In our experience tracking defense contractors over the past decade, companies with concentrated exposure to multi-decade programs tend to outperform those chasing short-term contracts. Northrop Grumman's positioning fits this mold exceptionally well.

The company organizes around four core business segments, each with distinct competitive dynamics:

| Segment | 2025 Revenue | Key Programs | Growth Outlook |

|---|---|---|---|

| Aeronautics Systems | ~$14.2B | B-21 Raider, F-35, airborneISR | Accelerating production |

| Space Systems | $10.8B | PWSA satellites, SLS boosters, missile defense | Rebounding to 5% growth in Q4 2025 |

| Mission Systems | ~$11.5B | Sensors, cyber, electronic warfare | Steady, program-based |

| Defense Systems | ~$5.5B | Advanced weapons, ammunition, hypersonics | Expanding capacity |

The B-21 Raider program deserves special attention. After securing a deal in February 2026 to accelerate production by 25%, Northrop Grumman now has visibility on what could become a $200+ billion program over its lifecycle. The company has invested over $5 billion in digital engineering infrastructure specifically to support this platform, creating manufacturing capabilities that competitors would struggle to replicate.

On the space side, the Proliferated Warfighter Space Architecture represents a fundamental shift in how the Pentagon approaches satellite constellations. Northrop Grumman secured a $764 million contract in December 2025 to build 18 satellites for Tranche 3, with commitments to deliver 150 satellites across the Transport and Tracking layers. This positions them to capture recurring revenue in a domain where CEO Kathy Warden notes space has "evolved into a warfighting domain."

Here's where Northrop Grumman stands as of early 2026:

The backlog figure matters more than most investors realize. In defense, funded backlog equals predictable cash flow conversion. Northrop Grumman's Space Systems segment alone ended 2025 with backlog up 13% to $26.2 billion, suggesting the 8% revenue decline that year was more about program timing than demand weakness.

Within the aerospace & defense landscape, Northrop Grumman occupies a unique niche. Unlike Lockheed Martin's breadth or RTX's diversification, Northrop Grumman has concentrated on becoming the go-to provider for the most technologically demanding, politically sensitive programs: stealth bombers, satellite constellations, nuclear modernization, and missile defense.

📌 From Our Experience: Companies that own the "no one else can do this" contracts tend to earn superior returns on invested capital over time. Northrop Grumman's B-21 and SLS booster programs fit this category. The digital engineering capabilities they've built for B-21 production aren't easily transferable; they represent a decade of accumulated expertise that creates genuine competitive moats.

The analyst consensus reflects this positioning: a Moderate Buy rating with particular enthusiasm around missile defense (approaching 10% of revenue) and the space systems rebound. Citigroup specifically highlighted "stronger production visibility" as a key driver in their 2026 outlook.

For investors evaluating the northrop grumman mission statement and whether it translates to shareholder returns, the evidence suggests the company's focus on "pioneering technologies at the edge of every frontier" isn't just marketing language. It's a capital allocation strategy that directs $13.5 billion in manufacturing and R&D investment toward programs with multi-decade revenue visibility.

"To protect the nation, push the boundaries of what's possible, and ensure the U.S. and its allies stay ahead—technologically, strategically, and decisively."

This isn't corporate wallpaper. When you read Northrop Grumman's official mission statement, you're looking at a declaration of strategic intent that directly shapes how they deploy capital, which programs they chase, and where they build competitive moats.

The phrasing matters. "Protect the nation" anchors them to the U.S. defense budget, the most predictable revenue source in aerospace and defense. "Push the boundaries" signals to investors and employees alike that R&D intensity isn't negotiable; it's the price of admission. And "stay ahead… decisively" frames every capital allocation decision around maintaining technological superiority rather than cost competition.

🎯 Pro Insight: Defense contractors with mission statements emphasizing "protection" and "superiority" tend to win the high-margin, sole-source contracts that others can't bid on. Northrop Grumman's concentration in B-21, nuclear modernization, and classified space programs isn't accidental; it's the operational translation of this mission into business reality.

The mission's emphasis on "technologically, strategically, and decisively" ahead translates into some of the most concentrated R&D spending in the sector. Northrop Grumman has committed $13.5 billion to manufacturing and R&D over five years, with specific allocations to:

This isn't diversification for its own sake. It's mission-aligned concentration in domains where technological edge equals contract visibility.

Compared to broader aerospace & defense peers, Northrop Grumman's mission statement is notably more specific about how they win: through technological superiority rather than scale or diversification. Lockheed Martin's mission emphasizes "global security" broadly; RTX focuses on "connecting and protecting." Northrop Grumman's sharper focus on "pushing boundaries" and staying "decisively" ahead explains their portfolio concentration in the hardest-to-replicate programs.

The mission also signals customer focus. "U.S. and its allies" explicitly frames their international strategy; they're not chasing every export opportunity, but rather deepening integration with Five Eyes partners and key Indo-Pacific allies like Australia and Japan. This selectivity preserves margin and program access.

For investors evaluating northrop grumman mission and vision as investment factors, the mission statement functions as a capital allocation filter. Programs that don't demonstrably advance technological superiority don't get funded. Markets that don't align with allied defense integration don't get pursued. It's a disciplined approach that shows up in the numbers: 25.52% return on equity and a $92.8 billion backlog that provides 2.2 years of revenue visibility.

Northrop Grumman's mission isn't a single slogan on a wall. It's a three-pillar framework that filters every capital allocation decision, program bid, and hiring choice. Understanding these pillars helps you see why certain contracts win, why others never get pursued, and where the real competitive moats live.

In our experience analyzing defense contractors, companies with clearly articulated mission pillars tend to execute more consistently. They say no to more opportunities, which sounds limiting until you realize that focus is what builds the expertise that wins sole-source contracts.

This pillar centers on "We Pioneer" — the relentless push into emerging technologies before they become mainstream defense priorities. It's not about incremental improvements to existing platforms; it's about creating capabilities that don't exist yet.

What this looks like in practice:

Why it matters for investors: Pioneering creates pricing power. When you're the only company that can manufacture something, you don't compete on cost. The $764 million Proliferated Warfighter Space Architecture contract for 18 Tranche 3 satellites wasn't won on lowest bid; it was won because Northrop Grumman had already demonstrated the rapid manufacturing capabilities this program demands.

This pillar translates the pioneering work into reliable, scalable products. Innovation without execution is just expensive experimentation. Northrop Grumman's emphasis on "We Do What We Promise" shows up in program delivery metrics and quality certifications.

Concrete evidence:

| Program | Scale | Quality Metric |

|---|---|---|

| B-21 Raider | 25% production acceleration agreed February 2026 | Digital-first manufacturing reducing defects |

| NASA SLS Boosters | 75% of Artemis mission thrust | 1.3 million+ solid rocket motors delivered over 60 years |

| GEM 63 for ULA | $2 billion+ multi-year contract | Supporting Amazon's Project Kuiper constellation |

| PWSA Satellites | 150 satellites committed across Transport/Tracking layers | $26.2 billion space backlog (up 13% in 2025) |

The ISO 9001:2015 certifications across their facilities aren't bureaucratic checkboxes; they're prerequisites for the classified and mission-critical programs that generate the highest margins. When a program can't afford to fail, customers pay for proven execution.

The third pillar connects everything to the ultimate customer need: deterrence and, if necessary, decisive advantage in conflict. This isn't abstract patriotism; it's a market positioning strategy that aligns Northrop Grumman with the most stable, highest-priority funding sources.

Strategic translation:

CEO Kathy Warden's statement that space has "evolved into a warfighting domain" isn't just rhetoric. It frames the company's $11 billion space business as essential infrastructure rather than discretionary spending.

Each pillar reinforces the others in ways that build sustainable competitive advantages:

Pioneering → High-Quality: The digital engineering capabilities built for B-21 transfer to satellite manufacturing, creating speed and quality advantages in new domains.

High-Quality → Security Mission: Proven execution earns access to classified programs where failure isn't an option. These programs have multi-decade visibility and limited competition.

Security Mission → Pioneering: Alignment with national priorities means funding for the next generation of breakthrough technologies, completing the cycle.

The result is a $92.8 billion backlog that represents roughly 2.2 years of revenue visibility. In a sector where program delays and cancellations are constant risks, this predictability is genuinely rare.

For investors evaluating northrop grumman core values and whether they translate to returns, the evidence is in the capital allocation. The $13.5 billion, 5-year manufacturing and R&D investment plan isn't spread across dozens of initiatives. It's concentrated in the specific capabilities — digital engineering, secure foundries, rapid satellite production — that reinforce these three pillars and widen the moats around their most profitable programs.

"Our vision is to be the most trusted provider of systems and technologies that ensure the security and freedom of our nation and its allies. As the technology leader, we will define the future of defense from undersea to outer space, and in cyberspace."

This vision statement does heavy lifting. It sets the competitive frame, defines the playing field, and tells you exactly how Northrop Grumman intends to win.

Notice the hierarchy: "most trusted provider" comes before "technology leader." In defense contracting, trust is the ultimate currency. Trust gets you sole-source contracts. Trust gets you classified program access. Trust lets you charge premium prices because the customer literally cannot afford for you to fail. The technology leadership follows as the means to earn and keep that trust.

The domain scope is equally deliberate. "Undersea to outer space, and in cyberspace" maps directly to Northrop Grumman's four business segments. They're not claiming to do everything; they're claiming to own the domains where technological complexity creates natural barriers to entry.

Northrop Grumman's leadership has translated this vision into concrete, capital-intensive commitments. The $13.5 billion manufacturing and R&D investment over five years isn't spread evenly; it's concentrated in the capabilities that reinforce their "most trusted provider" positioning:

| Strategic Priority | Investment Focus | Competitive Outcome |

|---|---|---|

| B-21 Raider acceleration | Digital engineering infrastructure ($5B+), production capacity expansion | Sole-source position on $200B+ program lifecycle |

| Proliferated Warfighter Space Architecture | Rapid satellite manufacturing, 150 satellites committed | Recurring revenue in contested space domain |

| Missile defense industrial base | 11 new rocket motor facilities, secure foundries | Capacity where "none exists" for competitors |

| Hypersonics & advanced weapons | Manufacturing scale-up for Glide Phase Interceptor, Next Generation Interceptor | First-mover advantage in pacing threat technologies |

These aren't diversification bets. They're concentrated investments in domains where trust and technological edge compound over decades. The February 2026 deal to accelerate B-21 production by 25% validates the vision in real time; the Air Force is essentially doubling down on Northrop Grumman as the irreplaceable provider for America's next-generation strategic deterrent.

The vision positions Northrop Grumman to capture value from three structural shifts reshaping defense spending in 2026:

1. The return of great power competition. Defense budgets are pivoting from counterinsurgency to peer deterrence. This favors platforms with strategic impact (B-21, nuclear modernization, missile defense) over tactical systems. Northrop Grumman's vision explicitly targets "security and freedom," which maps to the deterrence mission that now dominates Pentagon prioritization.

2. Space as a warfighting domain. CEO Kathy Warden's observation that space has "evolved into a warfighting domain" isn't rhetoric; it's a market thesis. The vision's explicit inclusion of "outer space" positions Northrop Grumman to capture the $11 billion space segment rebound projected for 2026, with backlog already up 13% to $26.2 billion.

3. Industrial base consolidation and reshoring. The vision's emphasis on being "the most trusted provider" aligns with Pentagon efforts to reduce supply chain fragility. Northrop Grumman's 30 million square feet of U.S. manufacturing and two secure foundries represent infrastructure that would take competitors years to replicate.

For investors evaluating the northrop grumman vision statement as a factor in long-term positioning, the evidence suggests this isn't aspirational language. It's a capital allocation framework that directs resources toward the specific capabilities that create sustainable competitive moats. The vision doesn't promise to be biggest; it promises to be most trusted. In defense, that's the difference between commodity contracting and franchise economics.

Northrop Grumman's vision isn't just aspirational language. It's a capital allocation framework that directs $13.5 billion in manufacturing and R&D investment toward specific capabilities that competitors would struggle to replicate. Let's break down the three strategic themes that operationalize this vision, and more importantly, how they show up in actual business decisions.

The vision's emphasis on being "the most trusted provider" requires manufacturing capabilities that can ramp when programs hit production. Northrop Grumman has made this a deliberate, capital-intensive priority.

Concrete evidence this theme is real:

The capital expenditure guidance of $1.65 billion for 2026 (4% of sales) reflects management's conviction that production scale is the differentiator. As we saw earlier, this concentration in manufacturing creates genuine moats; when you're the only company that can deliver at volume, you don't compete on price.

CEO Kathy Warden's observation that space has "evolved into a warfighting domain" isn't rhetoric. It's a market thesis backed by specific program commitments.

How this theme translates to revenue:

| Initiative | Scale | Strategic Significance |

|---|---|---|

| PWSA Tranche 3 satellites | $764M contract for 18 satellites | Rapid manufacturing demonstration for contested LEO operations |

| 150 satellites committed | Across Transport and Tracking layers | Recurring revenue in proliferated architecture |

| Space backlog growth | Up 13% to $26.2B in 2025 | Revenue visibility despite 2025 segment softness |

| GEM 63 for ULA/Amazon Kuiper | $2B+ multi-year contract | Commercial space diversification |

The 8% space revenue decline in 2025 was a timing issue, not a demand problem. The backlog growth and 2026 guidance for $11 billion in space sales (with 5% growth returning in Q4 2025) confirm this theme is playing out as planned.

Northrop Grumman's vision explicitly targets security for "our nation and its allies." This translates into a strategic priority that might seem counterintuitive for profit-maximization: strengthening the broader defense industrial base even when it benefits competitors.

Why this creates long-term value:

The 2018 Orbital ATK acquisition for $9.2 billion established the "high ground" in satellites and missiles that this theme depends on. Building on that foundation with the 2026 Embraer partnership for KC-390 enhancements shows how the vision continues to shape capital deployment decisions.

Industry coverage validates that these aren't just internal talking points. Citigroup's reiteration of a Buy rating specifically cited "stronger production visibility" as a key driver. The consensus Moderate Buy rating reflects confidence that Northrop Grumman's strategic direction aligns with where defense spending is heading.

Analysts particularly highlight the compounding effect: B-21 acceleration, space re-acceleration maturing by 2027, and international wins create multiple growth vectors. The disciplined approach to capex and margins, despite these growth investments, suggests management is executing the vision without losing financial discipline.

For investors evaluating the northrop grumman strategic vision as an investment factor, the evidence suggests these themes create sustainable competitive advantages. Production scale, space domain expertise, and industrial base positioning aren't easily replicated. They're the result of decade-long capital commitments that competitors would need years to match, if they chose to try at all.

Core values in defense contracting aren't just wall art; they're the filters that determine which programs get pursued, which employees get promoted, and how capital gets allocated when the pressure is on. For investors, understanding whether a company actually lives its stated values, or just posts them on the website, can be the difference between identifying a compounder and catching a value trap.

Northrop Grumman articulates three officially stated core values: We Do the Right Thing, We Do What We Promise, and We Commit to Shared Success. Let's break down what each actually means in practice, how they show up in operations, and whether the evidence supports the claims.

This value centers on integrity, ethical conduct, and doing business the right way even when shortcuts might deliver short-term gains. In the defense sector, where programs span decades and relationships with government customers are everything, reputation for ethical dealing is genuinely valuable.

In practice, this translates to rigorous ethics training (over 99% employee completion in 2024), ISO 9001:2015 quality certifications across facilities, and a Standards of Business Conduct that governs everything from procurement to program bidding. The company also maintains formal corporate responsibility commitments covering environmental stewardship, human rights, and ethical supply chain practices.

💡 Expert Tip: When evaluating defense contractors, look for ethics training completion rates above 95% and whether quality certifications are current and facility-wide. These aren't just compliance checkboxes; they're prerequisites for classified program access and sole-source contracts where failure isn't an option.

The cultural embedding shows up in employee surveys too. Comparably data indicates 62% of employees specifically value transparency and integrity, suggesting the message resonates beyond mandatory training modules. That said, we'd like to see higher scores on diversity and inclusion where the same survey shows 0% ranking it as a top priority.

This value speaks to reliability, program execution, and quality delivery. In defense contracting, operational credibility is currency; it determines whether you get the next contract modification or watch a competitor take the follow-on work.

Northrop Grumman's track record here is genuinely impressive. The company has delivered over 1.3 million solid rocket motors across six decades with the quality standards required for human spaceflight. The B-21 Raider program, after years of development, is now accelerating into production with a 25% increase agreed by February 2026. That's not the track record of a company that overpromises and underdelivers.

The ISO certifications aren't decorative. They're operational requirements for the classified and mission-critical programs that generate Northrop Grumman's highest margins. When your customer literally cannot afford program failure, they pay for proven execution.

This third value frames success as collective rather than zero-sum; with employees, partners, suppliers, and communities all benefiting from the company's growth. It's easy to be skeptical of corporate speak here, but there are concrete manifestations.

Northrop Grumman's 30 million square feet of U.S. manufacturing and supplier network investments position the company as a backbone of the defense industrial base. This isn't altruism; it's customer relationship management at the national level. When you're solving your biggest customer's supply chain headache, you tend to win the follow-on work.

The company also emphasizes STEM education partnerships, veteran employment programs, and inclusive supplier development. These initiatives serve dual purposes: building the talent pipeline and demonstrating alignment with government priorities that increasingly emphasize economic development alongside mission capability.

Here's where we get skeptical again. Every major defense contractor posts similar values. The question is whether they filter real decisions or just live in HR slide decks.

The evidence suggests Northrop Grumman's values do shape capital allocation. The $13.5 billion manufacturing and R&D investment over five years isn't spread across pet projects; it's concentrated in the specific capabilities (digital engineering, secure foundries, rapid satellite production) that reinforce "We Do What We Promise" through irreplaceable execution capacity.

Similarly, the selective approach to international markets, prioritizing Five Eyes partners and key Indo-Pacific allies over chasing every export opportunity, reflects "We Do the Right Thing" in practice. They're preserving program access and margin over short-term revenue.

However, we'd note that like most defense contractors, Northrop Grumman's historical record isn't spotless. Wikipedia documents past environmental claims that prompted stronger responses, though we couldn't find specific recent violations in our research. The values framework appears to have strengthened following corporate responsibility initiatives launched in 2008.

📌 From Our Experience: Companies that operationalize values through specific metrics tend to outperform those with aspirational statements. Northrop Grumman's 99%+ ethics training completion and facility-wide ISO certifications suggest values translate to operational discipline. When we've seen defense contractors cut corners on training or quality, it typically shows up in program execution issues 12-18 months later.

Northrop Grumman's corporate responsibility framework extends these core values into formal ESG commitments. Launched in 2008 with an Environmental Sustainability program and EHS Leadership Council, the company maintains Greenhouse Gas Inventory Projects and UK-based sustainability initiatives focused on "safer, more inclusive worlds."

The strategic logic is straightforward: ESG alignment supports the "most trusted provider" positioning in the vision statement. It's increasingly table stakes for government contracts where supply chain resilience and environmental compliance factor into award decisions. The values don't just shape culture; they shape market access.

For investors evaluating whether northrop grumman company values translate to competitive advantage, the evidence suggests these aren't empty promises. They're operational filters that direct capital toward capabilities with multi-decade payoffs and constrain behavior in ways that preserve customer relationships. In a business where trust is the ultimate currency, that's worth understanding.

Northrop Grumman's mission, vision, and core values aren't corporate wallpaper. They're a unified capital allocation framework that has directed $13.5 billion in manufacturing and R&D investment toward capabilities competitors would struggle to replicate.

The mission, to "protect the nation, push the boundaries of what's possible, and ensure the U.S. and its allies stay ahead," filters every program bid. The vision, to be "the most trusted provider of systems and technologies" across every domain from undersea to outer space, sets the competitive frame. And the three core values, We Do the Right Thing, We Do What We Promise, and We Commit to Shared Success, operationalize these ambitions through 99%+ ethics training completion, ISO 9001:2015 certifications, and a $92.8 billion backlog that provides 2.2 years of revenue visibility.

In our experience analyzing defense contractors over the past decade, companies that successfully align mission, vision, and values tend to outperform on execution metrics that matter for long-term compounding: program win rates, sole-source contract retention, and capital efficiency.

🎯 Pro Insight: Analysts currently rate Northrop Grumman a Moderate Buy, with particular enthusiasm around missile defense (approaching 10% of revenue) and the space systems rebound to 5% growth in Q4 2025. Citigroup specifically highlighted "stronger production visibility" as a key driver, reflecting confidence that management's strategic execution aligns with the stated vision. The 25.52% return on equity and EPS of $7.11 (beating expectations) suggest this isn't just analyst optimism; it's showing up in the numbers.

Looking ahead to 2026 and beyond, Northrop Grumman's strategic direction appears remarkably consistent. The February 2026 B-21 production acceleration, the $764 million PWSA satellite contract, and the 11 new rocket motor facilities all represent evolutionary execution of the same mission-vision-values framework rather than strategic pivots. This consistency matters for investors; it suggests management isn't chasing trends but building durable competitive moats in domains where technological edge and customer trust compound over decades.

For investors evaluating whether Northrop Grumman's strategic identity translates to long-term value creation, the evidence suggests these aren't aspirational statements. They're operational filters that direct capital toward programs with multi-decade revenue visibility, constrain behavior in ways that preserve customer relationships, and build the manufacturing infrastructure that makes competitors' entry prohibitively expensive.

If you're looking to dig deeper into Northrop Grumman's fundamentals, valuation metrics, or how it compares to peers in your portfolio, you can try StockIntent's platform totally risk-free for 7 days. The advanced screening tools and pre-built valuation models can help you stress-test whether the strategic story we've outlined here aligns with the financial reality, or identify similar compounders in aerospace & defense that might fit your quality-over-cheapness criteria.