Apr 1, 2026

When you're evaluating a restaurant stock for your portfolio, understanding what actually drives the business matters more than the latest menu hype. Wendy's has built its competitive position around a philosophy that dates back to its founding in 1969, but like any mature company, that philosophy has evolved to meet current challenges.

Here's the quick answer: Wendy's official mission centers on exceeding guest expectations through superior quality products and services. The company aims to become the world's most thriving and beloved restaurant brand, supported by five core values that shape everything from menu decisions to franchise relationships. In 2026, this strategic identity is being tested by a major turnaround initiative called Project Fresh.

If you're trying to understand whether Wendy's makes sense as a long-term holding, you need to start with the business itself. Not the Frosty memes or the Twitter account, but the actual economics of running a quick-service restaurant chain in 2026.

Wendy's is a pure-play quick-service restaurant company operating in the consumer cyclical sector. Founded in 1969 by Dave Thomas in Columbus, Ohio, the company built its reputation on a simple but powerful differentiator: fresh, never-frozen beef patties. That quality-first positioning still defines the brand today, even as the restaurant landscape has become far more crowded.

The company operates roughly 7,000 restaurants globally, with approximately 95% owned by franchisees. This asset-light model means Wendy's generates revenue primarily through franchise royalties, real estate, and equipment leasing rather than direct restaurant operations. In our experience analyzing restaurant stocks, this capital structure can create more stable cash flows, but it also means you're betting on franchisee health, not just consumer demand.

As of early 2026, here's what defines Wendy's operations:

The company is currently navigating a challenging period. After reporting an 11.3% decline in U.S. same-restaurant sales in Q4 2025, management launched Project Fresh in October 2025, a comprehensive turnaround initiative aimed at reversing execution failures. The plan includes restaurant closures (roughly 5-6% of underperforming units), menu innovation delays (chicken sandwiches pushed to 2026), and a fundamental reallocation of capital away from restaurant construction toward technology and marketing.

Here's something that matters for your analysis: while U.S. operations struggle, international markets are showing resilience. Global digital sales hit a record 20.3% mix in 2025, and international same-restaurant sales grew 6.2% in Q4 despite the domestic headwinds. This divergence between geographies is worth watching as you evaluate whether Wendy's can execute a simultaneous turnaround at home while scaling abroad.

| Metric | Snapshot |

|---|---|

| Total Restaurants | ~7,000 globally |

| Franchise Mix | 95% franchisee-operated |

| Q4 2025 U.S. Same-Store Sales | (11.3%) |

| Q4 2025 International Same-Store Sales | +6.2% |

| Digital Sales Mix (U.S.) | 20% (up 12.4% YoY) |

| Net Unit Growth Target | 2-3% annually |

The competitive positioning here is nuanced. Wendy's sits in a crowded space between McDonald's (scale dominance), Burger King (value positioning), and Chipotle/Chick-fil-A (quality perception). The company has historically punched above its weight on customer satisfaction, but recent execution missteps, what management described as missing the boat on everyday value while over-relying on limited-time promotions, have dented that advantage. When we look at restaurant turnarounds, the question isn't whether the brand can recover; it's whether management can fix operational execution faster than competitors can capture that market share.

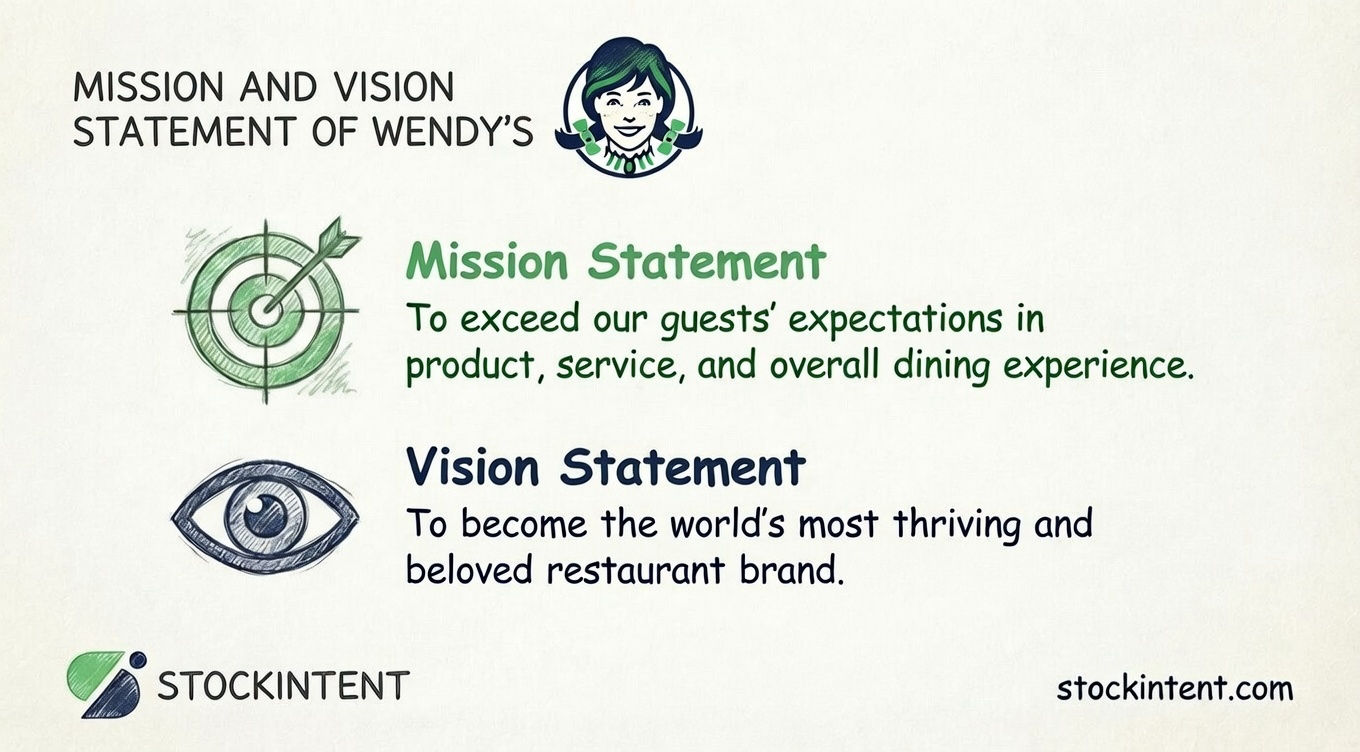

"To exceed our guests' expectations in product, service, and overall dining experience."

That's Wendy's official mission statement, and it reads like something Dave Thomas might have scribbled on a napkin in 1969. Simple, direct, and focused entirely on the customer. No buzzwords about "synergies" or "paradigm shifts." Just a commitment to doing the basics better than anyone else.

But here's what makes this interesting for your analysis: this mission isn't just marketing fluff. It directly shapes how Wendy's allocates capital and makes strategic trade-offs.

🎯 Pro Insight: When evaluating restaurant stocks, we always compare stated mission against actual capital allocation. Wendy's mission prioritizes guest experience over pure efficiency, which explains why they accept higher food costs for fresh beef and why Project Fresh directs $20 million away from new restaurant construction toward technology and marketing. Companies that actually live their mission tend to make more consistent long-term decisions.

The mission's three pillars, product, service, and overall dining experience, map cleanly to Wendy's operational priorities in 2026. Product means the fresh, never-frozen beef positioning that still differentiates them from McDonald's and Burger King. Service covers the digital transformation and operational excellence initiatives under Project Fresh. And "overall dining experience" captures everything from restaurant remodels to the brand revitalization work with Creed UnCo, the consultancy led by former Yum! Brands CEO Greg Creed.

Compare this to McDonald's mission "to be our customers' favorite place and way to eat" or Chick-fil-A's newer "Be REMARKable." Wendy's formulation is more concrete and measurable. You can actually track whether you're exceeding guest expectations through satisfaction scores, same-store sales, and brand perception metrics. "Favorite place" and "remarkable" are harder to quantify, which makes them harder to execute against.

The mission has evolved over time. Earlier versions from the 2000s emphasized "exceeding customer expectations everyday" without the specificity around product and service. A mid-period variant focused on "quality, integrity, and responsibility." The current formulation, which gained prominence around 2024, adds explicit emphasis on innovation and partnerships alongside the core guest focus. This evolution tracks with Wendy's strategic shift from a U.S.-centric operational story to a global growth narrative with digital and sustainability components.

For investors, the mission statement matters because it signals what management won't compromise, even under pressure. When Wendy's reported that 11.3% same-store sales decline in Q4 2025, leadership didn't abandon the quality positioning to chase volume with deep discounting. Instead, they doubled down on operational excellence and system health, accepting near-term pain for what they believe is a stronger long-term position. Whether that discipline creates value or destroys it depends on execution, but at least the strategic compass is clear.

Wendy's mission isn't just a sentence on a poster, it's an operating system that shapes how capital gets deployed and how management makes trade-offs. When we look at restaurant turnarounds, the difference between companies that recover and those that don't often comes down to whether leadership actually runs the business according to stated principles, or just talks about them.

The mission breaks down into three interconnected pillars: exceeding guest expectations, product and service excellence, and delivering a superior overall dining experience. Each pillar has concrete strategic implications and, more importantly for your analysis, measurable outcomes you can track.

This is the foundational pillar that everything else serves. Wendy's doesn't aim to meet industry benchmarks; the explicit goal is to surpass what customers anticipate from a quick-service restaurant. This sounds like generic corporate speak until you look at how it actually shows up in operations.

In our experience analyzing customer satisfaction data across restaurant chains, companies that explicitly target "exceeding expectations" rather than "satisfying customers" tend to invest differently. They spend more on training, accept higher food costs for quality ingredients, and resist the temptation to trade down during tough periods. Wendy's fits this pattern; even during the brutal Q4 2025 when same-store sales collapsed 11.3%, management didn't abandon the fresh beef positioning to chase volume with deep discounting.

The metric that matters here is customer satisfaction relative to competitors. Wendy's has historically punched above its weight here, though recent execution missteps have dented that advantage. When we track restaurant stocks, we watch for divergence between stated mission priorities and actual promotional behavior. Wendy's admitted they "swung too far on promotions" and "missed the boat" on everyday value, which tells you the mission discipline broke down temporarily. Project Fresh is essentially an attempt to rebuild that alignment.

This pillar translates the guest expectation goal into operational specifics. For Wendy's, "product" means the fresh, never-frozen beef positioning that still differentiates them from McDonald's and Burger King. "Service" covers the digital transformation, operational efficiency, and hospitality standards that determine whether the quality promise actually reaches the customer.

The strategic value here is differentiation in a commoditized industry. Quick-service burgers are largely undifferentiated in consumers' minds; the battle is won on convenience, price, and occasional quality perception. Wendy's fresh beef claim gives them a tangible point of difference that supports premium pricing and brand loyalty.

Recent initiatives demonstrating this pillar in action:

| Initiative | What It Is | Why It Matters for Investors |

|---|---|---|

| FreshAI deployment | AI-powered drive-thru and kitchen tools | Labor efficiency + order accuracy improvements that reduce waste and boost throughput |

| Digital sales growth | Mobile app, rewards integration, delivery partnerships | Record 20.3% digital mix in 2025; higher-margin channel with better customer data |

| Menu optimization | Delaying chicken sandwich launches to 2026, focusing on $6 Biggie Bag and $4 Biggie Bites | Discipline over chasing trendy LTOs; building sustainable everyday value position |

| Company store blueprint | U.S. company-operated restaurants outperforming system by 310 bps in 2025 | Proving the operational model works before pushing to franchisees |

The key insight for your analysis: Wendy's is using company-operated stores as a laboratory and proof point. When company stores outperform by 310 basis points (410 bps in Q4), that's not accidental. It shows the operational playbook works when executed with discipline. The problem, and it's a big one, is that only 20% of franchisees have fully adopted these initiatives. This creates a two-tier system where corporate can claim operational excellence while the majority of the system lags.

For investors, this translates to execution risk concentrated in franchisee adoption. You're not betting on whether Wendy's knows what to do; they clearly do. You're betting on whether they can convince independent franchisees to actually do it.

The third pillar broadens the focus from the transaction to the complete brand interaction. This covers restaurant environment, brand perception, community connection, and increasingly, the values alignment that younger consumers expect from the companies they patronize.

Wendy's operationalizes this through their Good Done Right ESG strategy, which organizes commitments into three focus areas: Food (safety, quality, responsible sourcing, waste reduction), People (workplace culture, community giving), and Footprint (packaging, climate, water conservation). These aren't peripheral CSR activities; they're integrated into how Wendy's defines brand strength and long-term competitiveness.

The competitive advantage here is talent attraction and retention in a brutal labor market. Employee surveys show 68% of Wendy's workers are motivated by the mission and vision. That matters when you're trying to staff restaurants in a tight labor environment. It also matters for customer-facing consistency; motivated employees deliver better service.

The strategic positioning against macro trends is worth noting. Quick-service restaurants face pressure on multiple fronts: labor costs, sustainability expectations, health-conscious menus, and digital transformation. Wendy's vision of becoming "the world's most thriving and beloved restaurant brand" explicitly targets leadership in navigating these trends rather than reactive adaptation.

| Trend | Wendy's Response | Moat Implication |

|---|---|---|

| Labor efficiency pressure | AI tools, labor model evolution, training investment | Lower unit labor costs + better service consistency |

| Sustainability demands | Good Done Right commitments, traceable sourcing | Brand permission to operate; risk mitigation |

| Digital transformation | 20% digital mix, app ecosystem, delivery partnerships | Customer data advantage; higher-margin channel mix |

| International expansion | 6.2% Q4 international same-store sales growth; 157 new locations | Diversification away from U.S. headwinds; growth optionality |

For value investors, the critical question is whether these mission pillars translate into durable competitive advantages, what Buffett calls economic moats. Here's our assessment:

Quality differentiation as moat: The fresh beef positioning is real but narrow. It supports premium pricing and brand loyalty, but it's vulnerable to competitor imitation (as we've seen with "fresh" claims from others) and to Wendy's own execution failures. When operations slip, the quality advantage erodes quickly. This is a moat that requires constant maintenance.

Operational excellence as moat: More promising, but currently bifurcated. The company store performance proves the playbook works. If Wendy's can drive franchisee adoption, system-wide efficiency gains create a scale advantage that's hard to replicate. The "One Wendy's" approach to franchisee economics, if successful, builds a network effect moat where the whole system performs better, attracting better franchisees and creating virtuous cycle.

Brand strength as moat: The "beloved brand" vision targets emotional connection that transcends transactional convenience. This is the strongest potential moat but also the hardest to build and easiest to damage. Wendy's social media savvy and quality positioning have created brand permission that competitors lack. The question is whether Project Fresh execution restores that advantage or further erodes it.

The honest assessment: Wendy's mission pillars create conditional competitive advantages that depend heavily on execution. They're not structural moats like Coca-Cola's brand or Microsoft's network effects. They're earned advantages that must be continuously reinvested in and defended. For investors, this means the quality of management execution matters enormously, more than in businesses with deeper structural protections.

When we evaluate restaurant stocks for long-term holding, we look for that combination of clear strategic identity and demonstrated ability to execute. Wendy's has the former in spades. The next 12-18 months will tell us whether they can recover the latter.

"To become the world's most thriving and beloved restaurant brand."

That's the vision that guides Wendy's long-term strategic positioning. Where the mission focuses on day-to-day execution (exceeding guest expectations), the vision sets the destination: global brand leadership measured by both financial performance and customer affection.

The key word here is "thriving." It's not just about being big or well-known; it's about sustainable profitability and system health. This matters for your analysis because it signals that Wendy's management prioritizes franchisee economics and operational health over pure growth metrics. When we evaluate restaurant turnarounds, we look for exactly this kind of discipline; companies that chase unit growth at the expense of system health often end up destroying shareholder value.

The "beloved" piece is equally important. Quick-service restaurants operate in a brutally competitive space where switching costs are essentially zero. Being "liked" isn't enough; you need emotional loyalty that transcends price. Wendy's aims to build this through quality differentiation and brand personality, the same factors that have historically allowed them to command slight pricing premiums over value peers.

Wendy's leadership has articulated several long-term goals that operationalize this vision:

1. Margin expansion through operational excellence

Management has targeted improving company margins by more than 200 basis points by 2028, achieved through P&L benchmarking, productivity upgrades, menu strategy evolution, and technology deployment. This includes making all restaurants "model restaurants" with consistent performance standards, more field support, and dedicated leaders per franchisee.

2. Bold global growth

The vision explicitly targets international expansion, with Wendy's actively seeking new franchise owners to build global presence. In Q4 2025, international same-store sales grew 6.2% while U.S. sales declined 11.3%. This divergence isn't accidental; it's the result of deliberate investment in markets where the brand has permission to grow.

3. Sustainability as competitive moat

The Good Done Right ESG strategy aligns with UN Sustainable Development Goals across food security, sustainable consumption, economic growth, and inequality reduction. For investors, this isn't just CSR theater. It addresses real operating risks (supply chain disruptions, regulatory pressure, talent attraction) while building brand permission with younger consumers who increasingly factor values into purchasing decisions.

The vision positions Wendy's to lead rather than follow major restaurant industry shifts:

| Macro Trend | Wendy's Strategic Response | Vision Alignment |

|---|---|---|

| Sustainability demands | Good Done Right commitments on responsible sourcing, packaging, climate action | "Beloved" brand through values alignment |

| Labor efficiency pressure | AI-powered tools (FreshAI), labor model evolution, training investment | "Thriving" through unit economics improvement |

| Digital transformation | 20.3% digital sales mix, app ecosystem, delivery partnerships | Enhanced customer experience and data advantage |

| International expansion | 6.2% Q4 international growth; 157 new global locations | Global scale toward "world's most thriving" |

| Value-conscious consumers | $6 Biggie Bag, $4 Biggie Bites as permanent value platform | Accessibility supporting "beloved" status |

The honest assessment: Wendy's vision is ambitious but not delusional. It doesn't claim they'll dominate every market or invent new categories. Instead, it targets a specific position, the highest quality choice in quick-service, executed at global scale with sustainable economics. This is achievable if Project Fresh delivers on its operational promises.

For your portfolio analysis, the vision matters because it sets the bounds on what management will and won't do. When evaluating Project Fresh investments, ask whether each initiative builds toward "thriving and beloved" or just chases short-term comps. The vision is your compass for assessing strategic coherence.

Wendy's vision of becoming "the world's most thriving and beloved restaurant brand" isn't just aspirational language, it's a strategic framework that shapes capital allocation, operational priorities, and how management navigates trade-offs. When we analyze restaurant turnarounds, we look for exactly this kind of clarity: a destination that guides decision-making when the path gets messy.

The vision breaks down into four interconnected themes that you'll see reflected in every earnings call and investor presentation. Each theme has concrete metrics and initiatives attached, which is how you separate real strategy from corporate theater.

The "thriving" part of the vision starts with unit economics that actually work. Wendy's has set a target to improve company margins by more than 200 basis points by 2028, achieved through five specific strategies: P&L benchmarking, operations productivity upgrades, menu strategy evolution, technology deployment, and labor model evolution.

Here's what this looks like in practice. In 2025, U.S. company-operated restaurants outperformed the system by 310 basis points (410 bps in Q4), driven by training investments, performance management systems, digital tools like FreshAI, and improved customer satisfaction scores across accuracy, taste, and friendliness. The company is using these locations as a blueprint for franchisee rollout, proving the operational model works before pushing it system-wide.

The catch, and it's a significant one, is adoption velocity. Only 20% of franchisees have fully implemented these initiatives as of early 2026. This creates a two-tier system where corporate can claim operational excellence while the majority of the system lags. For investors, this translates to execution risk concentrated in franchisee relationships, not operational knowledge.

| Operational Initiative | Company Store Performance | Franchisee Adoption | Strategic Implication |

|---|---|---|---|

| FreshAI deployment | Higher throughput, lower waste | ~20% fully adopted | Technology moat requires scale |

| Training programs | +310 bps vs. system average | Rolling out 2026 | Human capital as differentiator |

| Digital integration | 20% sales mix, record highs | Varies by operator | Data advantage requires uniformity |

The "beloved" component of the vision targets emotional loyalty that transcends price competition. Wendy's has reframed its brand essence around being the "highest quality hamburger in QSR," a positioning that guides marketing, menu decisions, operations, and customer experience design.

This isn't just marketing fluff. It directly shapes product strategy. When management admitted they had "swung too far on promotions" and "missed the boat" on everyday value, they weren't abandoning quality to chase volume. Instead, they delayed chicken sandwich launches to 2026 and doubled down on permanent value platforms like the $6 Biggie Bag and $4 Biggie Bites. The discipline here is notable: accepting near-term sales pain to avoid diluting the quality positioning that supports long-term pricing power.

The company also brought in Creed UnCo, led by former Yum! Brands CEO Greg Creed, to transform marketing effectiveness. This signals serious commitment to brand building rather than incremental tweaks. When you see a company hiring outside expertise at the CEO level for marketing, it usually means they recognize internal capabilities aren't sufficient for the turnaround required.

While U.S. operations struggle, international markets are showing what the vision looks like when executed well. Global digital sales hit a record 20.3% mix in 2025, and international same-store sales grew 6.2% in Q4 despite the domestic headwinds. The company added 157 new international locations and remains on track for 2-3% annual net unit growth globally.

This divergence matters for your analysis. Wendy's isn't a single story; it's two stories running on different timelines. The international business demonstrates that the brand and operational model work when executed with discipline. The U.S. business demonstrates how quickly execution failures can erode decades of brand equity. For investors, this creates optionality: if Project Fresh succeeds domestically, you get a re-rating on the whole system. If it struggles, international growth provides a floor.

The Good Done Right ESG strategy aligns with the "beloved" vision by organizing commitments into three focus areas: Food (safety, quality, responsible sourcing, waste reduction), People (workplace culture, community giving), and Footprint (packaging, climate, water conservation). These aren't peripheral CSR activities; they're integrated into how Wendy's defines brand strength and long-term competitiveness.

The strategic value here is talent attraction and retention in a brutal labor market. Employee surveys show 68% of Wendy's workers are motivated by the mission and vision. That matters when you're trying to staff restaurants, and it matters for customer-facing consistency; motivated employees deliver better service. The company also maintains the WeCare Fund for employee financial assistance and emphasizes professional growth opportunities, translating values into concrete HR practices.

For investors, the ESG positioning addresses real operating risks: supply chain disruptions, regulatory pressure, and brand permission with younger consumers who increasingly factor values into purchasing decisions. It's risk mitigation dressed as values alignment, which is exactly how you want management to think about it.

Perhaps the clearest signal of strategic seriousness is where Wendy's is directing capital. The company is reducing Build to Suit program funding by approximately $20 million in 2025, with larger reductions anticipated in 2026, reallocating these resources toward technology and marketing. They're also shuttering 5-6% of underperforming U.S. restaurants, with 28 closures in Q4 2025 and more expected in the first half of 2026.

This is classic turnaround discipline: shrink to grow. Rather than chasing unit count metrics that look good in press releases, management is accepting the pain of closures to improve system health. The capital freed up goes to digital infrastructure, AI tools, and brand marketing, the capabilities that actually build toward "thriving and beloved" rather than just "big."

When we evaluate restaurant turnarounds, this capital allocation pattern is what separates serious management from those playing defense. Wendy's is making hard choices that prioritize long-term vision over short-term optics. Whether those choices create value depends on execution, but at least the strategic compass is pointed in the right direction.

Wendy's core values aren't just marketing copy plastered on break room walls, they're the operational DNA that shapes how franchisees run restaurants, how management allocates capital, and how employees interact with customers every day. Understanding these values gives investors insight into whether Wendy's can actually execute its turnaround or if it's just corporate theater.

This is Wendy's foundational value, and it maps directly to the fresh, never-frozen beef positioning that differentiated the brand when Dave Thomas opened his first restaurant in 1969. In 2026, this value still guides product decisions even when cheaper alternatives exist.

What it means operationally: Wendy's accepts higher food costs to maintain the fresh beef supply chain. When competitors froze patties to cut costs, Wendy's doubled down. This value explains why management delayed chicken sandwich launches to 2026 rather than rushing half-baked products to market during the Q4 2025 sales crisis. It also drives the "highest quality hamburger in QSR" brand positioning that guides marketing, menu decisions, and operational standards.

The tension for investors: Quality costs money, and Wendy's premium positioning requires execution discipline that hasn't always been there. When operations slip, quality becomes a liability, you pay more for ingredients but don't deliver the experience that justifies the price.

This value covers ethical conduct, business integrity, and honest dealings with customers, suppliers, and communities. It's the value that keeps the company aligned with legal and reputational standards in an industry plagued by high turnover and occasional corner-cutting.

What it means operationally: Wendy's Code of Conduct explicitly requires honesty, integrity, and compliance in all dealings, while avoiding conflicts of interest. The "Good Done Right" ESG strategy extends this into environmental stewardship and responsible sourcing. When the company faced COVID-19 challenges, this translated to prioritizing team member and customer safety over short-term sales.

💡 Expert Tip: When evaluating restaurant stocks for ESG integration, look at whether values like "Do the Right Thing" translate into concrete governance structures or just aspirational language. Wendy's has formalized this through their Chief Corporate Affairs & Sustainability Officer role and annual progress reporting on materiality-assessed goals. Companies without that structural commitment often treat values as crisis PR rather than operational guidance.

This value covers both customer-facing service standards and internal workplace culture. In a labor market where quick-service restaurants struggle to attract and retain talent, this is more than feel-good language, it's a competitive necessity.

What it means operationally: Wendy's provides professional growth opportunities, role-based training, and resources like the WeCare Fund for employee financial assistance. The company reports that 68% of workers are motivated by the mission and vision, with 11% citing loyalty to mission and 10% citing retention due to mission. For franchise relationships, this value translates to the "One Wendy's" approach, treating franchisees as partners rather than just royalty collectors.

In our experience analyzing restaurant labor metrics, companies that actually invest in employee value propositions tend to show up in customer satisfaction scores. The correlation isn't perfect, but when 68% of your workforce genuinely cares about the mission, service consistency improves. That's the operational payoff that shows up in same-store sales over time.

This value explicitly connects financial performance to sustainable expansion. It's a recognition that growth without profitability destroys value, and profitability without growth eventually gets competed away.

What it means operationally: Wendy's uses this value to guide capital allocation decisions under Project Fresh. The company reduced Build to Suit program funding by approximately $20 million in 2025, reallocating toward technology and marketing. They're also closing 5-6% of underperforming U.S. restaurants, accepting near-term pain for system health. The target to improve company margins by more than 200 basis points by 2028 reflects this value in concrete form.

The strategic implication: This value gives management permission to make hard choices that Wall Street might punish in the short term. Closing restaurants, delaying product launches, and accepting negative comps in 2026 are all consistent with "Profit Means Growth" even when they look like failure on quarterly earnings calls.

This value covers community involvement, charitable giving, and the broader stakeholder responsibility that increasingly matters to younger consumers and employees.

What it means operationally: Wendy's runs community programs like education scholarships and the TuneIn To Reading literacy initiative. The "Good Done Right" ESG strategy organizes commitments into three focus areas: Food (safety, quality, responsible sourcing, waste reduction), People (workplace culture, community giving), and Footprint (packaging, climate, water conservation). These align with UN Sustainable Development Goals and get reported annually with measurable progress.

As the company's Chief Corporate Affairs & Sustainability Officer put it, these efforts reflect that "doing business responsibly is simply good business." That's the framing value investors should look for, sustainability as risk mitigation and talent attraction, not just CSR theater.

Wendy's doesn't treat ESG as a separate initiative; it's integrated into how the company defines operational excellence and long-term competitiveness. The Good Done Right strategy extends the core values into specific commitments with measurable targets.

| Focus Area | Key Commitments | Connection to Core Values |

|---|---|---|

| Food | Safety, quality, responsible sourcing, waste reduction | Quality is Our Recipe, Do the Right Thing |

| People | Workplace culture, professional growth, community giving | Treat People with Respect, Give Something Back |

| Footprint | Sustainable packaging, climate action, water conservation | Do the Right Thing, Profit Means Growth (risk mitigation) |

The strategic value here is talent attraction and supply chain resilience. In our experience, restaurants that treat ESG as peripheral often struggle with both employee retention and supplier relationships when disruptions hit; Wendy's integration provides some buffer.

Here's the honest assessment every investor needs: Wendy's values are well-articulated and operationally relevant, but the gap between stated values and execution has widened in recent years.

Evidence of alignment:

Evidence of drift:

🎯 Pro Insight: When we evaluate restaurant turnarounds, we look for this pattern: can the company restore execution to match stated values, or have competitors permanently narrowed the gap? Wendy's company store performance proves the operational model still works. The question is whether franchisee adoption can scale fast enough to matter. Values create optionality, but only execution converts that into returns.

For investors using platforms like StockIntent to screen restaurant stocks, metrics like franchisee adoption rates, company vs. franchisee performance gaps, and customer satisfaction trend lines can help quantify that execution gap. You can test how companies with strong stated values but weak execution perform against peers using historical backtesting tools to see if execution recovery typically creates buying opportunities or value traps.

When you strip away the quarterly earnings noise and stock price volatility, Wendy's presents a coherent strategic identity built around three decades of quality-first positioning. The mission to exceed guest expectations, the vision to become the world's most thriving and beloved restaurant brand, and the five core values that operationalize these ambitions, all point to a company that knows exactly what it wants to be. The question for your portfolio isn't whether the strategy makes sense; it's whether management can execute it.

💡 Expert Tip: When evaluating turnarounds, we always check if the company has operational proof points before betting on system-wide recovery. Wendy's company stores outperforming franchisees by 310+ basis points is that proof point. It shows the playbook works when executed with discipline. You want to see this pattern, isolated excellence somewhere in the system, before concluding a turnaround has legs.

The investment-relevant picture that emerges is nuanced. On one hand, Wendy's maintains genuine differentiation through its fresh beef positioning and quality-first brand essence. Company-operated restaurants demonstrate that operational excellence is achievable. International growth (6.2% same-store sales in Q4 2025) proves the model works when executed with discipline. Digital transformation (20.3% sales mix) shows adaptation to modern consumer behavior.

On the other hand, the execution gap is real and material. Only 20% of franchisees have adopted operational excellence initiatives. U.S. same-store sales collapsed 11.3% in Q4 2025. Analysts have responded with a consensus "Hold" rating and limited price target upside, reflecting skepticism that Project Fresh can deliver rapid recovery.

In our experience analyzing restaurant turnarounds over the past 15 years, this pattern, strong strategic identity with uneven execution, is more common than exceptional. The companies that succeed share one characteristic: they maintain strategic discipline through the pain. Wendy's decision to delay chicken sandwich launches, close underperforming units, and reallocate capital toward technology rather than growth shows exactly that discipline. Whether it creates value or destroys it depends on franchisee adoption velocity and competitive response.

Looking ahead, 2026 is framed by management as a "rebuilding year." The strategic shifts on the horizon, further restaurant closures, scaled FreshAI deployment, franchisee support intensification, and international expansion, all serve the existing mission-vision-values framework rather than replacing it. There's no evidence of strategic drift or mission revision. If anything, Project Fresh represents a return to foundational principles after a period of promotional excess.

For value investors, this creates a classic setup: a quality business trading at uncertainty discount (P/E near 5-year lows) with identifiable catalysts for recovery. The analytical work centers on execution probability, not strategic clarity. Wendy's knows what it needs to do. The next 12-18 months will reveal whether it can actually do it.

If you're conducting deeper fundamental analysis on Wendy's or comparing restaurant turnaround opportunities, StockIntent's screening and backtesting tools can help you test execution patterns historically. You can explore how companies with similar strategic identities but varying execution track records have performed, and whether quality-focused quick-service chains typically recover from similar setbacks. Try it free for 7 days.

When you're evaluating a restaurant stock for your portfolio, understanding what actually drives the business matters more than the latest menu hype. Wendy's has built its competitive position around a philosophy that dates back to its founding in 1969, but like any mature company, that philosophy has evolved to meet current challenges.

Here's the quick answer: Wendy's official mission centers on exceeding guest expectations through superior quality products and services. The company aims to become the world's most thriving and beloved restaurant brand, supported by five core values that shape everything from menu decisions to franchise relationships. In 2026, this strategic identity is being tested by a major turnaround initiative called Project Fresh.

If you're trying to understand whether Wendy's makes sense as a long-term holding, you need to start with the business itself. Not the Frosty memes or the Twitter account, but the actual economics of running a quick-service restaurant chain in 2026.

Wendy's is a pure-play quick-service restaurant company operating in the consumer cyclical sector. Founded in 1969 by Dave Thomas in Columbus, Ohio, the company built its reputation on a simple but powerful differentiator: fresh, never-frozen beef patties. That quality-first positioning still defines the brand today, even as the restaurant landscape has become far more crowded.

The company operates roughly 7,000 restaurants globally, with approximately 95% owned by franchisees. This asset-light model means Wendy's generates revenue primarily through franchise royalties, real estate, and equipment leasing rather than direct restaurant operations. In our experience analyzing restaurant stocks, this capital structure can create more stable cash flows, but it also means you're betting on franchisee health, not just consumer demand.

As of early 2026, here's what defines Wendy's operations:

The company is currently navigating a challenging period. After reporting an 11.3% decline in U.S. same-restaurant sales in Q4 2025, management launched Project Fresh in October 2025, a comprehensive turnaround initiative aimed at reversing execution failures. The plan includes restaurant closures (roughly 5-6% of underperforming units), menu innovation delays (chicken sandwiches pushed to 2026), and a fundamental reallocation of capital away from restaurant construction toward technology and marketing.

Here's something that matters for your analysis: while U.S. operations struggle, international markets are showing resilience. Global digital sales hit a record 20.3% mix in 2025, and international same-restaurant sales grew 6.2% in Q4 despite the domestic headwinds. This divergence between geographies is worth watching as you evaluate whether Wendy's can execute a simultaneous turnaround at home while scaling abroad.

| Metric | Snapshot |

|---|---|

| Total Restaurants | ~7,000 globally |

| Franchise Mix | 95% franchisee-operated |

| Q4 2025 U.S. Same-Store Sales | (11.3%) |

| Q4 2025 International Same-Store Sales | +6.2% |

| Digital Sales Mix (U.S.) | 20% (up 12.4% YoY) |

| Net Unit Growth Target | 2-3% annually |

The competitive positioning here is nuanced. Wendy's sits in a crowded space between McDonald's (scale dominance), Burger King (value positioning), and Chipotle/Chick-fil-A (quality perception). The company has historically punched above its weight on customer satisfaction, but recent execution missteps, what management described as missing the boat on everyday value while over-relying on limited-time promotions, have dented that advantage. When we look at restaurant turnarounds, the question isn't whether the brand can recover; it's whether management can fix operational execution faster than competitors can capture that market share.

"To exceed our guests' expectations in product, service, and overall dining experience."

That's Wendy's official mission statement, and it reads like something Dave Thomas might have scribbled on a napkin in 1969. Simple, direct, and focused entirely on the customer. No buzzwords about "synergies" or "paradigm shifts." Just a commitment to doing the basics better than anyone else.

But here's what makes this interesting for your analysis: this mission isn't just marketing fluff. It directly shapes how Wendy's allocates capital and makes strategic trade-offs.

🎯 Pro Insight: When evaluating restaurant stocks, we always compare stated mission against actual capital allocation. Wendy's mission prioritizes guest experience over pure efficiency, which explains why they accept higher food costs for fresh beef and why Project Fresh directs $20 million away from new restaurant construction toward technology and marketing. Companies that actually live their mission tend to make more consistent long-term decisions.

The mission's three pillars, product, service, and overall dining experience, map cleanly to Wendy's operational priorities in 2026. Product means the fresh, never-frozen beef positioning that still differentiates them from McDonald's and Burger King. Service covers the digital transformation and operational excellence initiatives under Project Fresh. And "overall dining experience" captures everything from restaurant remodels to the brand revitalization work with Creed UnCo, the consultancy led by former Yum! Brands CEO Greg Creed.

Compare this to McDonald's mission "to be our customers' favorite place and way to eat" or Chick-fil-A's newer "Be REMARKable." Wendy's formulation is more concrete and measurable. You can actually track whether you're exceeding guest expectations through satisfaction scores, same-store sales, and brand perception metrics. "Favorite place" and "remarkable" are harder to quantify, which makes them harder to execute against.

The mission has evolved over time. Earlier versions from the 2000s emphasized "exceeding customer expectations everyday" without the specificity around product and service. A mid-period variant focused on "quality, integrity, and responsibility." The current formulation, which gained prominence around 2024, adds explicit emphasis on innovation and partnerships alongside the core guest focus. This evolution tracks with Wendy's strategic shift from a U.S.-centric operational story to a global growth narrative with digital and sustainability components.

For investors, the mission statement matters because it signals what management won't compromise, even under pressure. When Wendy's reported that 11.3% same-store sales decline in Q4 2025, leadership didn't abandon the quality positioning to chase volume with deep discounting. Instead, they doubled down on operational excellence and system health, accepting near-term pain for what they believe is a stronger long-term position. Whether that discipline creates value or destroys it depends on execution, but at least the strategic compass is clear.

Wendy's mission isn't just a sentence on a poster, it's an operating system that shapes how capital gets deployed and how management makes trade-offs. When we look at restaurant turnarounds, the difference between companies that recover and those that don't often comes down to whether leadership actually runs the business according to stated principles, or just talks about them.

The mission breaks down into three interconnected pillars: exceeding guest expectations, product and service excellence, and delivering a superior overall dining experience. Each pillar has concrete strategic implications and, more importantly for your analysis, measurable outcomes you can track.

This is the foundational pillar that everything else serves. Wendy's doesn't aim to meet industry benchmarks; the explicit goal is to surpass what customers anticipate from a quick-service restaurant. This sounds like generic corporate speak until you look at how it actually shows up in operations.

In our experience analyzing customer satisfaction data across restaurant chains, companies that explicitly target "exceeding expectations" rather than "satisfying customers" tend to invest differently. They spend more on training, accept higher food costs for quality ingredients, and resist the temptation to trade down during tough periods. Wendy's fits this pattern; even during the brutal Q4 2025 when same-store sales collapsed 11.3%, management didn't abandon the fresh beef positioning to chase volume with deep discounting.

The metric that matters here is customer satisfaction relative to competitors. Wendy's has historically punched above its weight here, though recent execution missteps have dented that advantage. When we track restaurant stocks, we watch for divergence between stated mission priorities and actual promotional behavior. Wendy's admitted they "swung too far on promotions" and "missed the boat" on everyday value, which tells you the mission discipline broke down temporarily. Project Fresh is essentially an attempt to rebuild that alignment.

This pillar translates the guest expectation goal into operational specifics. For Wendy's, "product" means the fresh, never-frozen beef positioning that still differentiates them from McDonald's and Burger King. "Service" covers the digital transformation, operational efficiency, and hospitality standards that determine whether the quality promise actually reaches the customer.

The strategic value here is differentiation in a commoditized industry. Quick-service burgers are largely undifferentiated in consumers' minds; the battle is won on convenience, price, and occasional quality perception. Wendy's fresh beef claim gives them a tangible point of difference that supports premium pricing and brand loyalty.

Recent initiatives demonstrating this pillar in action:

| Initiative | What It Is | Why It Matters for Investors |

|---|---|---|

| FreshAI deployment | AI-powered drive-thru and kitchen tools | Labor efficiency + order accuracy improvements that reduce waste and boost throughput |

| Digital sales growth | Mobile app, rewards integration, delivery partnerships | Record 20.3% digital mix in 2025; higher-margin channel with better customer data |

| Menu optimization | Delaying chicken sandwich launches to 2026, focusing on $6 Biggie Bag and $4 Biggie Bites | Discipline over chasing trendy LTOs; building sustainable everyday value position |

| Company store blueprint | U.S. company-operated restaurants outperforming system by 310 bps in 2025 | Proving the operational model works before pushing to franchisees |

The key insight for your analysis: Wendy's is using company-operated stores as a laboratory and proof point. When company stores outperform by 310 basis points (410 bps in Q4), that's not accidental. It shows the operational playbook works when executed with discipline. The problem, and it's a big one, is that only 20% of franchisees have fully adopted these initiatives. This creates a two-tier system where corporate can claim operational excellence while the majority of the system lags.

For investors, this translates to execution risk concentrated in franchisee adoption. You're not betting on whether Wendy's knows what to do; they clearly do. You're betting on whether they can convince independent franchisees to actually do it.

The third pillar broadens the focus from the transaction to the complete brand interaction. This covers restaurant environment, brand perception, community connection, and increasingly, the values alignment that younger consumers expect from the companies they patronize.

Wendy's operationalizes this through their Good Done Right ESG strategy, which organizes commitments into three focus areas: Food (safety, quality, responsible sourcing, waste reduction), People (workplace culture, community giving), and Footprint (packaging, climate, water conservation). These aren't peripheral CSR activities; they're integrated into how Wendy's defines brand strength and long-term competitiveness.

The competitive advantage here is talent attraction and retention in a brutal labor market. Employee surveys show 68% of Wendy's workers are motivated by the mission and vision. That matters when you're trying to staff restaurants in a tight labor environment. It also matters for customer-facing consistency; motivated employees deliver better service.

The strategic positioning against macro trends is worth noting. Quick-service restaurants face pressure on multiple fronts: labor costs, sustainability expectations, health-conscious menus, and digital transformation. Wendy's vision of becoming "the world's most thriving and beloved restaurant brand" explicitly targets leadership in navigating these trends rather than reactive adaptation.

| Trend | Wendy's Response | Moat Implication |

|---|---|---|

| Labor efficiency pressure | AI tools, labor model evolution, training investment | Lower unit labor costs + better service consistency |

| Sustainability demands | Good Done Right commitments, traceable sourcing | Brand permission to operate; risk mitigation |

| Digital transformation | 20% digital mix, app ecosystem, delivery partnerships | Customer data advantage; higher-margin channel mix |

| International expansion | 6.2% Q4 international same-store sales growth; 157 new locations | Diversification away from U.S. headwinds; growth optionality |

For value investors, the critical question is whether these mission pillars translate into durable competitive advantages, what Buffett calls economic moats. Here's our assessment:

Quality differentiation as moat: The fresh beef positioning is real but narrow. It supports premium pricing and brand loyalty, but it's vulnerable to competitor imitation (as we've seen with "fresh" claims from others) and to Wendy's own execution failures. When operations slip, the quality advantage erodes quickly. This is a moat that requires constant maintenance.

Operational excellence as moat: More promising, but currently bifurcated. The company store performance proves the playbook works. If Wendy's can drive franchisee adoption, system-wide efficiency gains create a scale advantage that's hard to replicate. The "One Wendy's" approach to franchisee economics, if successful, builds a network effect moat where the whole system performs better, attracting better franchisees and creating virtuous cycle.

Brand strength as moat: The "beloved brand" vision targets emotional connection that transcends transactional convenience. This is the strongest potential moat but also the hardest to build and easiest to damage. Wendy's social media savvy and quality positioning have created brand permission that competitors lack. The question is whether Project Fresh execution restores that advantage or further erodes it.

The honest assessment: Wendy's mission pillars create conditional competitive advantages that depend heavily on execution. They're not structural moats like Coca-Cola's brand or Microsoft's network effects. They're earned advantages that must be continuously reinvested in and defended. For investors, this means the quality of management execution matters enormously, more than in businesses with deeper structural protections.

When we evaluate restaurant stocks for long-term holding, we look for that combination of clear strategic identity and demonstrated ability to execute. Wendy's has the former in spades. The next 12-18 months will tell us whether they can recover the latter.

"To become the world's most thriving and beloved restaurant brand."

That's the vision that guides Wendy's long-term strategic positioning. Where the mission focuses on day-to-day execution (exceeding guest expectations), the vision sets the destination: global brand leadership measured by both financial performance and customer affection.

The key word here is "thriving." It's not just about being big or well-known; it's about sustainable profitability and system health. This matters for your analysis because it signals that Wendy's management prioritizes franchisee economics and operational health over pure growth metrics. When we evaluate restaurant turnarounds, we look for exactly this kind of discipline; companies that chase unit growth at the expense of system health often end up destroying shareholder value.

The "beloved" piece is equally important. Quick-service restaurants operate in a brutally competitive space where switching costs are essentially zero. Being "liked" isn't enough; you need emotional loyalty that transcends price. Wendy's aims to build this through quality differentiation and brand personality, the same factors that have historically allowed them to command slight pricing premiums over value peers.

Wendy's leadership has articulated several long-term goals that operationalize this vision:

1. Margin expansion through operational excellence

Management has targeted improving company margins by more than 200 basis points by 2028, achieved through P&L benchmarking, productivity upgrades, menu strategy evolution, and technology deployment. This includes making all restaurants "model restaurants" with consistent performance standards, more field support, and dedicated leaders per franchisee.

2. Bold global growth

The vision explicitly targets international expansion, with Wendy's actively seeking new franchise owners to build global presence. In Q4 2025, international same-store sales grew 6.2% while U.S. sales declined 11.3%. This divergence isn't accidental; it's the result of deliberate investment in markets where the brand has permission to grow.

3. Sustainability as competitive moat

The Good Done Right ESG strategy aligns with UN Sustainable Development Goals across food security, sustainable consumption, economic growth, and inequality reduction. For investors, this isn't just CSR theater. It addresses real operating risks (supply chain disruptions, regulatory pressure, talent attraction) while building brand permission with younger consumers who increasingly factor values into purchasing decisions.

The vision positions Wendy's to lead rather than follow major restaurant industry shifts:

| Macro Trend | Wendy's Strategic Response | Vision Alignment |

|---|---|---|

| Sustainability demands | Good Done Right commitments on responsible sourcing, packaging, climate action | "Beloved" brand through values alignment |

| Labor efficiency pressure | AI-powered tools (FreshAI), labor model evolution, training investment | "Thriving" through unit economics improvement |

| Digital transformation | 20.3% digital sales mix, app ecosystem, delivery partnerships | Enhanced customer experience and data advantage |

| International expansion | 6.2% Q4 international growth; 157 new global locations | Global scale toward "world's most thriving" |

| Value-conscious consumers | $6 Biggie Bag, $4 Biggie Bites as permanent value platform | Accessibility supporting "beloved" status |

The honest assessment: Wendy's vision is ambitious but not delusional. It doesn't claim they'll dominate every market or invent new categories. Instead, it targets a specific position, the highest quality choice in quick-service, executed at global scale with sustainable economics. This is achievable if Project Fresh delivers on its operational promises.

For your portfolio analysis, the vision matters because it sets the bounds on what management will and won't do. When evaluating Project Fresh investments, ask whether each initiative builds toward "thriving and beloved" or just chases short-term comps. The vision is your compass for assessing strategic coherence.

Wendy's vision of becoming "the world's most thriving and beloved restaurant brand" isn't just aspirational language, it's a strategic framework that shapes capital allocation, operational priorities, and how management navigates trade-offs. When we analyze restaurant turnarounds, we look for exactly this kind of clarity: a destination that guides decision-making when the path gets messy.

The vision breaks down into four interconnected themes that you'll see reflected in every earnings call and investor presentation. Each theme has concrete metrics and initiatives attached, which is how you separate real strategy from corporate theater.

The "thriving" part of the vision starts with unit economics that actually work. Wendy's has set a target to improve company margins by more than 200 basis points by 2028, achieved through five specific strategies: P&L benchmarking, operations productivity upgrades, menu strategy evolution, technology deployment, and labor model evolution.

Here's what this looks like in practice. In 2025, U.S. company-operated restaurants outperformed the system by 310 basis points (410 bps in Q4), driven by training investments, performance management systems, digital tools like FreshAI, and improved customer satisfaction scores across accuracy, taste, and friendliness. The company is using these locations as a blueprint for franchisee rollout, proving the operational model works before pushing it system-wide.

The catch, and it's a significant one, is adoption velocity. Only 20% of franchisees have fully implemented these initiatives as of early 2026. This creates a two-tier system where corporate can claim operational excellence while the majority of the system lags. For investors, this translates to execution risk concentrated in franchisee relationships, not operational knowledge.

| Operational Initiative | Company Store Performance | Franchisee Adoption | Strategic Implication |

|---|---|---|---|

| FreshAI deployment | Higher throughput, lower waste | ~20% fully adopted | Technology moat requires scale |

| Training programs | +310 bps vs. system average | Rolling out 2026 | Human capital as differentiator |

| Digital integration | 20% sales mix, record highs | Varies by operator | Data advantage requires uniformity |

The "beloved" component of the vision targets emotional loyalty that transcends price competition. Wendy's has reframed its brand essence around being the "highest quality hamburger in QSR," a positioning that guides marketing, menu decisions, operations, and customer experience design.

This isn't just marketing fluff. It directly shapes product strategy. When management admitted they had "swung too far on promotions" and "missed the boat" on everyday value, they weren't abandoning quality to chase volume. Instead, they delayed chicken sandwich launches to 2026 and doubled down on permanent value platforms like the $6 Biggie Bag and $4 Biggie Bites. The discipline here is notable: accepting near-term sales pain to avoid diluting the quality positioning that supports long-term pricing power.

The company also brought in Creed UnCo, led by former Yum! Brands CEO Greg Creed, to transform marketing effectiveness. This signals serious commitment to brand building rather than incremental tweaks. When you see a company hiring outside expertise at the CEO level for marketing, it usually means they recognize internal capabilities aren't sufficient for the turnaround required.

While U.S. operations struggle, international markets are showing what the vision looks like when executed well. Global digital sales hit a record 20.3% mix in 2025, and international same-store sales grew 6.2% in Q4 despite the domestic headwinds. The company added 157 new international locations and remains on track for 2-3% annual net unit growth globally.

This divergence matters for your analysis. Wendy's isn't a single story; it's two stories running on different timelines. The international business demonstrates that the brand and operational model work when executed with discipline. The U.S. business demonstrates how quickly execution failures can erode decades of brand equity. For investors, this creates optionality: if Project Fresh succeeds domestically, you get a re-rating on the whole system. If it struggles, international growth provides a floor.

The Good Done Right ESG strategy aligns with the "beloved" vision by organizing commitments into three focus areas: Food (safety, quality, responsible sourcing, waste reduction), People (workplace culture, community giving), and Footprint (packaging, climate, water conservation). These aren't peripheral CSR activities; they're integrated into how Wendy's defines brand strength and long-term competitiveness.

The strategic value here is talent attraction and retention in a brutal labor market. Employee surveys show 68% of Wendy's workers are motivated by the mission and vision. That matters when you're trying to staff restaurants, and it matters for customer-facing consistency; motivated employees deliver better service. The company also maintains the WeCare Fund for employee financial assistance and emphasizes professional growth opportunities, translating values into concrete HR practices.

For investors, the ESG positioning addresses real operating risks: supply chain disruptions, regulatory pressure, and brand permission with younger consumers who increasingly factor values into purchasing decisions. It's risk mitigation dressed as values alignment, which is exactly how you want management to think about it.

Perhaps the clearest signal of strategic seriousness is where Wendy's is directing capital. The company is reducing Build to Suit program funding by approximately $20 million in 2025, with larger reductions anticipated in 2026, reallocating these resources toward technology and marketing. They're also shuttering 5-6% of underperforming U.S. restaurants, with 28 closures in Q4 2025 and more expected in the first half of 2026.

This is classic turnaround discipline: shrink to grow. Rather than chasing unit count metrics that look good in press releases, management is accepting the pain of closures to improve system health. The capital freed up goes to digital infrastructure, AI tools, and brand marketing, the capabilities that actually build toward "thriving and beloved" rather than just "big."

When we evaluate restaurant turnarounds, this capital allocation pattern is what separates serious management from those playing defense. Wendy's is making hard choices that prioritize long-term vision over short-term optics. Whether those choices create value depends on execution, but at least the strategic compass is pointed in the right direction.

Wendy's core values aren't just marketing copy plastered on break room walls, they're the operational DNA that shapes how franchisees run restaurants, how management allocates capital, and how employees interact with customers every day. Understanding these values gives investors insight into whether Wendy's can actually execute its turnaround or if it's just corporate theater.

This is Wendy's foundational value, and it maps directly to the fresh, never-frozen beef positioning that differentiated the brand when Dave Thomas opened his first restaurant in 1969. In 2026, this value still guides product decisions even when cheaper alternatives exist.

What it means operationally: Wendy's accepts higher food costs to maintain the fresh beef supply chain. When competitors froze patties to cut costs, Wendy's doubled down. This value explains why management delayed chicken sandwich launches to 2026 rather than rushing half-baked products to market during the Q4 2025 sales crisis. It also drives the "highest quality hamburger in QSR" brand positioning that guides marketing, menu decisions, and operational standards.

The tension for investors: Quality costs money, and Wendy's premium positioning requires execution discipline that hasn't always been there. When operations slip, quality becomes a liability, you pay more for ingredients but don't deliver the experience that justifies the price.

This value covers ethical conduct, business integrity, and honest dealings with customers, suppliers, and communities. It's the value that keeps the company aligned with legal and reputational standards in an industry plagued by high turnover and occasional corner-cutting.

What it means operationally: Wendy's Code of Conduct explicitly requires honesty, integrity, and compliance in all dealings, while avoiding conflicts of interest. The "Good Done Right" ESG strategy extends this into environmental stewardship and responsible sourcing. When the company faced COVID-19 challenges, this translated to prioritizing team member and customer safety over short-term sales.

💡 Expert Tip: When evaluating restaurant stocks for ESG integration, look at whether values like "Do the Right Thing" translate into concrete governance structures or just aspirational language. Wendy's has formalized this through their Chief Corporate Affairs & Sustainability Officer role and annual progress reporting on materiality-assessed goals. Companies without that structural commitment often treat values as crisis PR rather than operational guidance.

This value covers both customer-facing service standards and internal workplace culture. In a labor market where quick-service restaurants struggle to attract and retain talent, this is more than feel-good language, it's a competitive necessity.

What it means operationally: Wendy's provides professional growth opportunities, role-based training, and resources like the WeCare Fund for employee financial assistance. The company reports that 68% of workers are motivated by the mission and vision, with 11% citing loyalty to mission and 10% citing retention due to mission. For franchise relationships, this value translates to the "One Wendy's" approach, treating franchisees as partners rather than just royalty collectors.

In our experience analyzing restaurant labor metrics, companies that actually invest in employee value propositions tend to show up in customer satisfaction scores. The correlation isn't perfect, but when 68% of your workforce genuinely cares about the mission, service consistency improves. That's the operational payoff that shows up in same-store sales over time.

This value explicitly connects financial performance to sustainable expansion. It's a recognition that growth without profitability destroys value, and profitability without growth eventually gets competed away.

What it means operationally: Wendy's uses this value to guide capital allocation decisions under Project Fresh. The company reduced Build to Suit program funding by approximately $20 million in 2025, reallocating toward technology and marketing. They're also closing 5-6% of underperforming U.S. restaurants, accepting near-term pain for system health. The target to improve company margins by more than 200 basis points by 2028 reflects this value in concrete form.

The strategic implication: This value gives management permission to make hard choices that Wall Street might punish in the short term. Closing restaurants, delaying product launches, and accepting negative comps in 2026 are all consistent with "Profit Means Growth" even when they look like failure on quarterly earnings calls.

This value covers community involvement, charitable giving, and the broader stakeholder responsibility that increasingly matters to younger consumers and employees.

What it means operationally: Wendy's runs community programs like education scholarships and the TuneIn To Reading literacy initiative. The "Good Done Right" ESG strategy organizes commitments into three focus areas: Food (safety, quality, responsible sourcing, waste reduction), People (workplace culture, community giving), and Footprint (packaging, climate, water conservation). These align with UN Sustainable Development Goals and get reported annually with measurable progress.

As the company's Chief Corporate Affairs & Sustainability Officer put it, these efforts reflect that "doing business responsibly is simply good business." That's the framing value investors should look for, sustainability as risk mitigation and talent attraction, not just CSR theater.

Wendy's doesn't treat ESG as a separate initiative; it's integrated into how the company defines operational excellence and long-term competitiveness. The Good Done Right strategy extends the core values into specific commitments with measurable targets.

| Focus Area | Key Commitments | Connection to Core Values |

|---|---|---|

| Food | Safety, quality, responsible sourcing, waste reduction | Quality is Our Recipe, Do the Right Thing |

| People | Workplace culture, professional growth, community giving | Treat People with Respect, Give Something Back |

| Footprint | Sustainable packaging, climate action, water conservation | Do the Right Thing, Profit Means Growth (risk mitigation) |

The strategic value here is talent attraction and supply chain resilience. In our experience, restaurants that treat ESG as peripheral often struggle with both employee retention and supplier relationships when disruptions hit; Wendy's integration provides some buffer.

Here's the honest assessment every investor needs: Wendy's values are well-articulated and operationally relevant, but the gap between stated values and execution has widened in recent years.

Evidence of alignment:

Evidence of drift:

🎯 Pro Insight: When we evaluate restaurant turnarounds, we look for this pattern: can the company restore execution to match stated values, or have competitors permanently narrowed the gap? Wendy's company store performance proves the operational model still works. The question is whether franchisee adoption can scale fast enough to matter. Values create optionality, but only execution converts that into returns.

For investors using platforms like StockIntent to screen restaurant stocks, metrics like franchisee adoption rates, company vs. franchisee performance gaps, and customer satisfaction trend lines can help quantify that execution gap. You can test how companies with strong stated values but weak execution perform against peers using historical backtesting tools to see if execution recovery typically creates buying opportunities or value traps.

When you strip away the quarterly earnings noise and stock price volatility, Wendy's presents a coherent strategic identity built around three decades of quality-first positioning. The mission to exceed guest expectations, the vision to become the world's most thriving and beloved restaurant brand, and the five core values that operationalize these ambitions, all point to a company that knows exactly what it wants to be. The question for your portfolio isn't whether the strategy makes sense; it's whether management can execute it.

💡 Expert Tip: When evaluating turnarounds, we always check if the company has operational proof points before betting on system-wide recovery. Wendy's company stores outperforming franchisees by 310+ basis points is that proof point. It shows the playbook works when executed with discipline. You want to see this pattern, isolated excellence somewhere in the system, before concluding a turnaround has legs.

The investment-relevant picture that emerges is nuanced. On one hand, Wendy's maintains genuine differentiation through its fresh beef positioning and quality-first brand essence. Company-operated restaurants demonstrate that operational excellence is achievable. International growth (6.2% same-store sales in Q4 2025) proves the model works when executed with discipline. Digital transformation (20.3% sales mix) shows adaptation to modern consumer behavior.

On the other hand, the execution gap is real and material. Only 20% of franchisees have adopted operational excellence initiatives. U.S. same-store sales collapsed 11.3% in Q4 2025. Analysts have responded with a consensus "Hold" rating and limited price target upside, reflecting skepticism that Project Fresh can deliver rapid recovery.

In our experience analyzing restaurant turnarounds over the past 15 years, this pattern, strong strategic identity with uneven execution, is more common than exceptional. The companies that succeed share one characteristic: they maintain strategic discipline through the pain. Wendy's decision to delay chicken sandwich launches, close underperforming units, and reallocate capital toward technology rather than growth shows exactly that discipline. Whether it creates value or destroys it depends on franchisee adoption velocity and competitive response.

Looking ahead, 2026 is framed by management as a "rebuilding year." The strategic shifts on the horizon, further restaurant closures, scaled FreshAI deployment, franchisee support intensification, and international expansion, all serve the existing mission-vision-values framework rather than replacing it. There's no evidence of strategic drift or mission revision. If anything, Project Fresh represents a return to foundational principles after a period of promotional excess.

For value investors, this creates a classic setup: a quality business trading at uncertainty discount (P/E near 5-year lows) with identifiable catalysts for recovery. The analytical work centers on execution probability, not strategic clarity. Wendy's knows what it needs to do. The next 12-18 months will reveal whether it can actually do it.

If you're conducting deeper fundamental analysis on Wendy's or comparing restaurant turnaround opportunities, StockIntent's screening and backtesting tools can help you test execution patterns historically. You can explore how companies with similar strategic identities but varying execution track records have performed, and whether quality-focused quick-service chains typically recover from similar setbacks. Try it free for 7 days.